Friday’s tape was a neat little paradox: a weaker jobs report helped push the strongest indexes to new records. AI optimism stayed the headline, first in chips, then in power, while Washington kept investors on their toes with tariffs, housing “policy,” and some very loud Venezuela talk.

The close: records, with a side of “soft landing?”

The S&P 500 finished at 6,966.28 (+0.65%) and notched a record close, while the Dow ended at 49,504.07 (+0.48%), still less than 500 points from the psychologically ridiculous 50,000 milestone. The Nasdaq tagged along at 23,671.35 (+0.82%).

The catalyst was the December jobs report: +50,000 payrolls (below expectations), while unemployment improved to 4.4%. That combo is basically catnip for the “Fed cuts later this year” crowd.

And yes, revisions mattered too (downward), reinforcing the “slowing but not breaking” narrative.

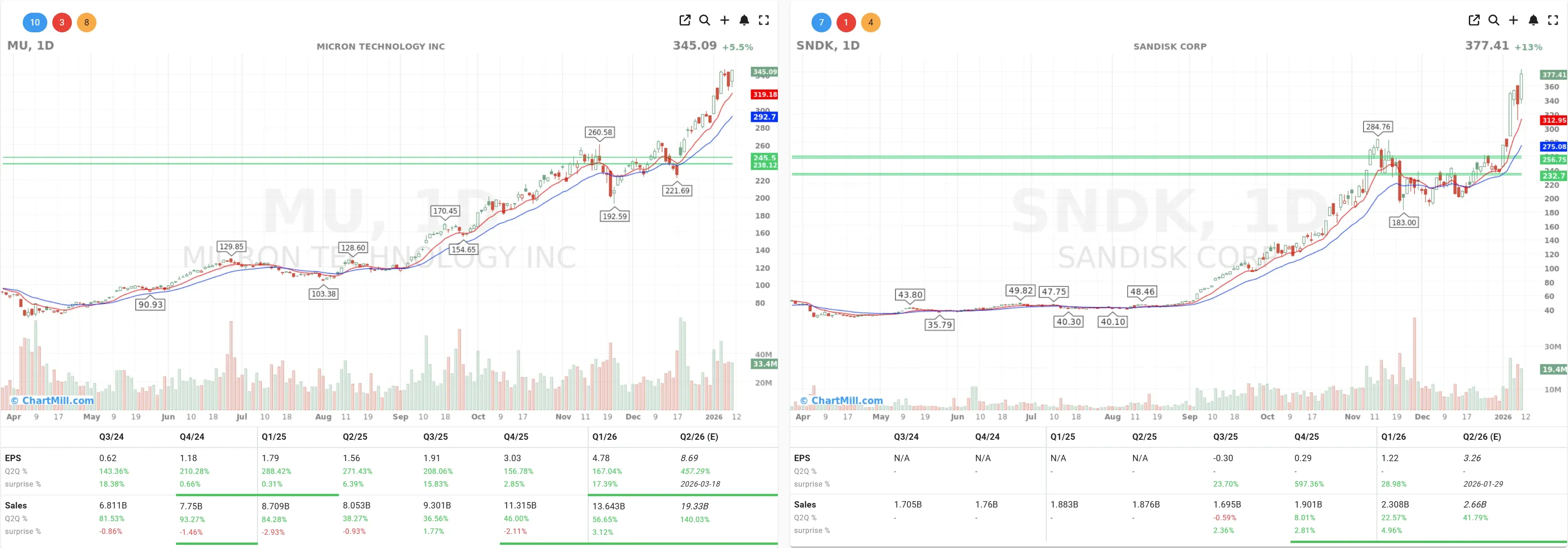

AI trade, but make it… memory (and semis)

The AI supply chain stayed front-and-center, and the market got more selective about which picks-and-shovels it wants.

Sandisk (SNDK | +12.81%) ripped higher after Mizuho cranked its price target from 250 to 410.

Micron (MU | +5.53%) stayed hot as analysts leaned into the “AI memory supercycle” idea.

On the broader chip tape, Lam Research (LRCX | +8.66%) surged after a target hike, and Broadcom (AVGO | +3.76%) helped drag the index higher.

Then came the headline whiplash: Intel (INTC | +10.8%) popped after President Trump praised CEO Lip-Bu Tan, proof that in 2026, a social post can still move a $100B+ company like it’s a microcap.

Housing stocks caught a policy tailwind

The other standout pocket was housing, after Trump pushed a plan involving $200B in mortgage-bond purchases via the housing GSE ecosystem.

That spilled into everything interest-rate-sensitive:

Home Depot (HD | +4.19%) was a top Dow contributor.

Homebuilders jumped: Lennar (LEN | +8.85%) and D.R. Horton (DHI | +7.80%) moved like rates just got cut 50 bps.

Even “housing transaction + mortgage machinery” stocks plays flew: loanDepot (LDI | +19.26%), Rocket Companies (RKT | +9.65%), and Opendoor (OPEN | +13.37%).

Macro and geopolitics: the stuff that can still ruin a good rally

Two big “overhang” items refused to go away:

-

Tariffs: The U.S. Supreme Court didn’t issue a ruling Friday on the legality of Trump’s sweeping tariffs, leaving markets waiting for clarity that could hit trade policy (and volatility) hard when it finally lands.

-

Oil + Venezuela/Iran risk: WTI hovered around the $58 handle, with the move tied to supply-disruption concerns (Venezuela and Iran were top-of-mind).

The euro ended near 1.1636 versus the dollar, basically reinforcing that FX traders are still pricing the U.S. as “higher-for-longer-ish,” even when jobs data softens.

What I’m watching next

If you’re wondering what could spoil the party: it’s not earnings yet, it’s policy uncertainty. A tariffs ruling could reprice risk fast, and the Fed leadership drama is already starting to matter as Powell’s term end approaches in May 2026.

Kristoff - ChartMill

Next to read: Small-Caps Break Higher As Participation Improves