QUALCOMM INC (NASDAQ:QCOM) Fits Peter Lynch’s Growth at a Fair Price Strategy

By Mill Chart

Last update: Aug 12, 2025

Peter Lynch’s investment strategy, described in One Up on Wall Street, centers on finding companies with steady growth at fair prices. His method combines growth and value investing, focusing on strong fundamentals, consistent profits, and low debt. The strategy steers clear of overly hyped or rapidly expanding firms, preferring those with clear, stable growth paths. A crucial measure in Lynch’s approach is the PEG ratio (Price/Earnings to Growth), which checks if a stock’s price matches its earnings growth. Other important factors include high return on equity (ROE), low debt, and good liquidity, all of which point to companies likely to provide long-term gains without high risk.

QUALCOMM INC (NASDAQ:QCOM) stands out as a strong option under this framework. The semiconductor and wireless technology company fits many of Lynch’s criteria, making it a good choice for investors looking for growth at a fair price. Here’s how QCOM matches the strategy’s main principles:

Valuation and Growth: The PEG Ratio

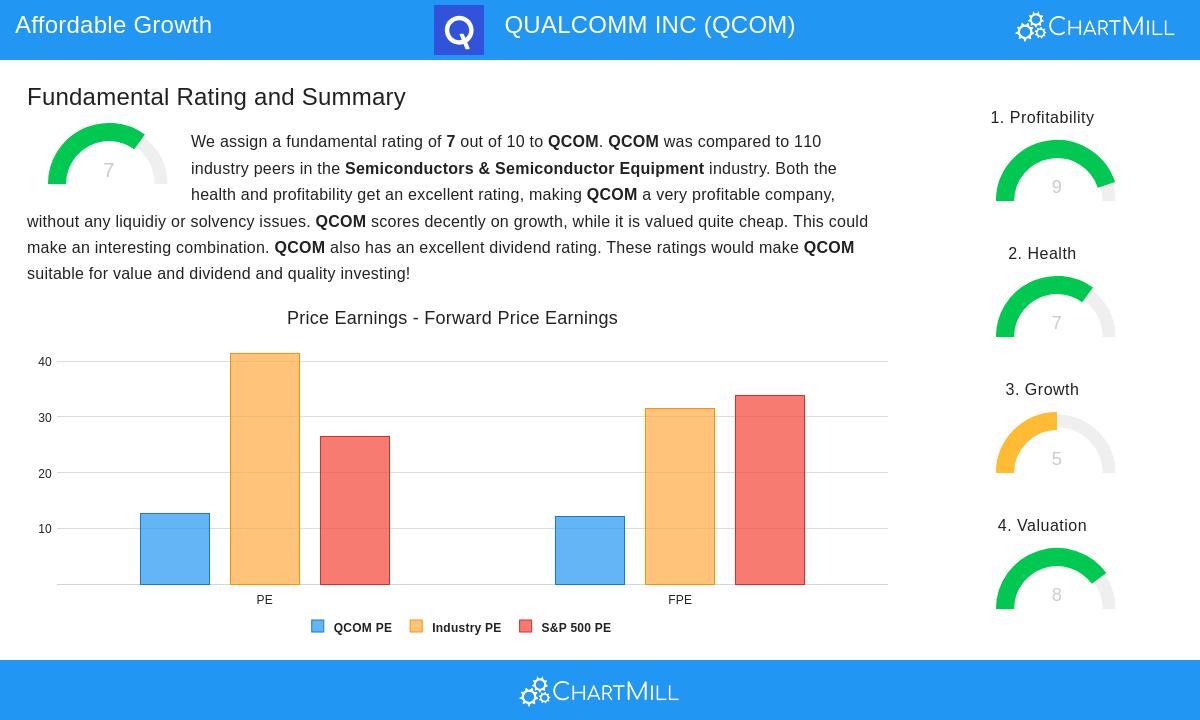

Lynch used the PEG ratio to avoid stocks priced too high for their growth potential. QCOM’s PEG ratio of 0.54 (based on the last 5 years of earnings growth) points to undervaluation, well under Lynch’s limit of 1. This implies the market hasn’t fully recognized QCOM’s historical EPS growth of 23.5% per year, a rate Lynch would view as steady given it stays below his 30% cap. The company’s forward P/E of 12.14 also highlights its fair pricing compared to competitors and the S&P 500.

Profitability: Return on Equity (ROE)

A high ROE shows effective use of investor funds, a trait Lynch valued. QCOM’s ROE of 42.6% exceeds Lynch’s 15% target and places it in the top 7% of its industry. This indicates strong pricing control and operational effectiveness, key for sustained growth.

Financial Health: Debt and Liquidity

Lynch preferred firms with little debt to handle economic challenges. QCOM’s debt-to-equity ratio of 0.54 fits his acceptable range (under 0.6), and its current ratio of 3.19 shows it can easily meet short-term needs. Importantly, the company’s free cash flow covers its debt well, with a debt-to-FCF ratio of just 1.27, signaling financial stability.

Fundamental Strength: A High-Level Summary

QUALCOMM’s fundamental report gives it a score of 7/10, noting strong profitability (9/10) and solid financial health (7/10). Key advantages include:

- Top-tier margins: Operating margin of 28.1% and profit margin of 26.8%, both better than 85% of peers.

- Reliable dividend: A 2.4% yield with a payout ratio of only 33%, backed by over a decade of steady payments.

- Smart reinvestment: ROIC of 20.4% beats the industry average, showing it uses profits wisely.

Though growth may slow (7.2% annual EPS growth forecast), QCOM’s pricing reflects this, keeping it attractive for growth at a fair price.

Why These Metrics Matter

Lynch’s strategy avoids paying too much for growth while ensuring firms have the financial strength to perform. QCOM’s low PEG ratio, high ROE, and modest debt align well with this idea. Its leadership in essential wireless technologies, a sector with lasting demand, adds a qualitative edge, matching Lynch’s liking for stable industries with reliable growth.

For investors searching for similar opportunities, find more Peter Lynch screen results here.

Disclaimer: This analysis is not investment advice. Do your own research or consult a financial advisor before making decisions.

180.19

-2.26 (-1.24%)

Find more stocks in the Stock Screener

QCOM Latest News and Analysis