Semis stumbled, healthcare ripped, and the macro tape said “it’s complicated.”

Market wrap—records on pause

The Dow edged up +0.1% while the S&P 500 (-0.3%) and Nasdaq (-0.4%) cooled after a string of record highs. The drag came from chip-adjacent weakness, offset by a healthcare surge after Berkshire’s 13F hit the wire.

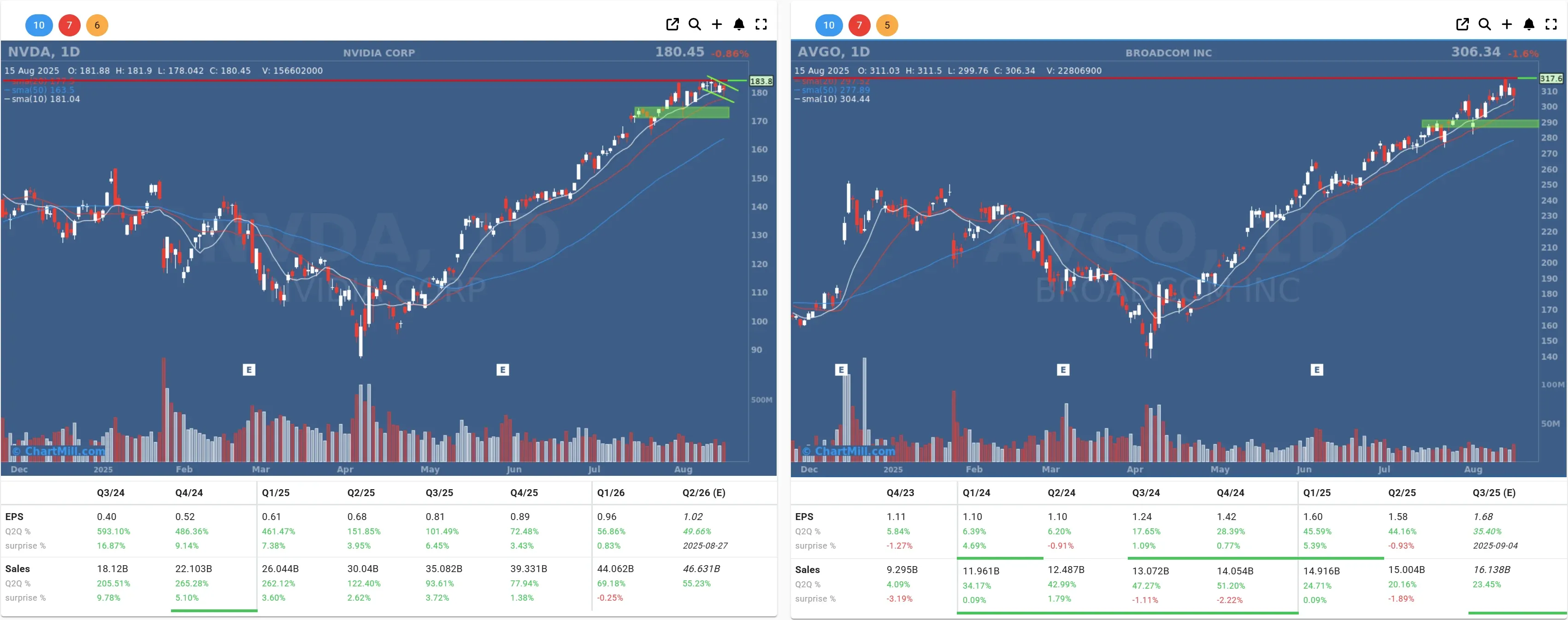

Semis: AMAT’s guidance resets expectations

Applied Materials (AMAT | -14.07%) guided fiscal Q4 revenue to $6.7B (±$0.5B) and non-GAAP EPS $2.11, citing softer China demand and export-approval delays, below Street marks and enough to knock the stock double-digits.

Peers wobbled as well, with weakness spreading to large caps like Nvidia (NVDA | -0.86%) and Broadcom (AVGO | -1.57%).

From my seat, this looks less like “end of the chip cycle” and more like a leading-edge digestion issue, uneven spend and China friction compressing the near-term order book. That’s consistent with the color around older vs. newer nodes and customer pushouts.

Intel: a different kind of catalyst

Intel (INTC | +2.93%) bucked the chip gloom after reports that Washington may take a stake in the company using CHIPS Act mechanisms, an unprecedented twist that would be aimed at onshoring critical capacity.

The stock added ~3% on the chatter. If anything close to this materializes, it would cushion capex risk and re-rate the turnaround narrative.

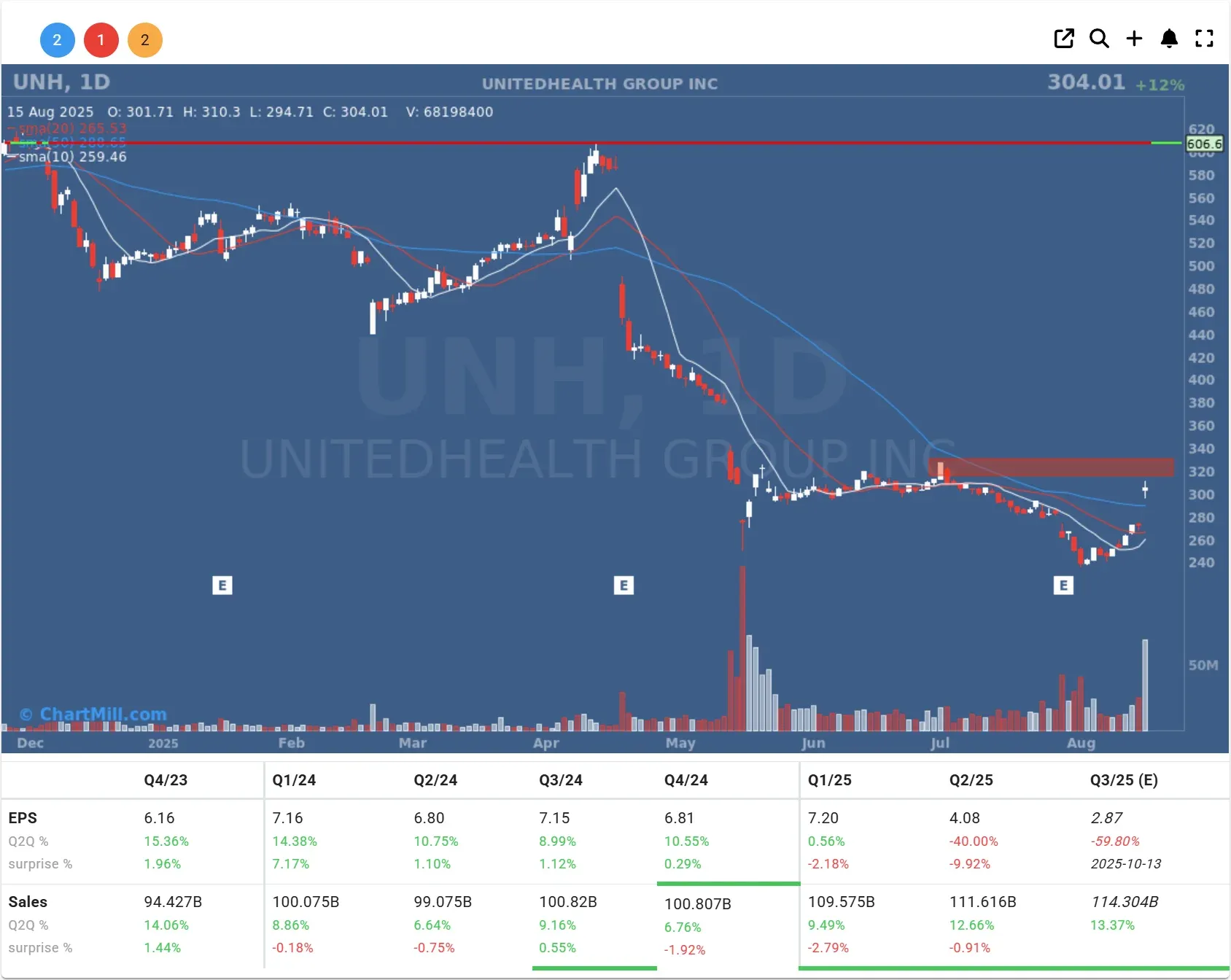

Buffett watch—healthcare pops, builders firm

UnitedHealth (UNH | +11.98%) surged ~12% after Berkshire revealed a new ~$1.6B position.

Berkshire also trimmed Apple and Bank of America while opening/boosting stakes in D.R. Horton (DHI | +1.05%), Lennar (LEN | +1.15%), and Nucor (NUE | +0.73%), a quiet nod to U.S. housing and industrial leverage.

My read: rotating some megacap tech gains into defensives/cyclicals that can grind through a higher-for-longer inflation mix.

Macro: consumers steady, prices firmer

-

Retail sales rose +0.5% m/m in July, with nonstore retail strong, solid, not sizzling.

-

UMich sentiment fell to 58.6 in August as 1-yr inflation expectations ticked up to 4.9% and 5-yr to 3.9%, an uncomfortable combo for doves.

-

PPI jumped +0.9% m/m (fastest in ~3 years), and import prices rose +0.4% m/m, evidence that tariff pass-through is not just a theory.

-

Empire State manufacturing improved to 11.9 in August, but industrial production slipped -0.1% m/m in July; business inventories rose +0.2% in June, up +1.6% y/y.

-

WTI settled at $62.80 and the euro closed near $1.1701, both relevant tells for imported inflation.

Net-net: demand isn’t rolling over, but price pressure is sticky where the Fed least wants it. That keeps September cut odds alive but wobblier, and it explains why markets faded into the weekend.

Geopolitics: Alaska summit, little to show (for now)

The Trump–Putin sit-down in Alaska ended without a Ukraine cease-fire breakthrough, though talks may resume. Oil traders read the outcome as near-term supply-steady, another reason crude drifted lower into the close.

My take

We’re still in a buy-the-dip, verify-the-data regime. If you’re heavy growth, I’d trim froth in semis into strength and recycle a slice into quality healthcare/defensives (yes, even post-pop names like UNH if your horizon is long and you scale entries).

For traders, I’d keep exposure progressive and index-light until we see either PPI/expectations cool or guidance stabilize in semi-equipment.

Kristoff - ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, August 18 BMO