Market Monitor News July 03 BMO (Nike, Verint Systems, Greenbreer UP - Centene DOWN)

By Kristoff De Turck - reviewed by Aldwin Keppens

Last update: Jul 3, 2025

After a day of suspense that felt more like a market thriller than a standard Wednesday session, U.S. equities ended largely in the green.

The S&P 500 hit yet another record, brushing aside weak labor market signals as optimism around a new trade deal with Vietnam lifted spirits and stocks. But beneath the surface, there’s some real tension brewing.

S&P500 Surges to Record Highs (Again), Nasdaq Leads the Way

Let’s not sugarcoat it: the S&P 500 (SPX | +0.5%) is on a tear, closing at a new record of 6,227.42, marking its sixth all-time high this year. The tech-heavy Nasdaq (IXIC | +0.9%) stole the spotlight, pushing to 20,393.13, while the Dow Jones (DJI | flat) didn’t join the celebration and hovered near the unchanged line at 44,484.42.

Interestingly, this relentless climb comes after a sharp drawdown in April, when the market was gripped by fears over Trump’s aggressive tariff rhetoric. Since then? A stunning rebound of nearly 25%. You read that right.

So, what gave markets a boost today despite some glaring cracks in the economic foundation?

Tariff Truce with Vietnam: Relief for Retailers, Muscle for Multinationals

The headline of the day was undoubtedly the U.S.-Vietnam trade agreement. In a statement that could only come from Donald Trump himself, posted on his Truth Social platform, of course, he proclaimed a new deal where Vietnamese goods will face a 20% import tariff and transit goods will be slapped with 40%. That’s a softening compared to the 46% tariff floated just months ago.

In return, Vietnam offers U.S. companies unfettered access to its markets, “zero tariffs,” as Trump triumphantly put it. This pact follows earlier agreements with the UK and China, and with the July 9 tariff pause deadline looming, it’s a signal that the White House is trying to strike deals quickly before that grace period evaporates.

Winners from this deal? Athletic apparel brands with deep supply chain ties to Vietnam. Nike (NKE | +4.06%), Under Armour (UAA | +1.93%), and On Holding (ONON | +2.85%) all surged.

Lululemon (LULU | +0.48%) and Abercrombie & Fitch (ANF | +1.79%) saw smaller gains.

Jobs Data: The First Crack in the Fed’s Patience

On the surface, investors cheered the trade developments. But the real elephant in the room is employment.

The latest ADP report came in… let’s call it disturbing. Private-sector employment fell by 33,000 in June, compared to a modest gain in May and sharply below economists’ expectations for 100,000 new jobs. This is the first contraction in private payrolls in over two years.

According to Chris Zaccarelli of Northlight Asset Management, “If the labor market weakens significantly, the Fed may have no choice but to act sooner than it would like.”

Fed Chair Jerome Powell already told Congress he’s in no rush to cut rates, unless the job market breaks down.

Tomorrow’s official jobs report just became must-watch television for the markets.

Tesla Jumps Despite Weak Deliveries, Centene Gets Crushed

Let’s talk stocks, starting with the good news.

Tesla (TSLA | +4.97%) defied the odds and rallied, even though its Q2 deliveries dropped 13.5% year-over-year.

Why? Simple. Investors had feared worse. When expectations are in the basement, even a weak result can look like a win. The Elon-Trump feud? For now, markets seem to be ignoring the drama.

Meanwhile, Centene (CNC | –40.37%) delivered one of the ugliest days in recent memory, plunging over 40% after pulling its 2025 forecast.

Rising risks in the Affordable Care Act marketplace and regulatory scrutiny hit like a freight train. This was its biggest one-day drop since 2006. Ouch.

In other corporate headlines:

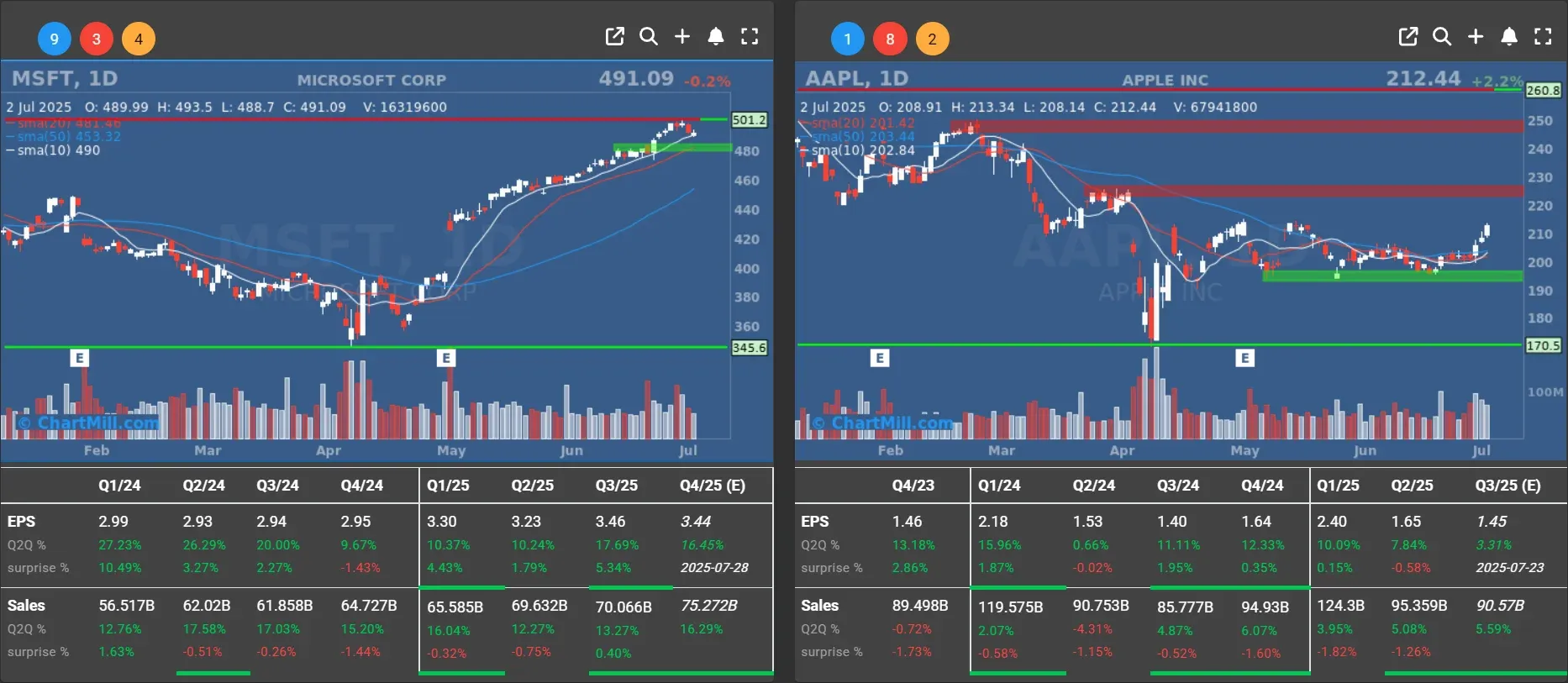

Apple (AAPL | +2.22%) rose after an upgrade from Jefferies. Maybe the fruit’s not so rotten after all.

Microsoft (MSFT | –0.2%) slipped slightly on reports of 9,000 upcoming layoffs.

JP Morgan (JPM | +0.55%) and Morgan Stanley (MS | +1.27%) advanced on new buyback and dividend plans. JPM alone is planning to repurchase $50 billion in stock.

Verint Systems (VRNT | +15.33%) soared on takeover chatter involving Thoma Bravo.

Constellation Brands (STZ | +4.48%) rallied despite disappointing earnings. Booze still sells, apparently.

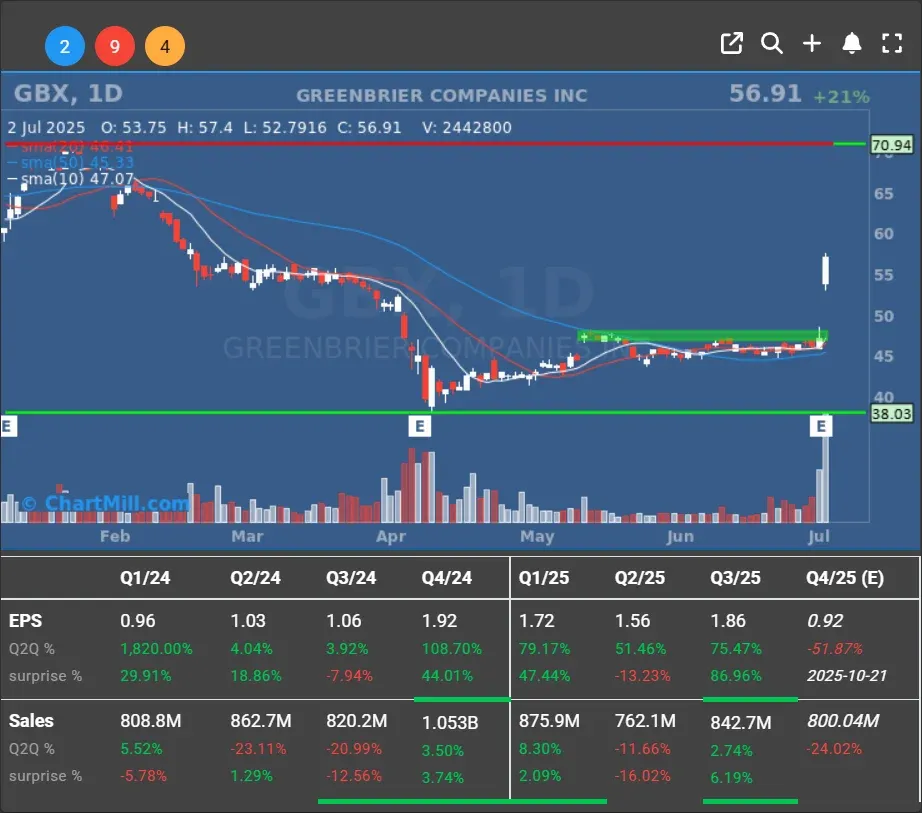

Greenbrier (GBX | +21.09%), a luxury resort operator, flexed with strong profits and revenue growth.

Oil, Currency & What’s Next

Oil prices rebounded sharply, West Texas Intermediate futures closed up 3.1% at $67.45 per barrel, despite rising inventories reported by the EIA. Market logic, right?

The euro strengthened slightly versus the dollar, trading at 1.1797.

As for Thursday? Buckle up. We’ve got six major economic releases before the early holiday close for Independence Day, including the all-important jobs report, jobless claims, and trade balance data.

Final Thoughts

Markets are riding high for now. But let’s not pretend the ADP numbers were a fluke. If the official jobs report confirms labor market weakness, rate cut hopes may finally morph into reality.

That could be good news for equities, but also a flashing yellow light for the economy.

Until then, keep one eye on Vietnam and the other on payrolls. The next few days could be pivotal.

Kristoff - Co-Founder ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, July 02

172.32

-1.55 (-0.89%)

247.68

+1.38 (+0.56%)

6.76

-0.11 (-1.6%)

76.39

0 (0%)

296

+4 (+1.37%)

33.31

-0.47 (-1.39%)

91.6

+1.75 (+1.95%)

56.3

-0.61 (-1.07%)

498.84

+7.75 (+1.58%)

213.55

+1.11 (+0.52%)

315.35

-0.3 (-0.1%)

21.51

+0.07 (+0.33%)

:$APQ (9/2/2014, 6:00:08 PM)

10330

+935 (+9.95%)

Find more stocks in the Stock Screener

STZ Latest News and Analysis

a day ago - ChartmillMarket Monitor News July 03 BMO (Nike, Verint Systems, Greenbreer UP - Centene DOWN)

a day ago - ChartmillMarket Monitor News July 03 BMO (Nike, Verint Systems, Greenbreer UP - Centene DOWN)Wall Street Cheers Tariff Truce, But Will the Jobs Market Spoil the Party?

2 days ago - ChartmillWhich S&P500 stocks are moving on Wednesday?

2 days ago - ChartmillWhich S&P500 stocks are moving on Wednesday?Let's have a look at the top S&P500 gainers and losers one hour before the close of the markets of today's session.

2 days ago - ChartmillUnusual volume S&P500 stocks in Wednesday's session

2 days ago - ChartmillUnusual volume S&P500 stocks in Wednesday's sessionLet's take a look at the S&P500 stocks that are experiencing unusual volume in today's session.

2 days ago - ChartmillExplore the top gainers and losers within the S&P500 index in today's session.Curious about the top performers within the S&P500 index in the middle of the day on Wednesday? Dive into the list of today's session's top gainers and losers for a comprehensive overview.