LULULEMON ATHLETICA INC (NASDAQ:LULU) emerged from our Peter Lynch-inspired stock screen as a potential candidate for long-term growth at a reasonable price (GARP) investors. The company combines solid growth, strong profitability, and financial health, though its valuation requires careful consideration. Below, we break down why LULU fits the criteria.

Growth and Profitability

- EPS Growth (5Y): 24.4% – LULU has delivered consistent earnings growth, well above the 15% minimum threshold in Lynch’s strategy.

- Return on Equity (ROE): 42.0% – This high ROE indicates efficient use of shareholder capital, far exceeding the 15% benchmark.

- Revenue Growth (5Y): 21.6% – The company has expanded its top line at an impressive rate, reflecting strong demand for its athletic apparel.

Financial Health

- Debt-Free Balance Sheet – With a Debt/Equity ratio of 0, LULU carries no debt, a rare strength in its industry.

- Current Ratio: 2.16 – The company comfortably covers short-term obligations, well above the minimum requirement of 1.

- Strong Cash Flow – Positive operating cash flow over the past five years underscores financial stability.

Valuation Considerations

- PEG Ratio (5Y): 6.66 – This elevated PEG suggests the stock is priced for high growth, which may concern value-focused investors.

- P/E Ratio: 20.7 – While above the industry average, LULU’s premium valuation aligns with its superior profitability and growth prospects.

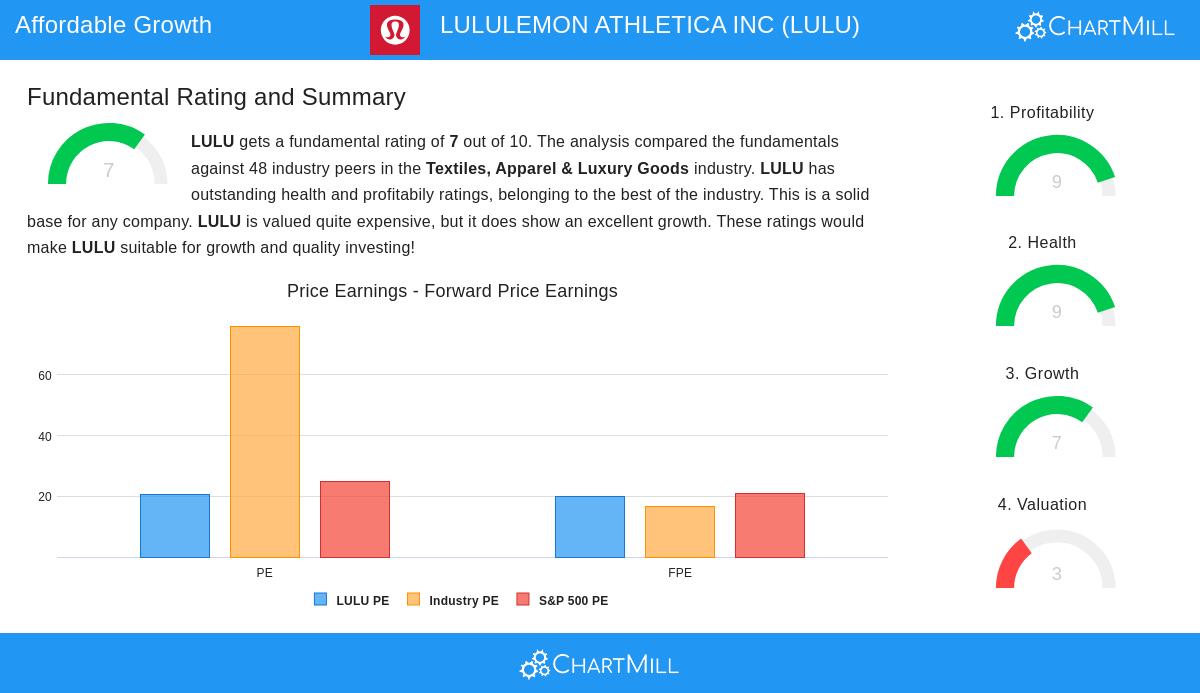

Fundamental Report Highlights

LULU earns a fundamental rating of 7/10, with top marks in profitability (9/10) and financial health (9/10). Its growth metrics are strong, though future estimates show a slight moderation in revenue and EPS expansion. For a deeper look, review the full fundamental analysis here.

Our Peter Lynch Strategy screener lists more stocks matching these criteria and is updated regularly.

Disclaimer

This is not investment advice. The observations here are based on data available at the time of writing. Always conduct your own research before making investment decisions.