For investors looking for a disciplined, long-term way to build wealth, few strategies hold the authority of Peter Lynch’s method. The famous manager of the Fidelity Magellan Fund supported investing in what you understand, concentrating on companies with clear operations, durable growth, and good finances, all while trading at a sensible price. This "growth at a reasonable price" (GARP) idea steers clear of the limits of speculative growth pursuit and deep-value discount searching, instead looking for good companies that can increase returns over many years. A filter built on Lynch's main rules, which include earnings growth, price assessment, profit generation, and financial strength, can reveal possible choices for this kind of portfolio.

One company that recently appeared from this filter is Lululemon Athletica Inc (NASDAQ:LULU). The Vancouver-based seller of performance athletic wear and items has grown into a leading brand in its category. But does its financial picture match the ideas of a long-term, Lynch-like investment? An examination of the specific filter rules and the company's wider basic factors indicates it deserves more attention from GARP-focused investors.

Match with Peter Lynch's Main Rules

The Peter Lynch filter uses particular, measurable checks to find companies with a mix of growth and sensible price. Lululemon's present numbers show a good match with these rules:

- Durable Earnings Growth: Lynch preferred companies increasing earnings per share (EPS) between 15% and 30% each year over a five-year span, quick enough to be a frontrunner, but not so fast that the speed is unstable. Lululemon's five-year EPS growth rate of 24.37% fits well within this goal range, pointing to a record of strong, yet possibly steady, increase.

- Sensible Price Assessment via PEG Ratio: Maybe the central part of Lynch's price check is the Price/Earnings to Growth (PEG) ratio. A PEG of 1 or less indicates the stock's price is sensible compared to its growth rate. Lululemon's PEG ratio, using its past five-year growth, is 0.60, suggesting the market may not completely account for its historical growth path.

- High Profit Generation (ROE): Lynch demanded a high return on equity (ROE) as a mark of an effective and profitable operation. He looked for at least 15%. Lululemon greatly passes this barrier with an ROE of 38.67%, showing outstanding skill to create profits from shareholder equity.

- Careful Financial Strength: The filter requires a debt-to-equity ratio below 0.6 (Lynch individually liked below 0.25) and a current ratio above 1 to confirm short-term ability to pay. Lululemon performs well here, having a debt-to-equity ratio of 0.0, meaning it functions with no interest-bearing debt, and a sound current ratio of 2.13.

These numbers together create a portrait of a company that has grown earnings at a solid rate, keeps outstanding profit generation and a very strong balance sheet, and trades at a price that seems sensible when its growth is considered, a main idea of the GARP method.

Wider Basic Condition Review

While the filter gives a useful initial check, Lynch stressed the need for more detailed examination. A look at Lululemon's full basic report supports the positive signs.

The company gets a good total basic rating of 6 out of 10. Its strong points are especially clear in two areas important for long-term investors:

- Profit Generation Leader: With a profit generation score of 8/10, Lululemon is notable. Its profit margin (15.72%), operating margin (22.05%), and return on invested capital (28.30%) all place in the high group of its industry, supporting Lynch's focus on high-margin, effective businesses.

- Outstanding Financial Strength: The company reaches a strength score of 8/10. The lack of debt is a key reason, but it is helped by a strong Altman-Z score (7.83) showing very low failure risk and a steady record of share count decrease through buybacks, another factor Lynch saw as good.

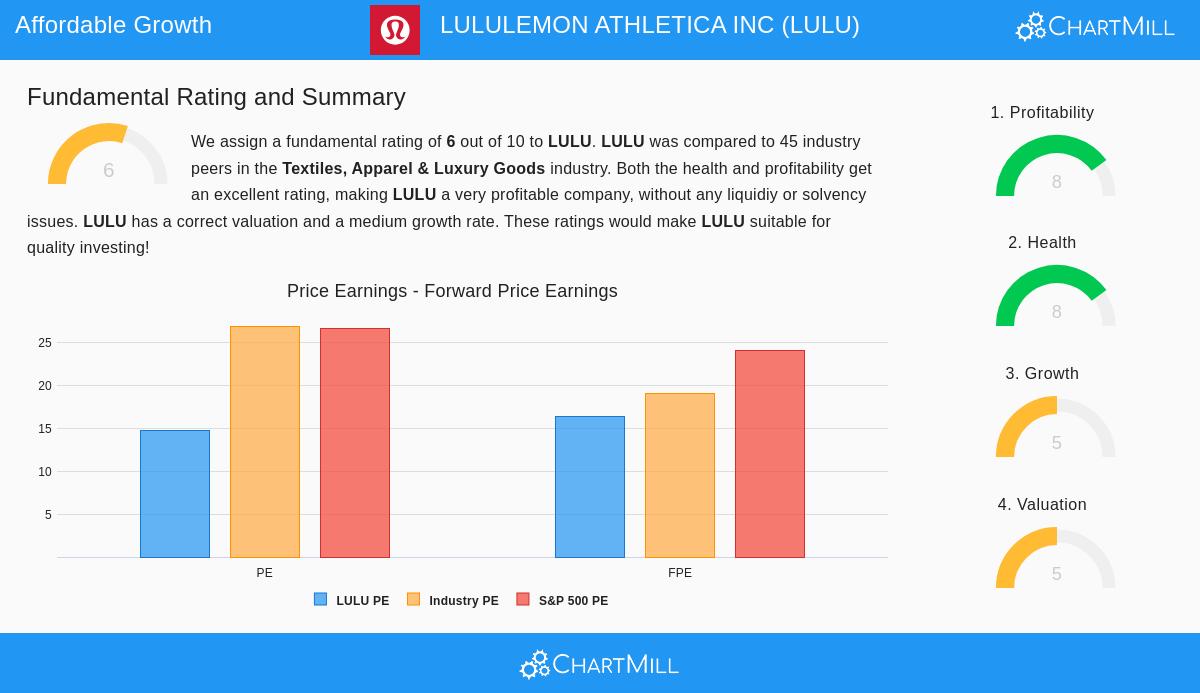

The price assessment view is mixed but tends positive. With a P/E ratio near 14.7, Lululemon is priced lower than the wider S&P 500 and most of its industry peers. The primary note of care is in the growth forecast. While past growth has been excellent, experts predict a notable slowdown in both revenue and EPS growth in the next few years. For a Lynch investor, this highlights the need for study: knowing why growth is expected to slow and judging whether the company can discover new paths for growth is key before making a long-term decision.

Is Lululemon a Lynch-Like "GARP" Choice?

Based on the measurable filter and basic review, Lululemon Athletica makes a strong case for investors using a Peter Lynch-inspired GARP plan. It meets the necessary marks: a strong brand in a clear business (athletic wear), a long history of shown high-quality growth, top-level profit generation, and a clean balance sheet. Most importantly, its present price, as measured by the PEG ratio, does not seem to require perfection, offering a possible buffer.

The filter that found Lululemon is built on the proven ideas of Peter Lynch. You can discover more possible choices that fit this "growth at a reasonable price" description by checking the Peter Lynch Strategy screen. Keep in mind, a filter is a beginning step for study, not a list of purchases. Any investment needs complete inquiry into the company's business model, competitive edges, and future possibilities.

,

Disclaimer: This article is for information only and does not make up financial guidance, a suggestion, or an offer to buy or sell any security. The review is based on data and a particular investment plan filter, investors should do their own examination and think about their personal financial situation before making any investment choices.