Strong Growth Data, Weak Market Mood

Wall Street closed lower across the board: the Dow Jones fell 0.4% and the Nasdaq lost 0.5%.

Ironically, the trigger wasn’t bad economic news but rather stronger-than-expected growth. The U.S. economy expanded 3.8% in Q2 (annualized), well above the prior 3.3% estimate. Consumer spending was revised up sharply to 2.5% (from 1.6%), and business investment surged 7.3%, powered in part by AI-driven data center demand.

That all sounds positive, but here’s the catch: solid growth and sticky inflation reduce the likelihood of further Fed rate cuts this year. Treasury yields climbed, and futures markets pared back bets on two additional cuts before year-end.

Company Highlights

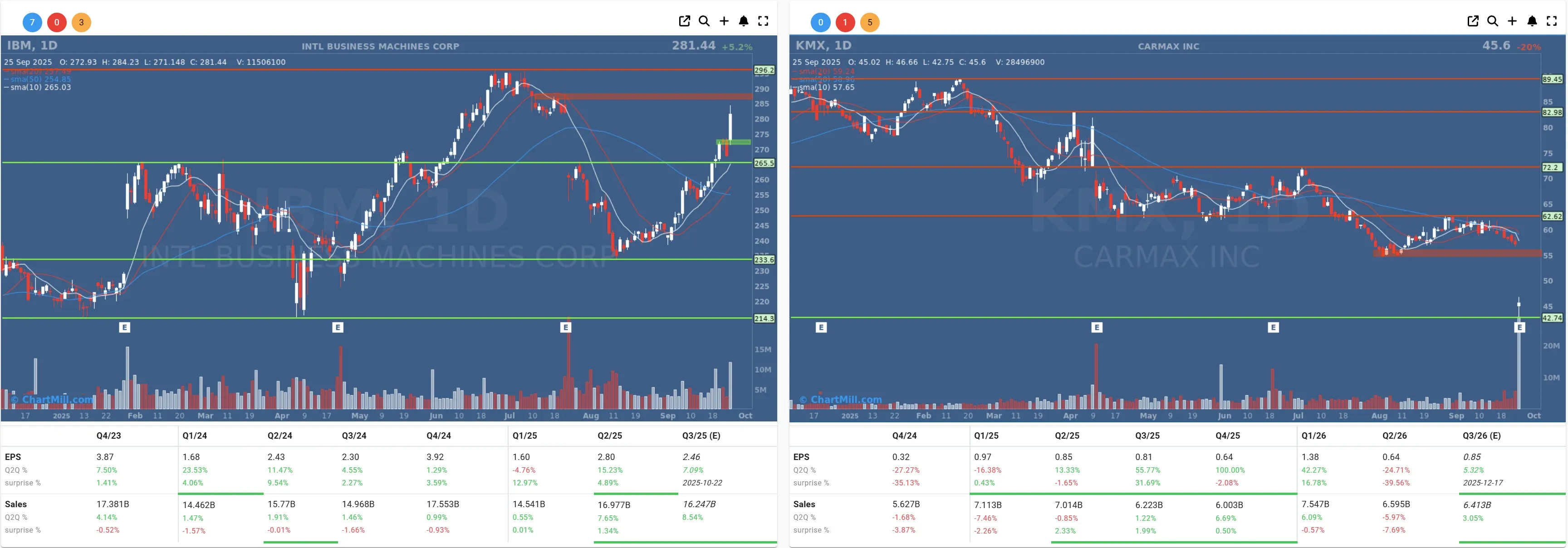

IBM (IBM | +5.2%) popped after HSBC announced a breakthrough in applying its Heron quantum processor to financial market predictions.

Tests reportedly improved bond price forecasting by 34%. While it sounds flashy, some experts dismissed it as more milestone than market mover. As one fund manager quipped: “Storm in a teacup.” Investors didn’t mind; they happily bid up the stock.

Used-car retailer CarMax (KMX | -20.07%) crashed after reporting a 6.3% drop in same-store sales for Q2.

EPS came in at $0.64, far below consensus of $1.03. Analysts at Wedbush slashed their target from $84 to $54, warning that the company is losing market share faster than expected.

JPMorgan echoed the disappointment. It was one of the day’s biggest losers on Wall Street.

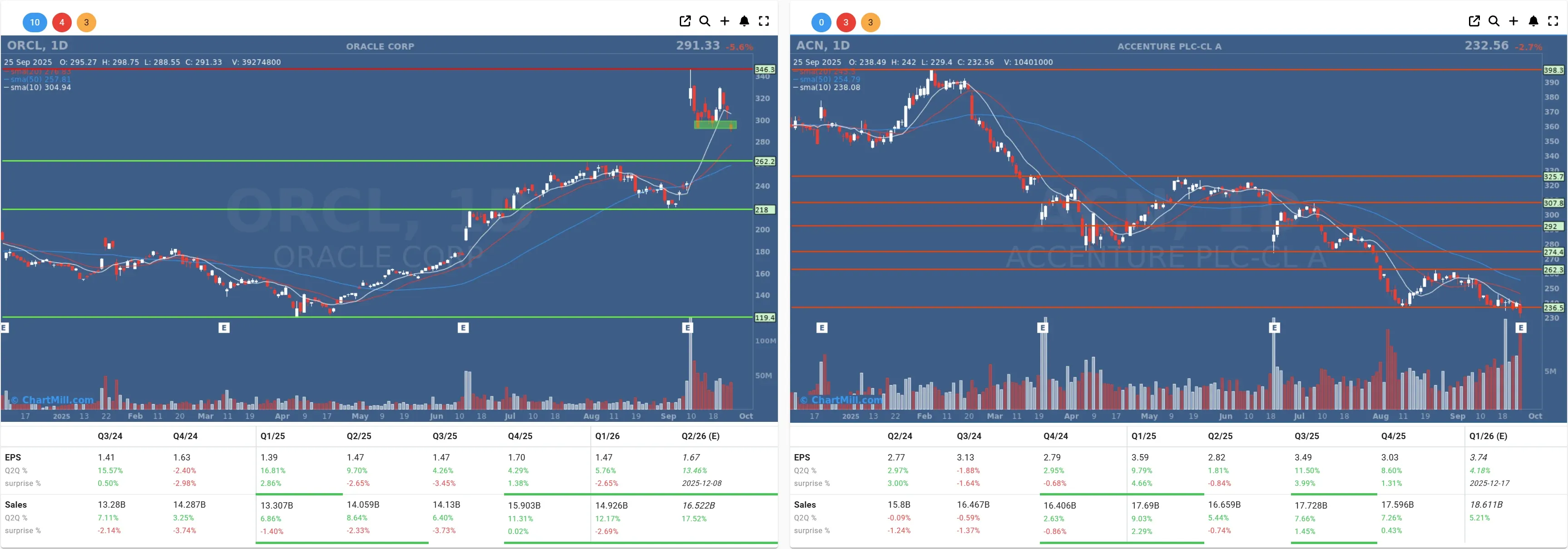

Consulting giant Accenture (ACN | -2.73%) flagged slower growth for fiscal 2026 due to U.S. government budget tightening.

The impact could trim 1–1.5% off annual revenue. Still, Q4 looked solid with revenue up 7% to $17.6B and EPS at $3.03, slightly ahead of estimates. AI-related bookings remain a bright spot, but cautious guidance kept shares under pressure.

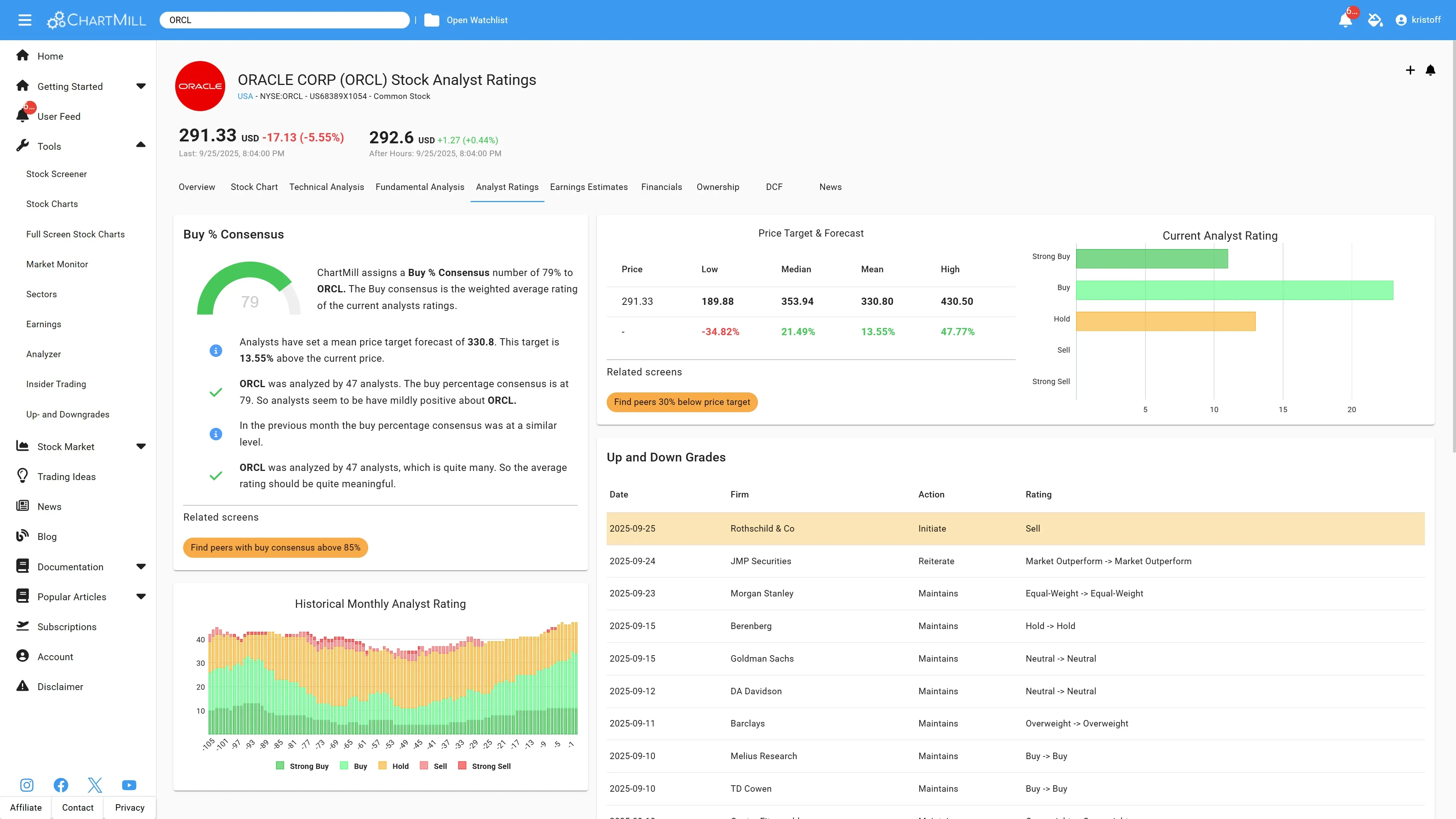

Oracle (ORCL | -5.55%) slid after Rothschild & Co Redburn initiated coverage with a “Sell” rating and a $175 price target, nearly 40% below current levels. Analysts argued the market overestimates Oracle’s cloud revenue potential.

The stock may also have been hit by reports linking Oracle to the TikTok U.S. spin-off deal.

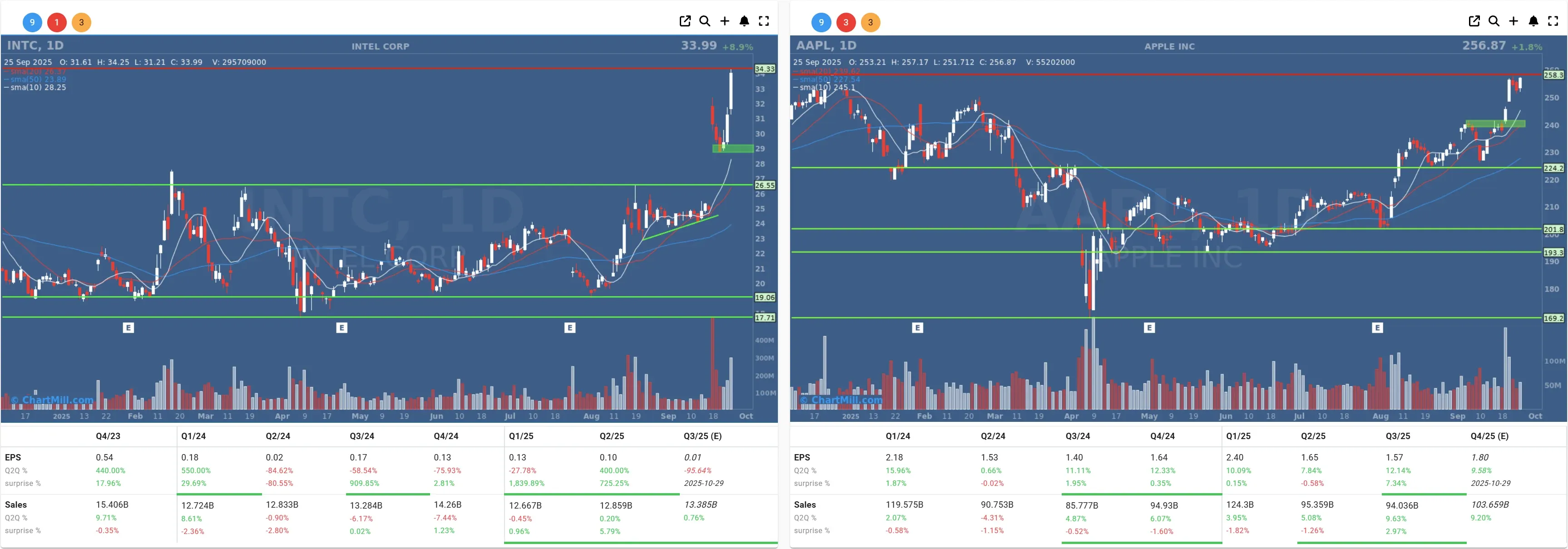

Intel (INTC | +8.87%) jumped after Bloomberg reported early talks with Apple (AAPL | +1.81%) about investment and deeper cooperation. The news sparked hopes of stabilization for Intel’s struggling foundry ambitions.

Macro & Commodities

-

Jobless claims fell to 218,000 - the lowest since July - signaling resilience in the labor market.

-

Durable goods orders rose 2.9% in August, surprising to the upside.

-

Core PCE inflation for Q2 was revised slightly higher at 2.6%. Investors now look to the August PCE release on Friday.

-

Dollar strength: EUR/USD slipped under 1.17.

-

Treasuries: the 10-year yield pushed up to 4.175%.

-

Commodities: Oil paused after recent gains; silver hit a 14-year high, while gold cooled slightly below its recent peak.

Geopolitical Spotlight: TikTok Deal Moves Forward

President Trump signed an executive order approving the sale of TikTok’s U.S. operations to a consortium led by Oracle’s Larry Ellison, with backing from Silver Lake and Abu Dhabi’s MGX. ByteDance will retain a minority stake of 19.9%, while leasing its algorithm under U.S. oversight.

Valuation of the new entity is pegged at $14 billion. Legal and regulatory hurdles remain, but the path is clearer than before.

My Take

Markets don’t like “too good to be true.” Strong GDP should be a win, but traders see it as a Fed headache.

Combine that with mixed corporate earnings and a TikTok sideshow, and it’s no wonder indexes stalled.

Kristoff - ChartMill

Next to read: Market Breadth Weakens Sharply as Decliners Dominate