Value investing relies on finding stocks priced below their true value while showing good financial stability and earnings. One way to spot these opportunities is by looking for companies with strong valuation scores (a ChartMill Valuation Rating higher than 7) paired with steady growth, earnings, and financial strength. This method confirms the stock isn’t just low-priced but also fundamentally strong, a core idea in Benjamin Graham’s value investing approach.

Incyte Corp (NASDAQ:INCY) appears to meet these standards. The biopharmaceutical firm, specializing in cancer and inflammation treatments, has a Valuation Rating of 9/10, indicating it trades at a notable discount compared to similar companies. Its Profitability (7/10) and Health (7/10) scores point to efficient operations and a solid financial position, while a Growth Rating of 5/10 suggests steady, though not rapid, expansion potential.

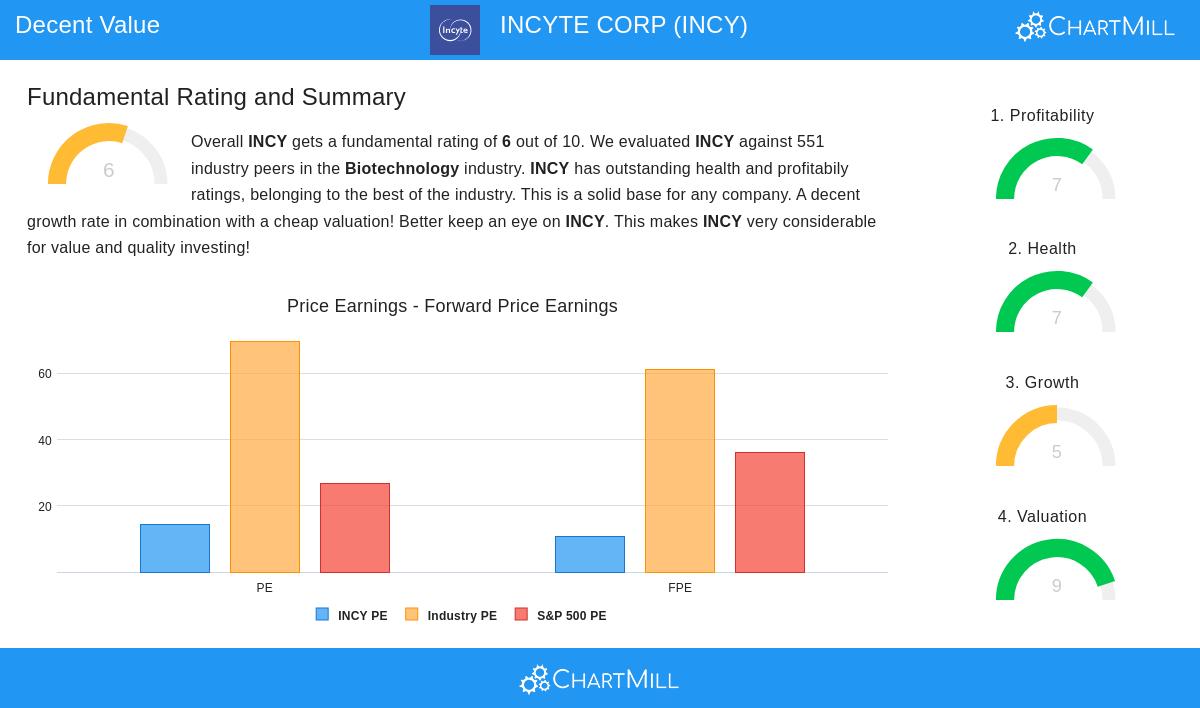

Valuation: A Strong Discount

Incyte’s valuation numbers are notable:

- P/E Ratio of 14.45 is much lower than the industry average (69.77) and the S&P 500 (26.82), making it cheaper than 95% of biotech competitors.

- Forward P/E of 10.84 reinforces its discounted price, trading far below the sector’s 61.27 average.

- Enterprise Value/EBITDA and Price/Free Cash Flow ratios are also attractive, ranking above 92% of peers.

For value investors, these figures suggest a possible safety margin—a central concept in value investing. The low multiples imply the market might be underestimating Incyte’s earnings and cash flow prospects.

Financial Health: A Stable Position

Incyte’s Health Rating of 7/10 reflects reliability:

- Altman-Z Score of 5.31 shows low bankruptcy risk, better than 77% of the industry.

- Debt/Equity of 0.01 and Debt/FCF of 0.12 reveal minimal debt and strong solvency.

- Liquidity is sufficient, with a Current Ratio of 2.04, though slightly below industry averages.

A sturdy financial position lowers risk, matching value investing’s focus on protecting capital.

Profitability: Effective Operations

Despite some margin pressure, Incyte’s Profitability Rating of 7/10 highlights positives:

- ROA (0.37%) and ROE (0.58%) rank in the top 10% of biotech companies.

- Operating Margin of 5.39% beats 92% of peers, though it has declined year-over-year.

- Gross Margin of 93.19% remains among the best in the industry, showing pricing strength.

High profitability relative to valuation hints the stock might be undervalued—a key target for value investors looking for quality at a lower price.

Growth: Uneven but Promising

Incyte’s Growth Rating of 5/10 reflects mixed results:

- Revenue increased 18.88% YoY, with a 14.46% 5-year CAGR, but future estimates show a slight drop (-0.42%).

- EPS jumped 433.67% YoY, though long-term trends (-14.21% CAGR) and drug approval cycles affect consistency.

While growth isn’t outstanding, the valuation more than makes up for modest progress, a balance value investors often accept.

Conclusion

Incyte Corp offers a strong case for value investors: priced well below its earnings and cash flow potential, yet financially stable and profitable. Its focus on biotech adds growth potential, though sector risks (e.g., patent expirations, R&D uncertainty) require attention.

For investors searching for similar opportunities, discover more undervalued stocks using the Decent Value Stocks screener.

Disclaimer: This analysis is not investment advice. Conduct your own research or consult a financial advisor before making decisions.