Let’s be honest, what started as a mild summer trading day turned into a rollercoaster of Fed fears, pharma fireworks, and political drama that would make even Netflix jealous.

Here's what you need to know to keep your portfolio aligned with the latest twists in the market.

Fed Frenzy: Powell’s (Non-)Exit Sends Shockwaves

Midday Wednesday, Wall Street collectively clenched when headlines hit suggesting President Donald Trump was prepping to fire Fed Chair Jerome Powell. Stocks nosedived in a flash, with traders fearing a political hijack of monetary policy.

But just as fast as the fear spread, it faded, Trump later clarified that he had no concrete plans to remove Powell, calling such a move “very unlikely... unless he commits fraud.”

Still, the market’s knee-jerk reaction told us everything: Powell is seen as a stabilizing figure, and investors aren’t ready to play roulette with Fed independence.

Meanwhile, Trump’s call for a 3-point rate cut remains... aggressive. Powell, on the other hand, noted that the Fed might have eased earlier if Trump’s tariff policies hadn’t stoked inflation. Touché, Jay.

Economic Pulse: Inflation Eases, Production Picks Up

On the macro front, producer prices came in flat for June, a welcome surprise against expectations of a 0.3% increase. That’s a small win for those worried about Trump’s tariffs fanning inflation flames. But let’s not break out the champagne just yet, consumer data still shows rising prices on tariff-sensitive goods like furniture and toys.

Also worth noting: industrial production rose by 0.3% in June, outpacing expectations. The Beige Book painted a picture of a U.S. economy still trudging forward, modest growth, stable employment, and tempered price increases.

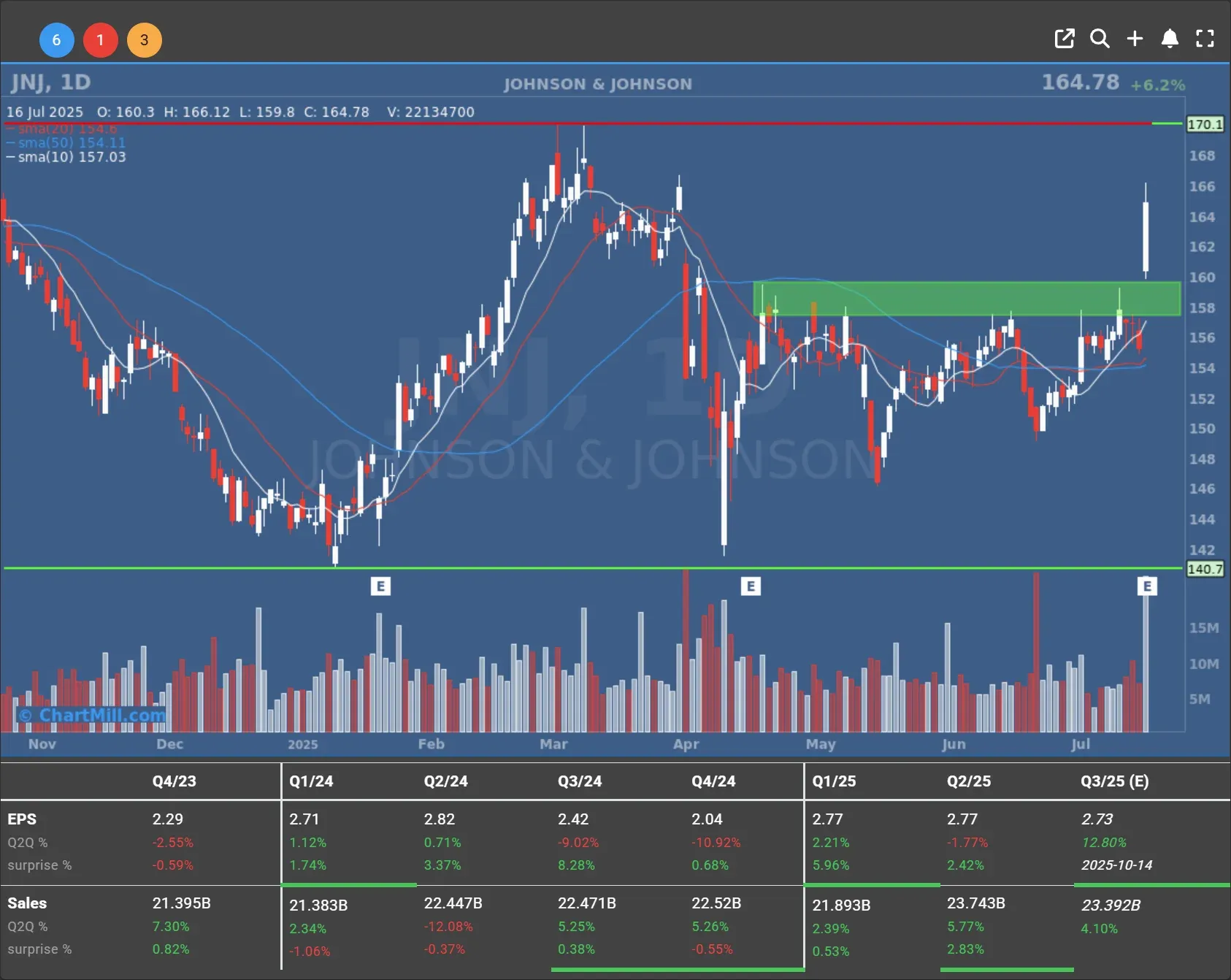

Johnson & Johnson Delivers the Goods

Pharma heavyweight Johnson & Johnson (JNJ | +6.19%) was the undisputed MVP of the day. Fueled by robust demand for its cancer drug Darzalex, J&J posted stronger-than-expected results and raised its full-year guidance.

Revenue is now expected to reach between $93.2B and $93.6B, up from $91B–$92B, with EPS projected at $10.80–$10.90.

In short, the drugmaker is firing on all cylinders.

Gunpowder and Politics: GrabAGun’s Rough Start

Elsewhere, GrabAGun (PEW | -24.20%) made its Wall Street debut with a resounding thud. Despite the high-profile support from Donald Trump Jr. - who rang the NYSE opening bell - the firearm e-commerce firm plunged over 24% on day one.

Backed by a SPAC and now valued at roughly $300 million, PEW’s ticker may be clever, but its market debut was anything but.

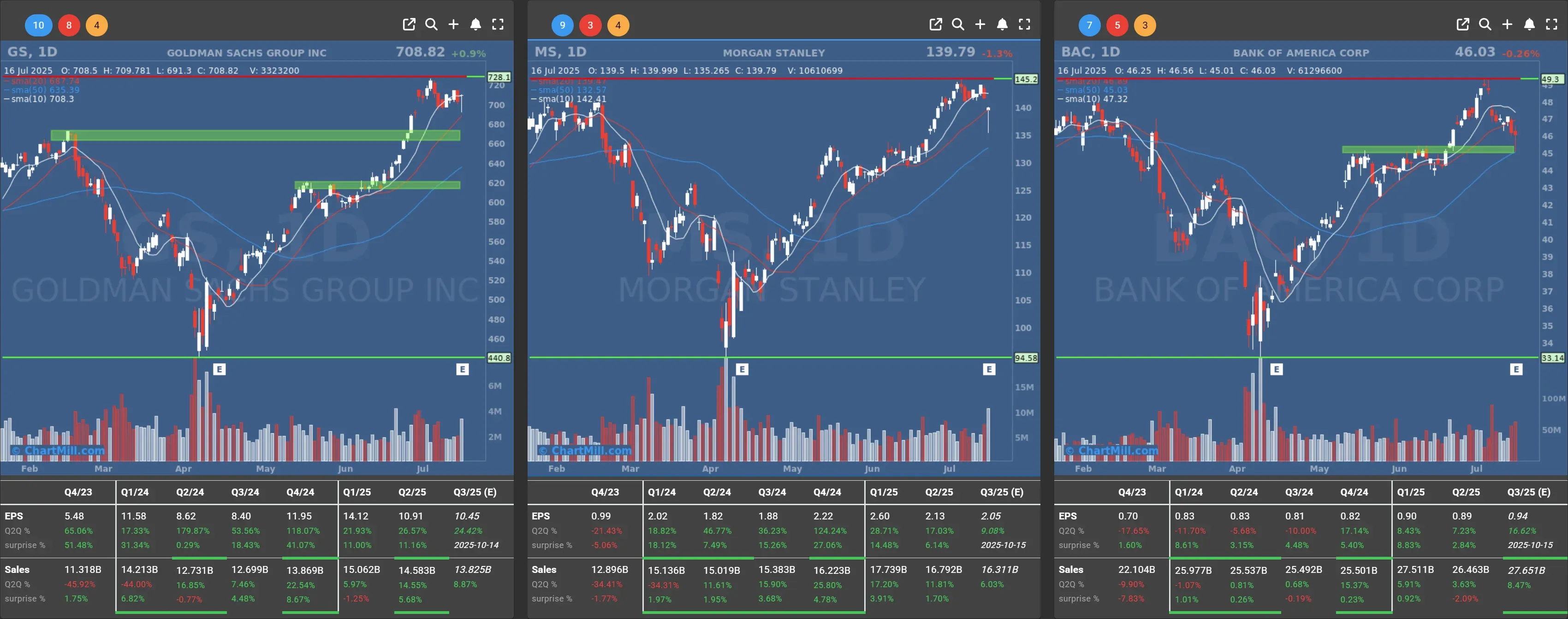

Bank Earnings: Mixed Bag for Wall Street Giants

-

Goldman Sachs (GS | +0.9%) impressed, with Q2 EPS of $10.91, beating expectations by a wide margin. Revenue rose 15% to $14.6B, about $1B above the Street’s forecast. Not bad at all.

-

Bank of America (BAC | -0.26%) didn’t fare as well. Even though consumer health remains “resilient,” according to CEO Brian Moynihan, the stock dropped slightly after earnings.

-

Morgan Stanley (MS | -1.27%) beat profit forecasts but still fell, suggesting investors wanted more upside than what was delivered.

Deal Talk: Brighthouse Financial Pops

Brighthouse Financial (BHF | +6.23%) surged after The Wall Street Journal reported that Aquarian Holdings is in exclusive talks to acquire the life insurer. No deal yet, but traders are betting on it.

United Airlines Soars... Then Descends

United Airlines (UAL | +2.42%) posted solid earnings (Q2 EPS of $3.87 vs. $3.81 expected) but cut full-year guidance to $9–$11 per share, lower than the $10 consensus.

Domestic pricing pressures and a 26% drop in net income didn’t help sentiment.

Still, CEO Scott Kirby struck a hopeful tone, saying “the world is less uncertain than it was six months ago.” Take that as you will.

Energy and Forex: Oil Slides, Euro Fluctuates

WTI crude (66.35 USD | -0.30%) slipped slightly despite a 3.4M barrel draw in U.S. crude inventories. Meanwhile, the euro saw a volatile session, settling at $1.1648 as traders weighed shifting inflation data and interest rate expectations.

Final Take

Wednesday reminded us that even in midsummer, markets don’t nap. Between potential Fed chair shakeups, big pharma surprises, and the debut of politically charged companies, volatility remains a loyal companion.

My advice? Stay nimble. We’re still navigating a market balancing strong corporate fundamentals against rising political unpredictability. That’s a recipe for both opportunity and whiplash.

Until tomorrow, stay sharp out there.

Kristoff - ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, July 17