Alphabet Inc-CL C (NASDAQ:GOOG) Fits Peter Lynch's Growth at a Reasonable Price (GARP) Strategy

By Mill Chart

Last update: Aug 16, 2025

Peter Lynch’s investment approach, detailed in One Up on Wall Street, centers on finding companies with steady growth at fair prices—commonly known as the Growth at a Reasonable Price (GARP) method. The strategy highlights financial stability, earnings strength, and controlled debt, steering clear of overly hyped or rapidly expanding businesses that might face challenges sustaining their pace. By looking for firms with solid but not excessive earnings growth, strong financial positions, and appealing valuations compared to growth (using measures like the PEG ratio), Lynch’s method seeks to identify long-term successes.

One stock that aligns with this model is ALPHABET INC-CL C (NASDAQ:GOOG), the parent company of Google. Alphabet matches several important criteria from Lynch’s strategy, making it an attractive option for GARP-focused investors.

Why Alphabet Matches the Peter Lynch Standards

-

Steady Earnings Growth

- Lynch preferred firms with reliable but not extreme earnings growth, usually between 15% and 30%. Alphabet’s EPS has increased at an average yearly rate of 25.25% over the past five years—fitting well within Lynch’s ideal range.

- Projected EPS growth remains solid at 15.78%, showing the company is growing at a sustainable pace without overheating.

-

Fair Valuation Compared to Growth (PEG Ratio)

- A key Lynch measure is the PEG ratio, which accounts for growth when evaluating the P/E ratio. A PEG under 1 suggests a stock may be priced below its growth potential. Alphabet’s PEG ratio is 0.92, indicating its earnings growth is not fully priced in.

- This matches Lynch’s view that investors should pay a fair price for growth rather than overpay for high-growth stocks.

-

High Profitability (ROE & Margins)

- Return on Equity (ROE) reflects efficient use of capital. Alphabet’s ROE of 31.85% surpasses Lynch’s 15% benchmark and beats 94% of its peers in the Interactive Media & Services sector.

- The company also maintains strong operating (33.53%) and profit margins (31.12%), showing its ability to turn revenue into earnings effectively.

-

Solid Financial Position (Low Debt, Good Liquidity)

- Lynch favored firms with little debt to avoid financial stress. Alphabet’s Debt/Equity ratio of 0.07 is well below the screener’s 0.6 limit—and even under Lynch’s stricter preference for ratios below 0.25.

- Its Current Ratio of 1.90 shows it has enough liquidity to meet short-term obligations, lowering operational risks.

-

Other Advantages (Cash Flow, Share Buybacks)

- Alphabet produces significant free cash flow, with a Debt-to-FCF ratio of just 0.40, meaning it could clear all debt in under six months using cash flow alone.

- The company has also been reducing shares outstanding through buybacks, another Lynch-approved practice, as it reflects confidence in the business and improves per-share metrics over time.

Fundamental Review Summary

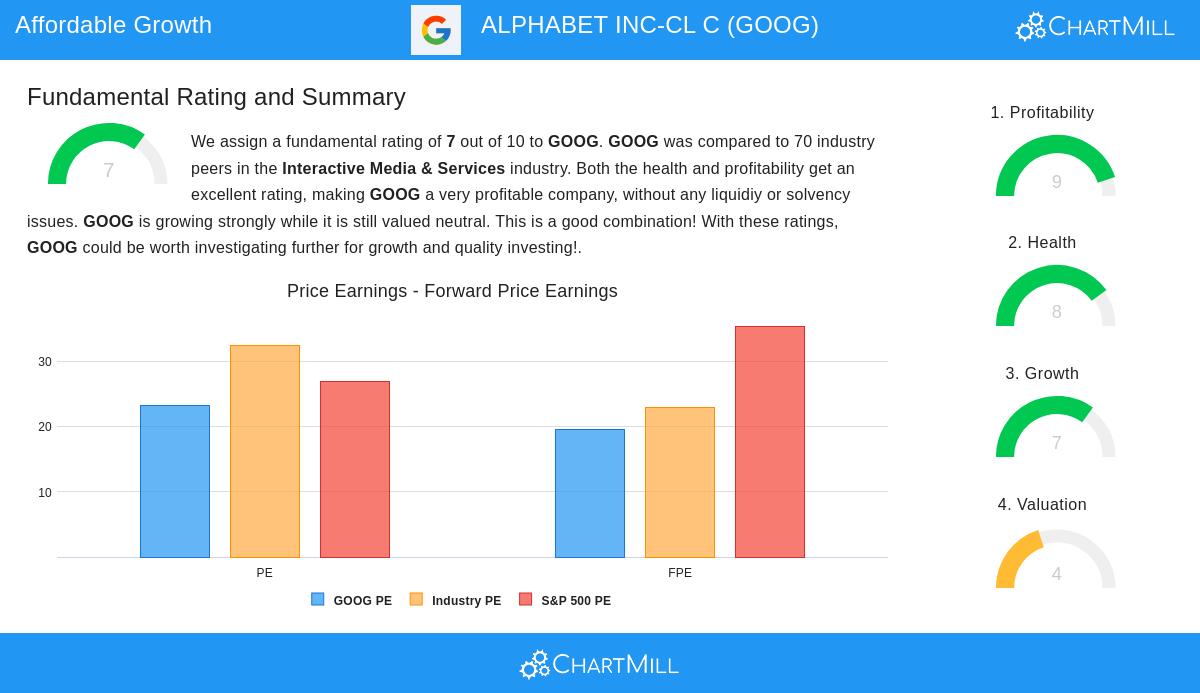

Alphabet’s fundamental report gives it a 7/10 score, emphasizing its outstanding profitability, financial stability, and growth outlook. While its P/E ratio (23.15) may seem slightly high, this is supported by its high-quality earnings, sector-leading margins, and consistent growth path. The report states that Alphabet’s valuation is fair relative to both its industry and the S&P 500, especially when considering its growth potential.

Finding More Peter Lynch Screen Picks

For investors looking for other stocks that fit Lynch’s approach, the Peter Lynch Stock Screener offers a selected list of companies meeting these standards.

Final Thoughts

Alphabet’s mix of consistent earnings growth, high profitability, careful financial management, and fair valuation makes it a strong choice for investors following Peter Lynch’s GARP principles. While no investment is risk-free, the company’s leading role in digital advertising, cloud computing, and AI innovation suggests it is well-placed for long-term growth.

Disclaimer: This article is not investment advice. Always conduct your own research or consult a financial advisor before making investment decisions.

244.36

-2.82 (-1.14%)

Find more stocks in the Stock Screener

GOOG Latest News and Analysis