In the hunt for investment chances, many experienced investors look to the ideas of value investing. This established method, supported by people like Benjamin Graham and Warren Buffett, centers on finding companies whose share price is lower than their calculated real worth. The aim is to buy these "undervalued" securities and keep them until the market adjusts its valuation, hoping to gain from the coming together of price and value. A frequent way to locate these possibilities is to filter for stocks with good basic foundations, like earnings and balance sheet strength, that are also selling at good price ratios. This technique aims to sidestep "value traps," or firms that are inexpensive for a cause, by confirming the business itself is stable.

Expedia Group Inc. (NASDAQ:EXPE) recently appeared from such a filtering process, which looked for firms with a good basic valuation rating while also showing acceptable scores for expansion, earnings, and balance sheet strength. An examination of the company's detailed basic report shows why it may deserve more attention from investors using this structured method.

Valuation: A Central Support for Value Investors

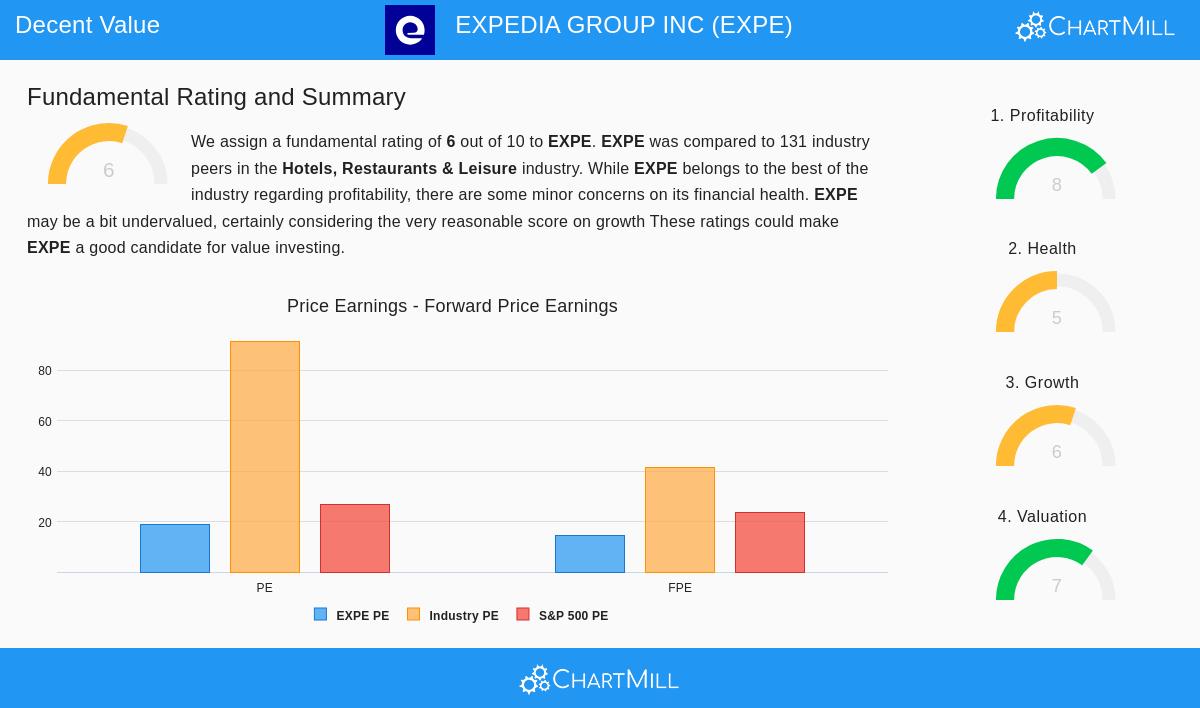

For a value investor, a good price is the starting place. It shows the possible difference from real worth. Expedia's basic report gives it a Valuation Rating of 7 out of 10, meaning it is valued lower than many similar companies.

- Price-to-Earnings (P/E) Setting: While Expedia's own P/E ratio of 18.77 might not immediately seem like a "deal," the setting is important. This number is lower than about 70% of firms in the Hotels, Restaurants & Leisure field, which has an average P/E above 90. Also, it is below the S&P 500 average of 26.59.

- Future and Cash Flow Measures: More interesting are the forward P/E of 14.68 and the Price-to-Free Cash Flow ratio. The forward P/E is lower than 74% of field peers, and the cash flow multiple puts Expedia in the least expensive 10% of its industry. This hints the market is not completely valuing the company's future earnings ability or its good cash production.

- Growth Adjustment: The low PEG ratio, which changes the P/E for anticipated earnings expansion, shows the stock's price is fair compared to its growth path. With earnings forecast to increase almost 23% in the near future, the current cost may not include this possible rise.

This mix of comparative and absolute price measures fits with the value investing rule of looking for a "margin of safety"—buying at a cost low enough below calculated worth to allow for mistakes in calculation or unexpected market changes.

Earnings and Expansion: The Driver Behind the Price

An inexpensive stock is only a wise investment if the company is basically stable and able to expand. A low price combined with good earnings can point to a notable chance. Expedia does well here, getting a high Earnings Rating of 8.

- Notable Results: The company produces notable results on its invested money. Its Return on Equity (ROE) of over 103% and Return on Invested Capital (ROIC) of 18.46% put it in the best group of its field, doing better than over 90% of rivals. This shows management is very good at creating earnings from shareholder equity and capital investments.

- Good and Increasing Margins: Expedia has a strong Gross Margin of nearly 90%, a sign of its asset-light online travel platform structure. Both its Operating Margin (13.72%) and Profit Margin (9.66%) have shown upward movement in recent years and compare well to the field average. For a value investor, this steady and high-level earnings gives trust that the business model is lasting and can aid future expansion.

- Growth Path: The Expansion Rating of 6 is backed by a good history and positive view. Earnings Per Share (EPS) increased over 26% in the last year and is expected to keep increasing at a high speed. Importantly, experts predict that both EPS and sales growth will speed up in the near future compared to the past. This forward movement is key, as value investing is not about buying still companies; it is about buying growing companies at a lower price.

Balance Sheet Strength: Checking the Financial Risk

Balance sheet strength is the protection in the value calculation. It makes sure the company can handle economic drops and keep running without trouble. Expedia's Strength Rating of 5 shows a varied but workable situation, which is why the filtering rules asked for "acceptable" instead of "outstanding" strength.

- Stability Positives: The company creates notable value, with its ROIC much higher than its cost of capital. Its debt compared to its free cash flow is low, meaning it could settle its debts in slightly more than two years—a ratio that does better than 83% of the field. This good free cash flow production is a main factor against balance sheet worries.

- Cash and Debt Points: The main points for care are a high Debt-to-Equity ratio and low Current and Quick Ratios, which suggest less-than-perfect immediate cash availability. However, the report explains this by stating the high earnings and good free cash flow can maintain this setup, especially if the debt amount is from actions good for shareholders like share repurchases. For a value investor, this highlights the need for a complete view: the company's effective cash source helps balance the debt on its balance sheet.

Conclusion

Expedia Group offers a situation where the market's present valuation may not fully include the company's basic positives. Its notable earnings, speeding growth outline, and good cash flow production are matched with price ratios that are good compared to both its field and the wider market. While investors should thoughtfully review the company's debt and cash measures, its overall basic view—especially its ability to create high returns on capital—hints the stock is not just a "value trap" but a possibly undervalued company in the travel industry.

This review of Expedia came from a structured hunt for acceptable value stocks. Investors curious about finding other firms that meet similar rules of fair valuation, earnings, strength, and growth can use this "Acceptable Value" filter themselves for more findings.

Disclaimer: This article is for information only and does not make financial guidance, a suggestion, or an offer or request to buy or sell any securities. The review uses data and ratings from ChartMill, and investors should do their own study and talk with a qualified financial advisor before making any investment choices. Past results are not a guide for future results.