A cooler inflation print gave Wall Street a reason to breathe on Friday, but not enough to fully relax.

By the final hour, sellers leaned back on the “sell tech into strength” button, and we limped into the long Presidents’ Day weekend with markets basically unchanged, but with plenty of single-stock drama under the surface.

The Inflation "Gift" and the Fed’s Next Move

If you were looking for a silver lining to take into the holiday, the January inflation data was it. [https://tradingeconomics.com/united-states/consumer-price-index-cpi), which was a pleasant surprise compared to the 2.5% analysts expected and a sharp drop from December's 2.7%.

Even better, core prices - the ones the Fed watches like a hawk - dipped to 2.5%.

From where I sit, this significantly shifts the conversation back toward rate cuts later this year. Earlier in the week, strong labor market data had some of us worried that the Fed would stay "higher for longer," but this cooling CPI print suggests the central bank’s mission is back on track.

The 10-year Treasury yield responded accordingly, slipping to 4.06%.

The AI Great Divide: Winners vs. Laggards

The real drama, however, continues to be the AI-driven divergence.

Applied Materials (AMAT | +8.08%) is the absolute star of the moment. CEO Gary Dickerson made it clear that the "accelerated investments" in AI computing are creating a massive tailwind for their semiconductor equipment.

When JPMorgan-analyst Harlan Sur hikes a price target from $260 to $400 in one go, you know the institutional appetite is ravenous.

On the flip side, we are seeing real signs of "AI displacement" fears. Expedia (EXPE | -6.41%) took a hit despite decent results because investors are terrified that consumers are ditching traditional travel agents for AI chatbots like ChatGPT or Google’s Gemini 3.

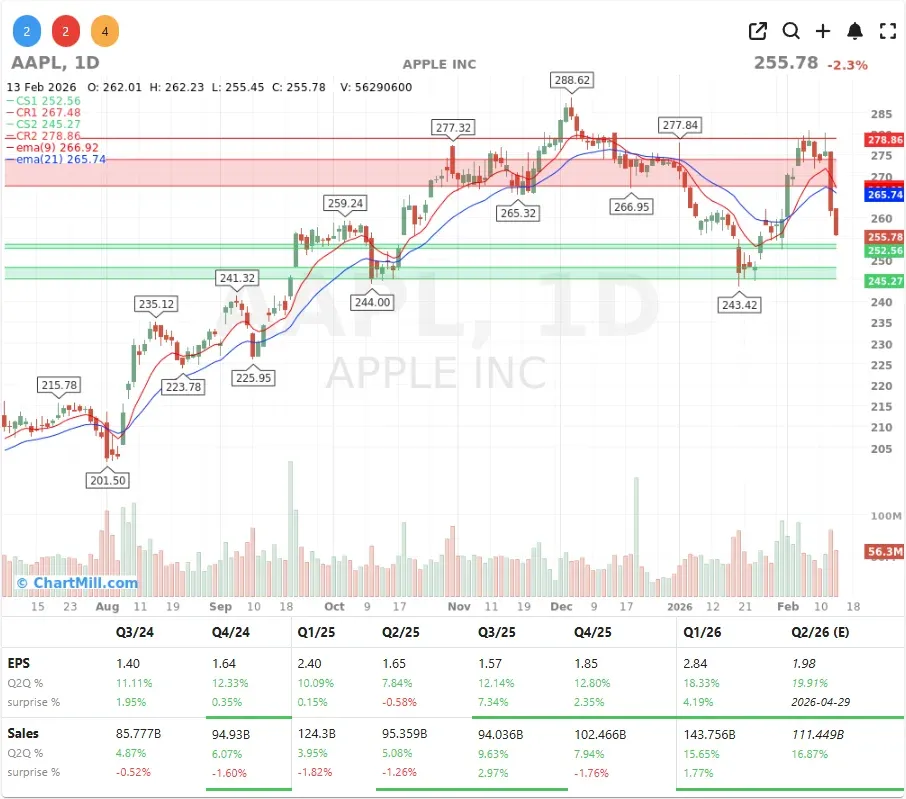

Even Apple (AAPL | -2.27%) is feeling the heat; a 8% weekly drop on news that the Siri AI upgrade might be delayed is a clear signal that being "late to the party" is a cardinal sin in this market.

Earnings Highs, Lows, and Geopolitical Shifting Sands

The earnings parade brought some staggering volatility.

Rivian Automotive (RIVN | +26.64%) rocketed higher after a revenue beat, proving there is still life in the EV sector if you can demonstrate growth.

Coinbase (COIN | +16.46%) also enjoyed a massive rally as it crushed adjusted profit estimates, likely aided by Bitcoin’s recovery back to $69,000.

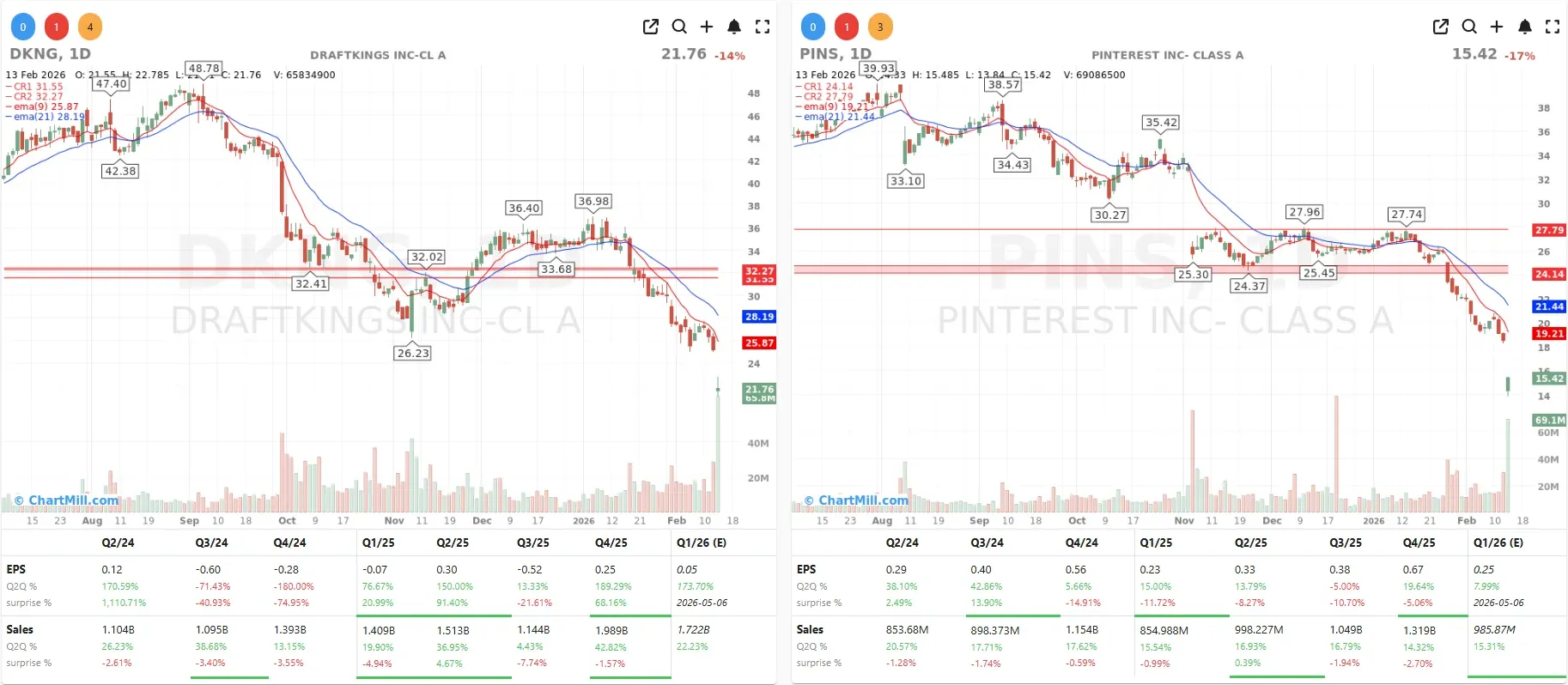

Conversely, Pinterest (PINS | -16.83%) and DraftKings (DKNG | -13.51%) served as a stark reminder that a "decent" quarter isn't enough if your future outlook is shaky.

Policy headlines hit steel

Steel stocks like Cleveland-Cliffs (CLF | -3.53%), Steel Dynamics (STLD | -3.92%), and Nucor (NUE | -2.96%) sold off on reports that President Trump might be considering a reversal of steel and aluminum tariffs.

This is a massive geopolitical pivot that could reshape the domestic manufacturing landscape overnight if it gains traction.

Conclusion

As we head into this shortened trading week, my advice is to look past the "flat" index numbers. The real story is the internal rotation.

We are seeing a market that is increasingly disciplined: rewarding tangible AI infrastructure growth while ruthlessly selling off sectors vulnerable to AI disruption or geopolitical policy shifts.

The cooling inflation gives us some breathing room, but the "AI anxiety" that has spread from tech to logistics and banking suggests that the volatility is far from over.

Keep your eyes on the yields, but watch the AI adoption rates even closer.

Kristoff - ChartMill

Next to read: Breadth Stabilizes After Violent Reversal