Market Monitor News July 01 BMO (Hewlett Packard Enterprise, SunRun UP - Enphase Energy DOWN)

By Kristoff De Turck - reviewed by Aldwin Keppens

Last update: Jul 1, 2025

After a quarter that felt like a stock market highlight reel, Monday's session didn’t disappoint. Records were broken, megadeals were sealed, and just enough geopolitical intrigue was sprinkled in to keep everyone on edge.

If you’re looking to read the pulse of the market, this is it; alive, kicking, and for now, tilted upward.

Record-Breaking Quarter Ends with a Bang

The second quarter wrapped up with fireworks (and no, I’m not talking about July 4th yet). The S&P 500 closed at a new all-time high of 6,204.95 (+0.5%), the Nasdaq rose 0.5% to 20,369.73, and the Dow Jones wasn’t to be left out, climbing 0.6% to 44,094.77.

The S&P ended the quarter with a nearly 12% gain, and the Nasdaq went even harder with an 18% jump, its best stretch since early 2023. The Dow, trailing slightly behind, added 6.5% but remains about 3% from its record high.

Driving the optimism is a potent cocktail of resilient tech earnings, easing trade tensions, and renewed expectations of a Fed rate cut in the not-so-distant future.

The icing on the cake? Canada backtracked on its planned digital services tax, just in time to prevent a potential trade war escalation with the US.

Trade Winds Shift, Investors Sniff Opportunity

President Trump’s “big, beautiful” trade deal continues to take shape, and markets are watching closely. Reports from Bloomberg suggest the EU may be warming up to a US trade agreement, centered around a universal 10% tariff on most European goods, with carve-outs for sectors like pharmaceuticals, semiconductors, alcohol, and aircraft.

It’s all still in legislative limbo, but signs of thawing tensions are pushing risk appetite higher.

Meanwhile, Trump's threat to fire Fed Chair Jerome Powell and replace him with someone “more dovish” rattled the currency markets. The dollar weakened, pushing the EUR/USD to 1.1763, and increasing speculation of looser monetary policy ahead.

Cloudy With a Strong Chance of Revenue: Oracle’s Mega Deal

One of Monday’s loudest headlines came from Oracle (ORCL | +3.99%), which secured what might become a $30 billion annual cloud contract starting FY2028.

The client remains unnamed, but CEO Safra Catz assured investors it’s not a one-off; Oracle reportedly signed multiple significant cloud deals.

Tip: Read our latest 'Stocks to Watch Report' on Oracle

To put this in perspective, Oracle posted $57.4 billion in revenue in FY2025, so the new deal alone could eventually account for more than half its current total sales!

Apple Eyes Outside AI Help, Investors Nod in Agreement

Apple (AAPL | +2.03%) quietly rallied late Monday after Bloomberg reported the tech titan may shelve its internal AI ambitions in favor of licensing third-party models from the likes of Anthropic (Claude) and OpenAI (ChatGPT).

This strategic pivot signals Apple’s growing urgency to catch up in the AI arms race, especially after rumors about a potential acquisition of Perplexity AI earlier this month.

It’s a rare moment of humility for Cupertino, but investors liked what they heard. And in this market, acknowledging you’re behind might be the smartest thing you can do.

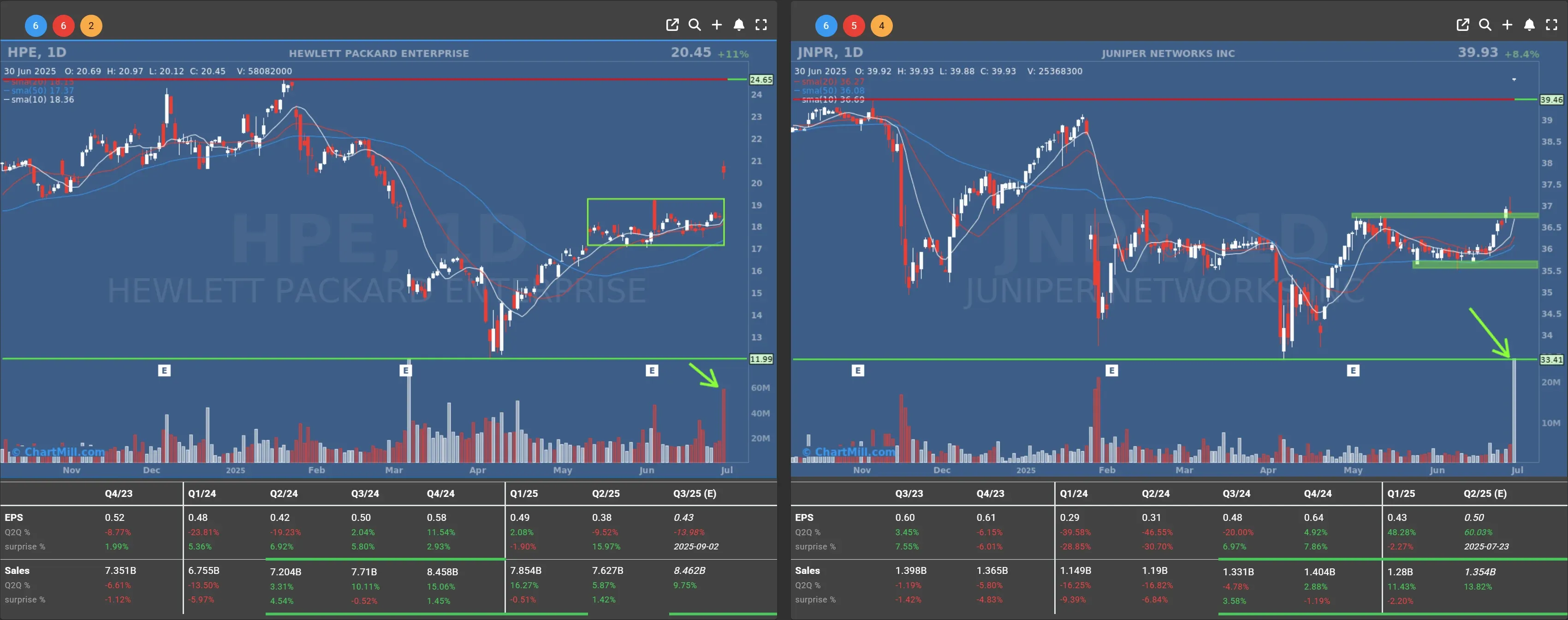

HPE Surges on Juniper Green Light and Analyst Cheers

Shares of Hewlett Packard Enterprise (HPE | +11.08%) rocketed higher following DOJ approval for its $14 billion acquisition of Juniper Networks (JNPR | +8.45%). The deal aims to shift HPE’s revenue mix away from hardware and more toward network infrastructure... hello, higher margins.

Bank of America sweetened the story, bumping its price target on HPE from $20 to $23 and reiterating a Buy rating. That’s another 11% upside from here, if you're counting.

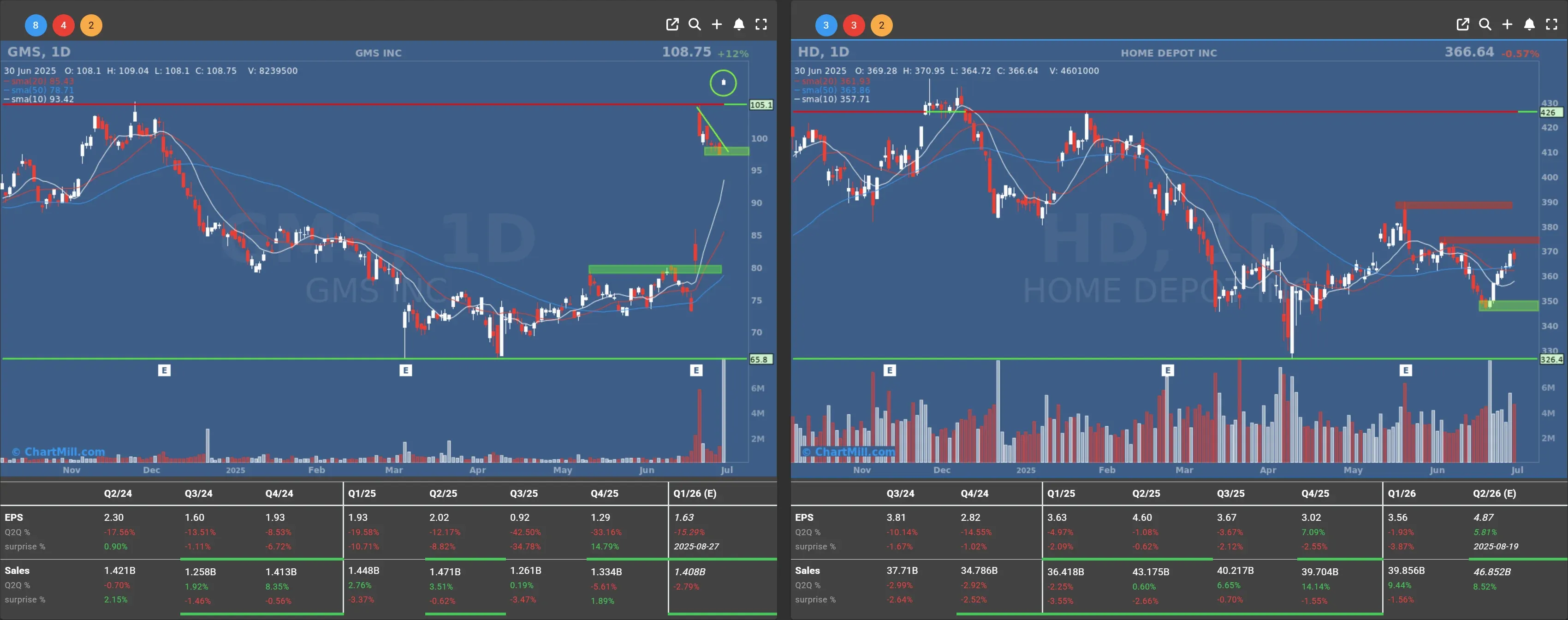

Home Depot Goes Pro with Bold GMS Acquisition

Home Depot (HD | –0.57%) is doubling down on the pro market, announcing that its SRS Distribution unit will acquire GMS (GMS | +11.73%), a specialty building materials supplier, for $4.3 billion. That price tag includes a hefty 39% premium over GMS’s pre-rumor price.

This move puts an end to a potential hostile bid from QXO, backed by billionaire Brad Jacobs. It’s a savvy strategic grab as HD tries to hedge against the slowdown in consumer renovation spending.

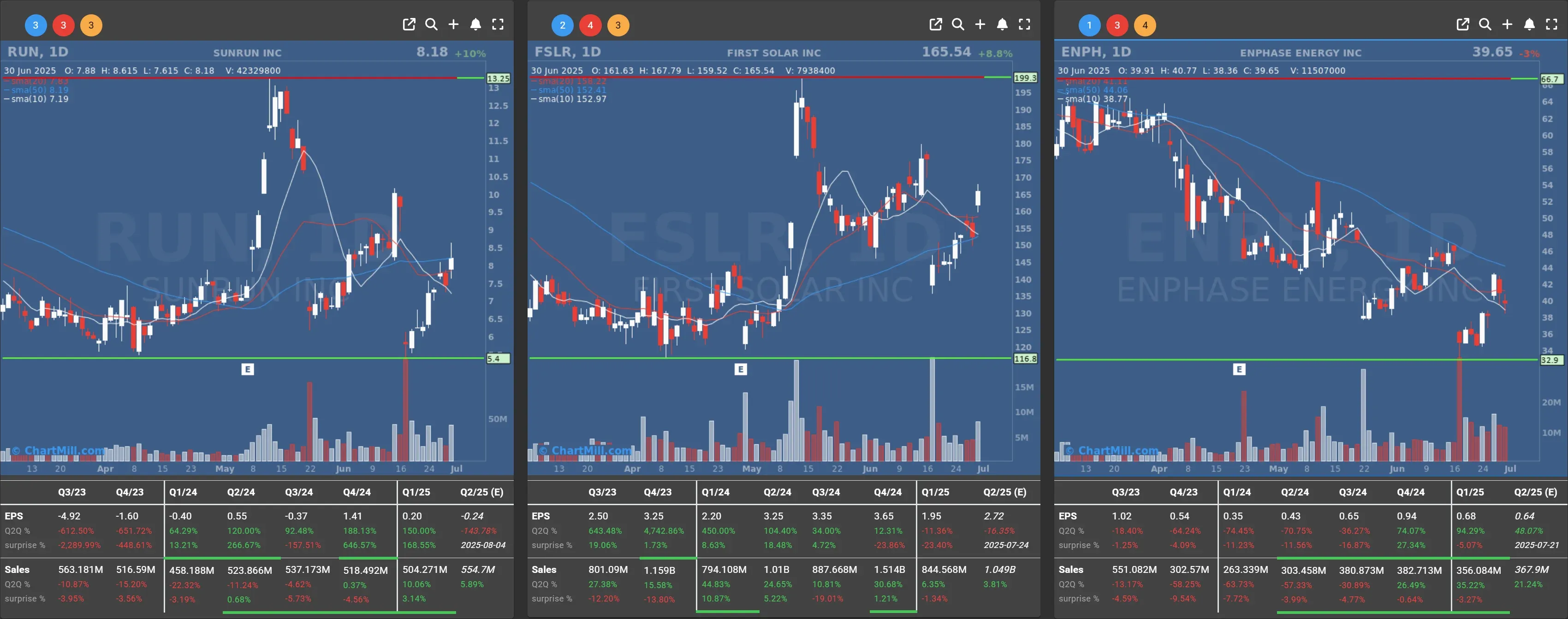

Solar Stocks Shine, EVs Dim in Wake of Trump's Budget Law

Green energy names saw mixed fortunes after the latest draft of Trump’s budget law. First Solar (FSLR | +8.81%) and Sunrun (RUN | +10,09%) surged, while Enphase Energy (ENPH | –3,01%) dipped.

The bill phases out tax breaks for residential solar leasing but preserves incentives for power purchase agreements, good news for industrial players like First Solar.

Meanwhile, Tesla (TSLA | –1.84%) took a hit as EV tax credits are set to expire come September. Unsurprisingly, Elon Musk had a few things to say about that over the weekend (you can probably guess the tone).

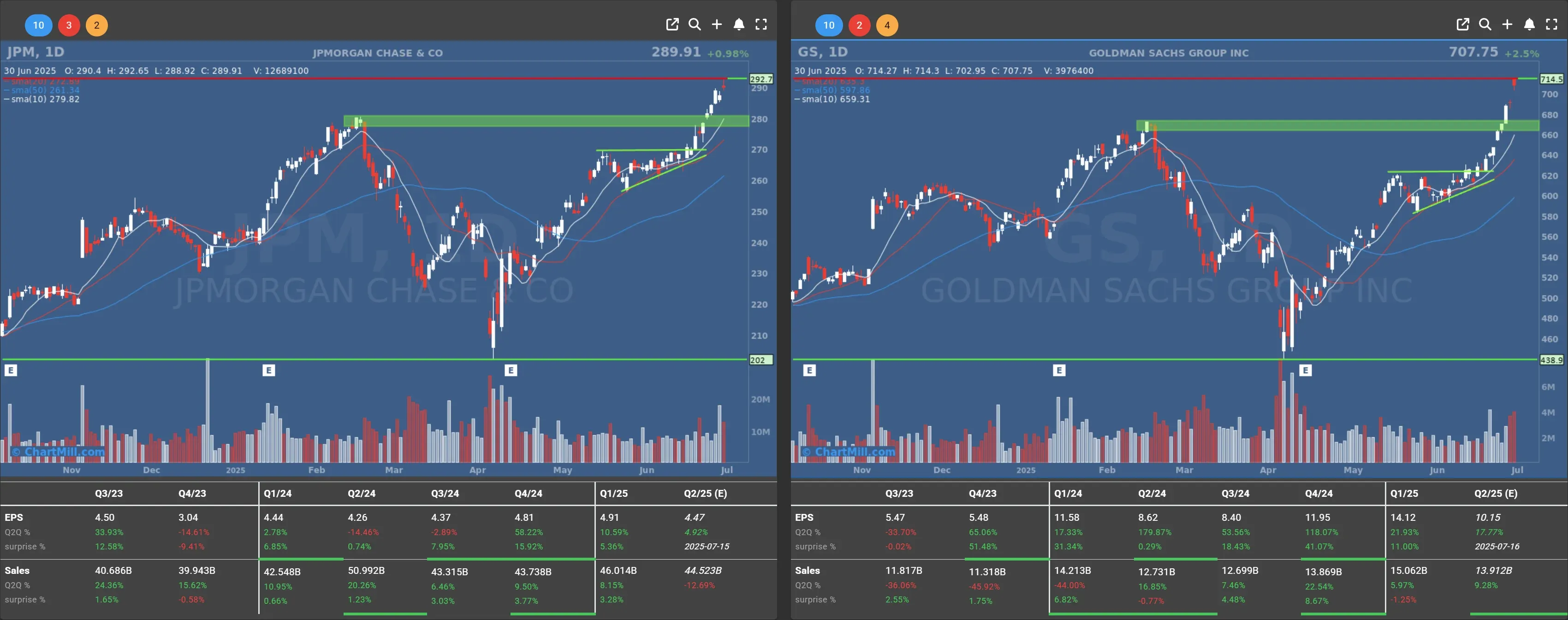

Banks Pass Stress Test With Flying Colors

In another confidence booster, major US banks including JPMorgan (JPM | +0.98%), Goldman Sachs (GS | +2.45%), Wells Fargo (WFC | +0.78%), and Bank of America (BAC | +0.42%) all passed the Fed’s annual stress test.

The verdict? These institutions are more than capitalized enough to weather even a severe recession.

It’s not often you hear “Wall Street” and “safe and sound” in the same sentence, but for now, the balance sheets are doing the talking.

Wrapping Up: Eyes on Jobs and Fireworks

Markets will be closed this Friday for Independence Day, but the official jobs report drops Thursday, a day earlier than usual. Expect volatility to pick up mid-week as traders position themselves ahead of the data and take profits from what’s been an exceptional quarter.

Until then, the bulls have the upper hand and they’re not shy about it.

Kristoff - Co-Founder ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, July 01

706.46

-1.29 (-0.18%)

48.15

+0.83 (+1.75%)

290.41

+0.5 (+0.17%)

81.49

+1.37 (+1.71%)

373.16

+6.52 (+1.78%)

218.96

+0.33 (+0.15%)

39.95

+0.02 (+0.05%)

207.82

+2.65 (+1.29%)

162.96

-2.58 (-1.56%)

300.71

-16.95 (-5.34%)

40.91

+1.26 (+3.18%)

9.04

+0.86 (+10.51%)

20.48

+0.03 (+0.15%)

108.76

+0.01 (+0.01%)

Find more stocks in the Stock Screener

GS Latest News and Analysis

a day ago - ChartmillMarket Monitor News July 01 BMO (Hewlett Packard Enterprise, SunRun UP - Enphase Energy DOWN)

a day ago - ChartmillMarket Monitor News July 01 BMO (Hewlett Packard Enterprise, SunRun UP - Enphase Energy DOWN)Wall Street Keeps Climbing as Deals, AI Drama, and Trade Winds Stir Up the Market

2 days ago - ChartmillThese S&P500 stocks are moving in today's session

2 days ago - ChartmillThese S&P500 stocks are moving in today's sessionLet's delve into the developments on the US markets in the middle of the day on Monday. Below, you'll find the top gainers and losers within the S&P500 index during today's session.

2 days ago - ChartmillWhat's going on in today's pre-market session: S&P500 movers

2 days ago - ChartmillWhat's going on in today's pre-market session: S&P500 moversThe US market is yet to commence its session on Monday, but let's get a preview of the pre-market session and explore the top S&P500 gainers and losers driving the early market movements.