What a difference a day makes.

On Thursday, Meta Platforms spooked tech investors with sky-high AI spending and shrinking free cash flow. But by Friday, the mood had flipped.

Amazon stormed to a new record after reporting a blowout quarter for its cloud division AWS and in doing so, gave the entire Nasdaq a lift heading into the weekend.

Amazon Takes the AI Crown

While Meta keeps pouring billions into AI projects that may or may not pay off, Amazon (AMZN | +9.58%) is already cashing in. AWS revenue jumped 20% to $33 billion, contributing $11.4 billion in operating profit. CEO Andy Jassy even hinted that the company’s cloud backlog has swelled to $200 billion and that’s before the new October deals are counted.

Morgan Stanley promptly raised its price target from $300 to $315, maintaining its “buy” rating. Investors clearly agreed, pushing AMZN to $244.20, a market cap of $2.63 trillion and a jaw-dropping $240 billion in added value overnight. The Nasdaq closed up 0.6%, wiping away the Meta hangover in one clean move.

Tech Titans Close Out a Wild Earnings Week

It’s been a mixed bag for the so-called “Mag7.”

Alongside Amazon, Apple (AAPL | -0.38%) reported strong results and struck an upbeat tone heading into the holiday season.

Alphabet (GOOG | -0.03%) and Microsoft (MSFT | -1.51%) also impressed investors with healthy AI-related cloud demand.

Then there was Meta (META | -2.72%) - the odd one out - punished for announcing $30 billion in new bond financing to fund its AI push. Free cash flow is expected to drop from $43 billion this year to $31 billion next year. Investors clearly weren’t thrilled: META fell another 3% Friday, on top of Thursday’s 11% plunge.

October Ends on a High Note

Despite the turbulence, October delivered solid gains: the Dow Jones and S&P 500 each rose around 2%, while the Nasdaq gained over 4%.

Strong tech earnings helped offset political uncertainty and the ongoing U.S. government shutdown, which entered its fifth week.

The lack of key macroeconomic data - including the Fed’s preferred PCE inflation gauge and the monthly jobs report - is complicating things for policymakers. Without fresh data, the Federal Reserve is effectively flying blind on inflation and employment trends. Not ideal, to put it mildly.

A Quiet Macro Scene with a Geopolitical Edge

On the economic front, Chicago’s PMI contracted less than expected, hinting at resilient productivity and new orders. Meanwhile, the meeting between President Trump and Chinese leader Xi Jinping provided a rare dose of optimism — the two agreed to a one-year trade truce, easing global tensions.

Oil prices ticked higher toward the weekend as reports surfaced that Washington is weighing strikes on Venezuelan targets linked to drug trafficking. “Even a small loss of heavy crude could have a noticeable impact,” warned Phil Flynn of Price Futures Group. WTI crude still ended the month 2% lower, while gold and silver gained nearly 4% in October.

Company Highlights

-

Chevron (CVX | +2.74%) reported record production of 4.1 million barrels per day and returned $6 billion to shareholders.

-

Netflix (NFLX | +2.74%) announced a 10-for-1 stock split and is reportedly exploring a bid for Warner Bros. Discovery’s streaming assets.

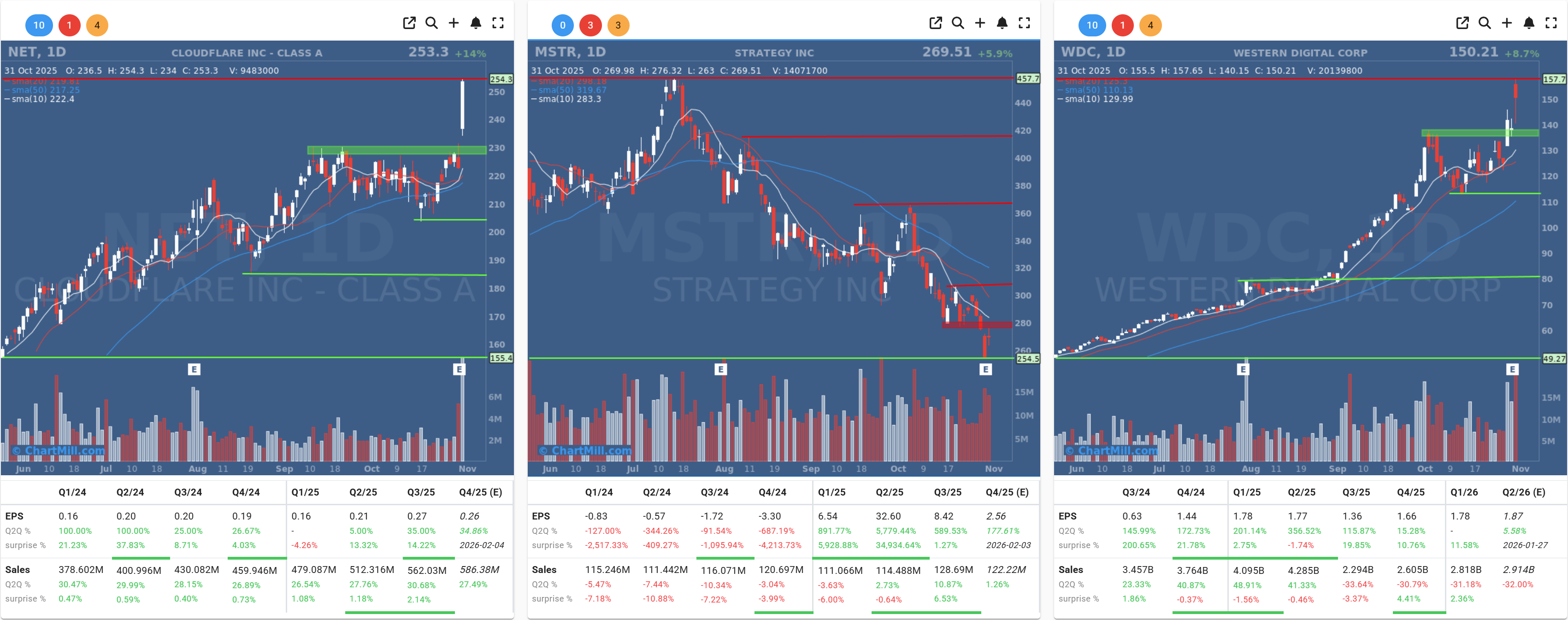

- Western Digital (WDC | +8.75%) and Cloudflare (NET | +13.84%) both crushed expectations with strong earnings, while bitcoin-focused MicroStrategy (MSTR | +5.87%) returned to profit as it expanded its holdings to 640,808 BTC.

Looking Ahead

As we head into November, investors face a tricky mix: strong corporate earnings versus political dysfunction in Washington. With the shutdown dragging on and inflation data delayed, markets may remain headline-driven for now.

But one thing is clear, as long as Big Tech keeps monetizing AI at this pace, Wall Street’s love affair with the sector isn’t cooling anytime soon. Just ask Amazon.

Kristoff - ChartMill

Next to read: Market Breadth Stabilizes After Sharp Dip, but Overall Trend Remains Weak