SALESFORCE INC (NYSE:CRM) was identified as an affordable growth stock by our stock screener. The company demonstrates solid growth potential while maintaining strong profitability and financial health, all at a valuation that doesn’t appear stretched. Below, we break down why CRM fits the criteria for investors seeking growth at a reasonable price.

Growth Prospects

- CRM has delivered strong revenue growth, with an 8.72% increase over the past year and a 17.25% average annual growth rate over recent years.

- Earnings per share (EPS) have grown by 15.29% in the last year, with a three-year average growth rate of 27.71%.

- Future growth remains promising, with expected annual EPS growth of 11.03% and revenue growth of 8.94%.

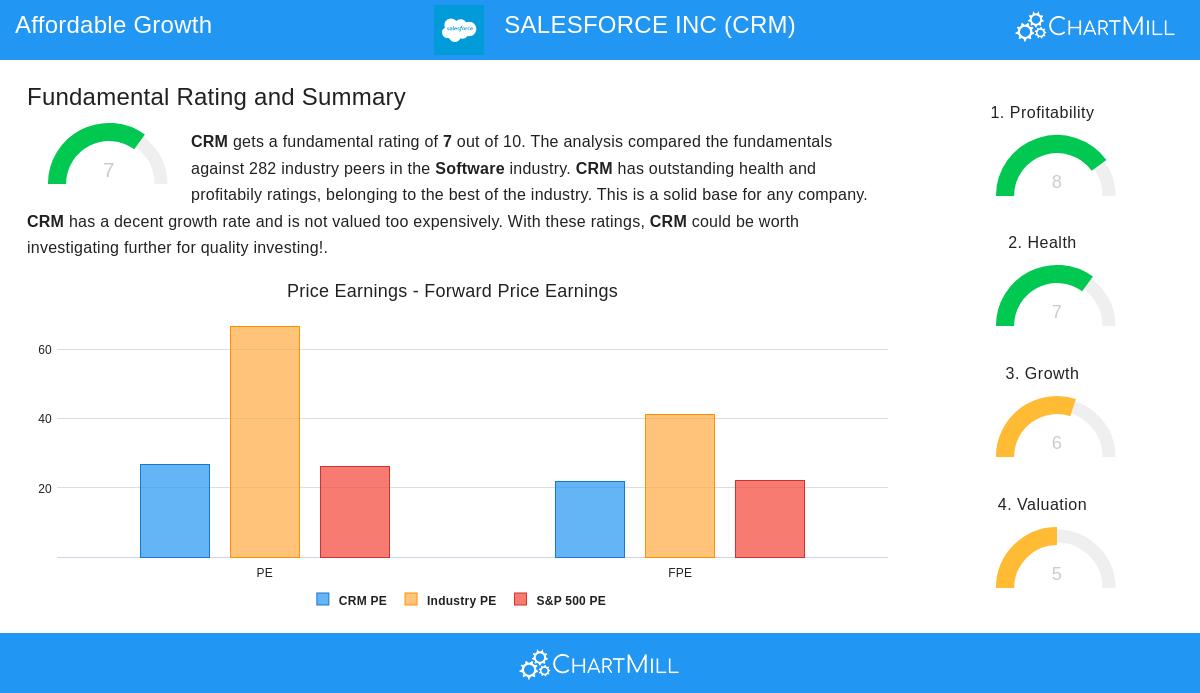

Valuation Assessment

- The stock trades at a P/E ratio of 26.72, slightly above the S&P 500 average (26.17) but below many industry peers—71% of software companies are more expensive.

- Its forward P/E of 21.81 is in line with the broader market and suggests a more reasonable earnings outlook.

- The Enterprise Value/EBITDA ratio indicates CRM is cheaper than 79% of its industry competitors.

Profitability & Financial Health

- CRM earns a high profitability rating (8/10), with strong margins: a 16.35% net profit margin (outperforming 83% of peers) and a 20.23% operating margin.

- Financial health is solid (7/10), with a low debt-to-equity ratio (0.14) and a strong Altman-Z score (4.66), indicating low bankruptcy risk.

- Free cash flow generation supports its ability to manage debt, with a favorable debt-to-FCF ratio of 0.68.

While CRM’s dividend yield is minimal (0.60%), its focus on reinvesting earnings aligns with its growth strategy.

For a deeper look, review the full fundamental analysis of CRM.

Our Affordable Growth screener lists more stocks with similar characteristics and is updated daily.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should conduct your own analysis before making investment decisions.