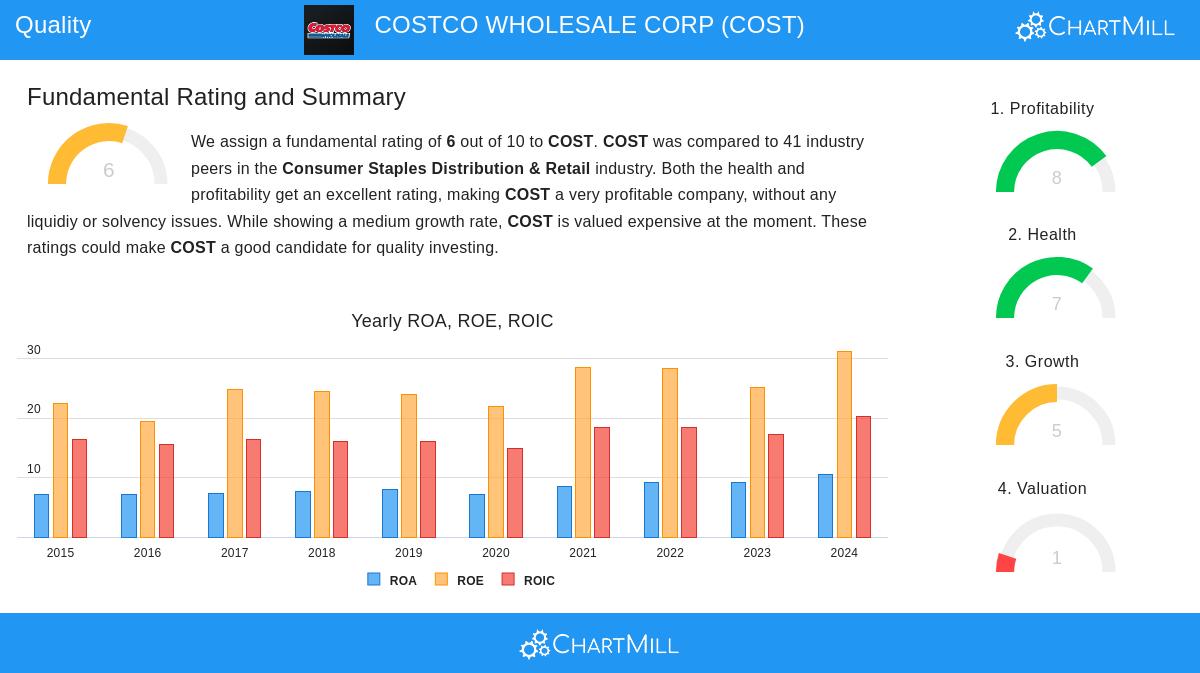

COSTCO WHOLESALE CORP (NASDAQ:COST) stands out as a strong candidate for quality investors, meeting key criteria for profitability, financial health, and sustainable growth. The company’s fundamentals reflect a well-managed business with competitive advantages, making it a compelling option for long-term investors.

Why COSTCO Fits the Quality Investing Criteria

- High Return on Invested Capital (ROIC): COSTCO’s ROIC of 31.66% (excluding cash and goodwill) is well above the 15% threshold for quality stocks, indicating efficient use of capital.

- Strong EBIT Growth: The company’s EBIT has grown at a 14.4% annual rate over the past five years, outpacing its revenue growth of 6.7%, a sign of improving profitability.

- Low Debt Relative to Cash Flow: With a debt-to-free-cash-flow ratio of 0.83, COSTCO could pay off its debt in less than a year using current cash flow, reflecting financial strength.

- High Profit Quality: Over the past five years, COSTCO has converted 103% of net income into free cash flow, demonstrating reliable earnings.

- Consistent Revenue Growth: Analysts expect future revenue growth of 6.7%, reinforcing the company’s ability to expand steadily.

Key Takeaways from the Fundamental Report

- Profitability: COSTCO scores well on profitability metrics, with strong returns on equity (29.8%) and assets (10.4%). Operating and profit margins have also improved over time.

- Financial Health: The company maintains a solid balance sheet, with a low debt-to-equity ratio (0.23) and an Altman-Z score of 10.2, indicating minimal bankruptcy risk.

- Valuation: While COSTCO trades at a premium (P/E of 60.4), its high profitability and growth prospects may justify the valuation for quality-focused investors.

Our Caviar Cruise screener lists more quality stocks and is updated daily.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should conduct your own analysis before making investment decisions.