Wall Street continues its smooth glide into earnings season, with just enough turbulence brewing in the background to keep investors on their toes. While optimism about Big Tech’s upcoming numbers keeps sentiment aloft, trade war chatter and a cooling economic pulse may yet unsettle the flight path.

Indices at New Heights But the Clouds Are Gathering

Let’s start with what can only be described as a power move by the major U.S. indices. The S&P 500 closed above the 6,300 mark for the first time ever, while the Nasdaq climbed 0.4% to another record high. Only the Dow Jones took a minor detour, slipping 0.1%.

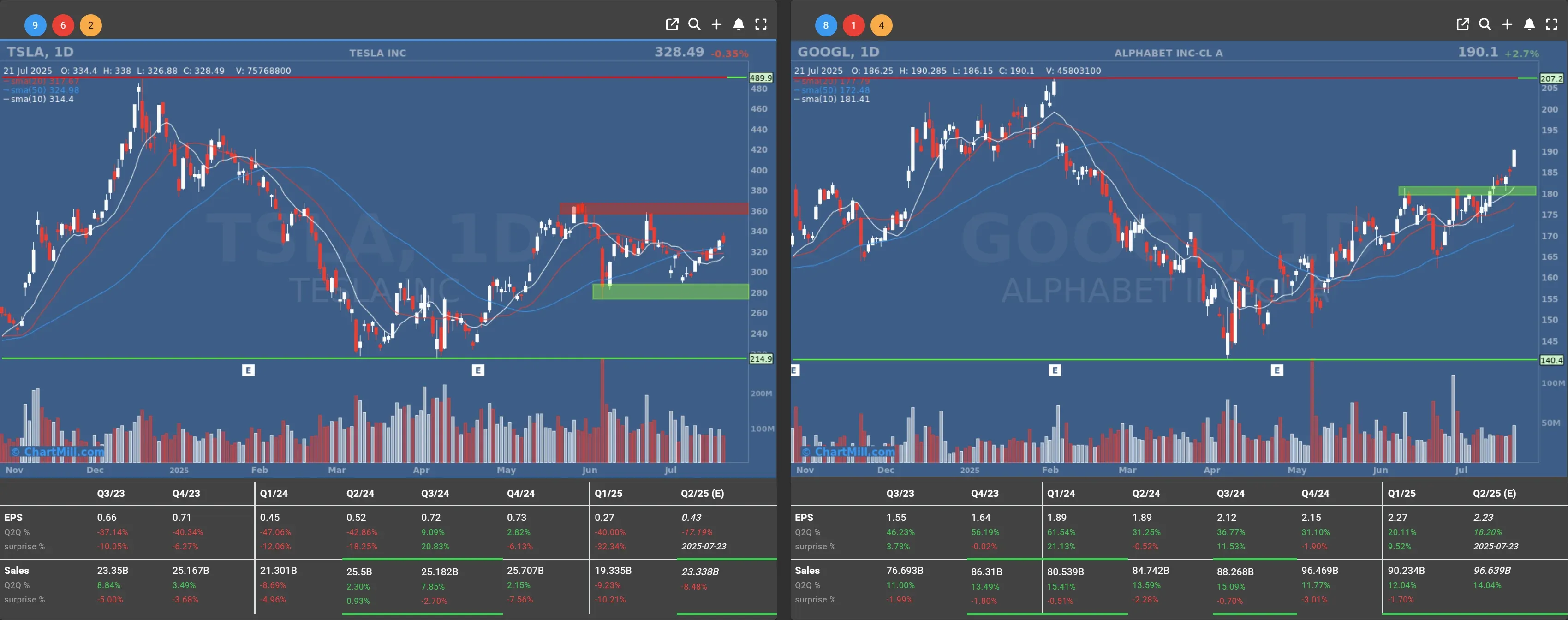

This bullish tone is largely driven by growing anticipation around this week’s earnings from Alphabet (GOOGL | +2.72%) and Tesla (TSLA | -0.35%), both reporting on Wednesday. The rest of the “Magnificent Seven” remain quiet for now but investor appetite is clearly alive and well.

Still, while traders sip on their half-year optimism, they’re keeping the other eye on Washington’s tariff saber-rattling.

U.S. Commerce Secretary Howard Lutnick has firmly reiterated that August 1 is a “hard deadline” for import tariffs. The European Union isn’t sitting idle, it’s already prepping countermeasures should negotiations stall.

Macroeconomic Indicators: Leading, But Lower

Not everything is up and to the right. Monday’s release of the U.S. leading indicators for June showed another decline.

After a minor upward revision for May, this renewed drop again signals weakness ahead in the economy. For context: leading indicators have been negative for months. The bond market seems to agree. The 10-year U.S. yield dropped 7 basis points to 4.36%, and Germany’s equivalent shed 8 points to land at 2.62%.

Oil softened slightly, with WTI crude down 0.2% to $67.20. Traders are pricing in weak demand caused by tariff threats and minimal expected disruption from new European sanctions on Russian oil.

Meanwhile, gold crept back above $3,400 per troy ounce and the euro rose to 1.1689 versus the dollar.

AI Still the Golden Child of Tech

Amid all this, tech bulls keep pointing to the AI boom as a tailwind that's just getting started.

According to Wedbush, we're staring at a potential $2 trillion in AI-related spending over the next three years. That’s not a typo, trillion with a ‘T’.

For every $1 spent at Nvidia, $8–$10 flows through the rest of the tech ecosystem, Wedbush calculates. That alone could justify the rich valuations tech currently enjoys.

Domino’s Tastes Bitter Despite Beating Expectations

Domino’s Pizza (DPZ | -0.8%) delivered a revenue beat with $1.15 billion in sales, just topping analyst forecasts.

But investors were quick to toss the slice aside. The stock dropped after weak margin performance and vague commentary on upcoming promotional spending. A $27.4 million write-down tied to its DPC Dash investment didn’t help the optics either.

Earnings: The Good, the Bad, and the Steel

We’re still early in the reporting season, but 85% of S&P 500 companies that have reported so far have beaten estimates. That’s encouraging, but remember, the bar may have been set intentionally low. Here's a taste of what moved markets Monday:

Block (XYZ | +7.22%) surged after the fintech firm was added to the S&P 500, replacing Hess, which Chevron is acquiring. With a $43 billion market cap, Block’s inclusion surprised some, especially since rivals Robinhood ($93B) and Applovin ($120B) are larger.

Verizon (VZ | +4.04%) impressed with a solid earnings beat and improved full-year guidance.

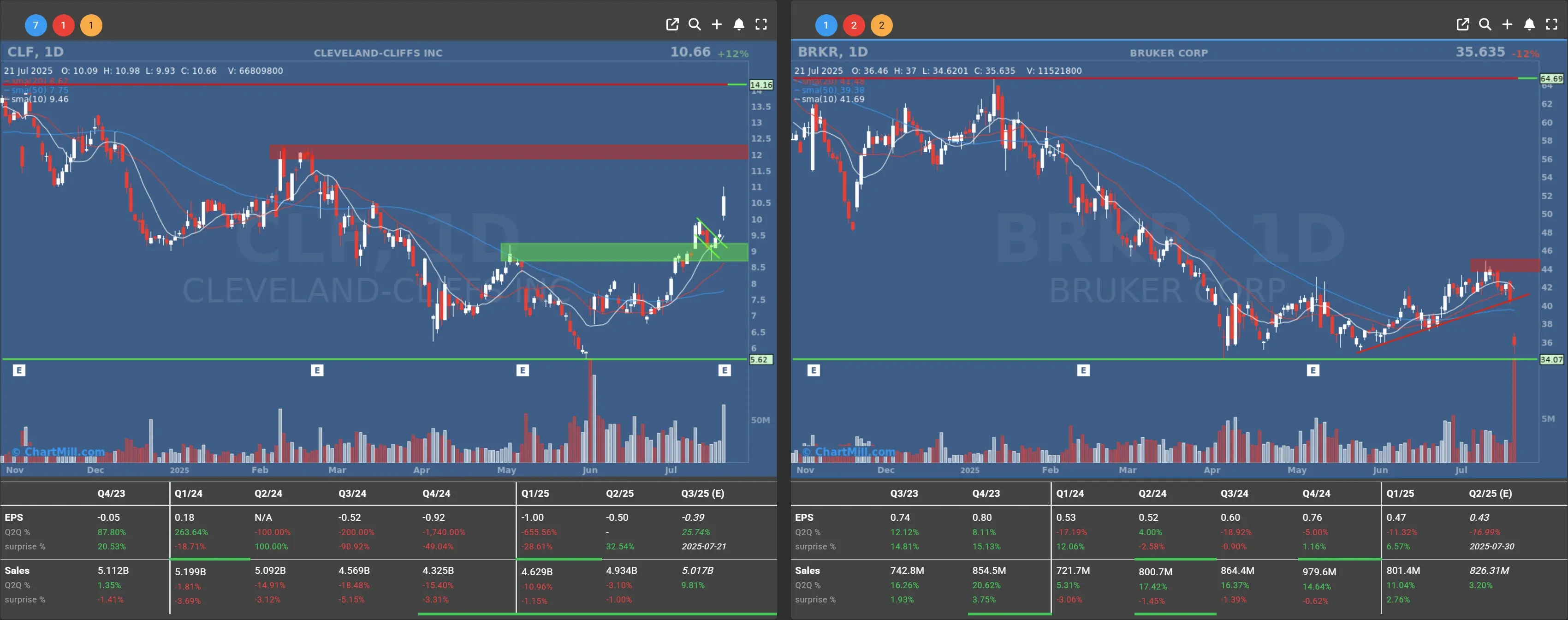

Cleveland-Cliffs (CLF | +12.45%) saw strength thanks to a narrower-than-expected loss. CEO Lourenco Goncalves attributed optimism to Trump’s pressure on the Fed and potential rate cuts to revive auto demand.

Bruker (BRKR | -12.12%) missed the mark on preliminary Q2 figures, prompting a sharp selloff.

Tesla’s Big Test Ahead

Tesla’s earnings Wednesday might be the week’s most volatile event. The company already revealed a 13.5% drop in Q2 deliveries, and analysts expect a ~10% revenue dip and up to 20% lower profit.

The real kicker? Elon’s much-hyped affordable model remains stuck in the pipeline, and Trump’s reversal of EV tax credits isn’t helping either.

SpaceX Ties the Government’s Hands

One last geopolitical nugget: Elon Musk’s other giant, SpaceX, might be “too important to fail.” The Wall Street Journal reported that federal agencies are stuck with existing SpaceX contracts due to their strategic importance, especially for defense and NASA.

With a $400 billion valuation, the company seems to be in orbit, both literally and politically.

Looking Ahead

We’re just getting warmed up. Earnings from Alphabet, Tesla, Intel, General Motors, Coca-Cola, Lockheed Martin, Texas Instruments, IBM, and American Airlines will flood the tape this week. Keep an eye not just on the bottom lines, but also the guidance, especially with tariffs looming and AI expectations peaking.

Final thought: With equity markets at all-time highs, and big tech about to show its cards, we’re either on the cusp of another leg higher, or setting up for a classic “buy the rumor, sell the news” moment.

I’ll be watching... with popcorn.

Kristoff - ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, July 22