Brent crude punched through $100 a barrel for the first time since 2022, Iran's new Supreme Leader vowed to keep the Strait of Hormuz closed and a simmering private credit crisis finally boiled over onto bank stock prices, all in a single Thursday session. Welcome to the new normal.

The day oil rewrote the script

If you thought markets were done reacting to the conflict in the Middle East, Thursday was a rude wake-up call. Brent crude futures settled above $100 per barrel for the first time since August 2022, rising over 9%, dragging equity indices firmly into the red.

The S&P 500 finished the day down 1.52% at 6,672.62, the Dow Jones Industrial Average shed 739 points (–1.56%) to close at 46,677.85, and the tech-heavy Nasdaq dropped 1.78% to end at 22,311.98.

The trigger? Iran's new Supreme Leader Mojtaba Khamenei said in his first address that the Strait of Hormuz should remain closed, TheStreet compounding fears that oil supply disruptions would persist far longer than originally hoped. The U.S. Navy's own energy secretary didn't help: energyminister Chris Wright told CNBC that American naval vessels are not yet able to escort ships through the strait and that it may not be possible until the end of the month.

The supply picture deteriorated further when the International Energy Agency revised its 2026 oil supply growth forecast sharply downward, to 1.1 million barrels per day from an earlier estimate of 2.4 million, warning in its monthly report that this conflict represents the largest supply disruption in the history of the global oil market.

What does this mean practically for your portfolio?

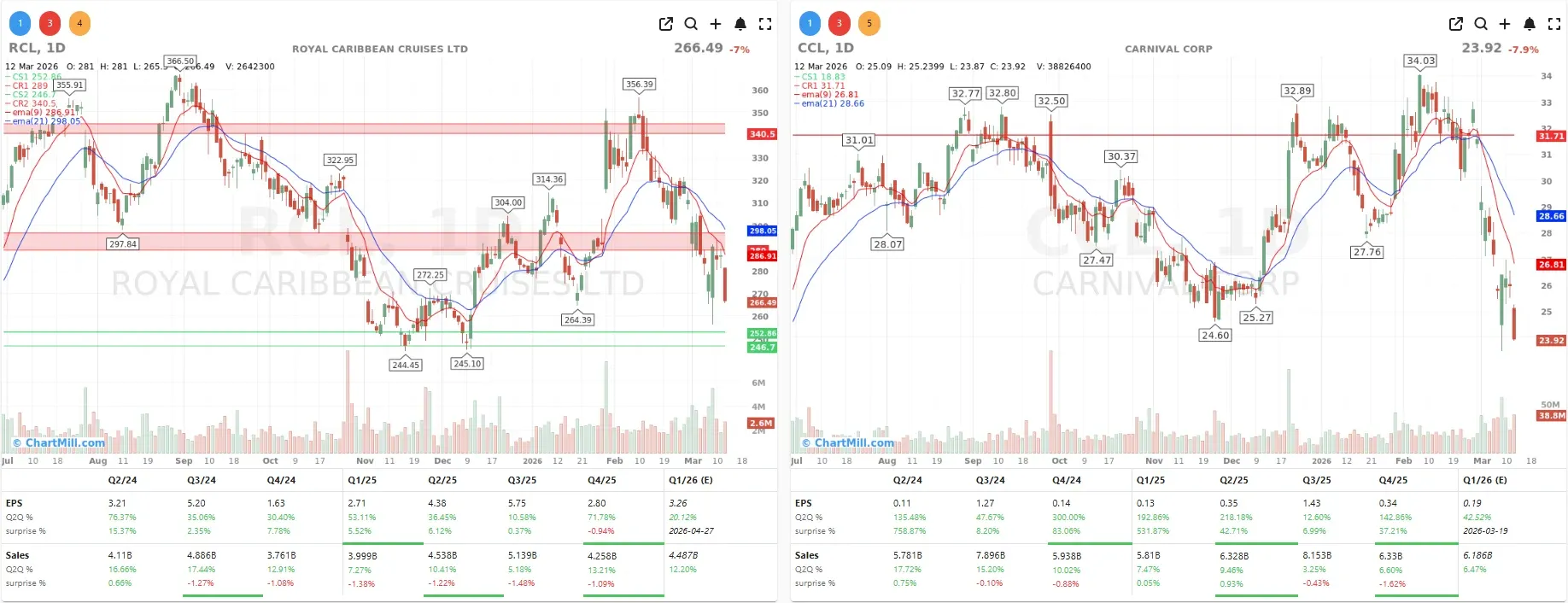

The oil shock is now a multi-week story, not a spike. Sectors with heavy fuel exposure - airlines, cruise lines, logistics - should be reviewed carefully. Royal Caribbean (RCL | –6.99%) and Carnival (CCL | –7.89%) are feeling it directly, as fuel is among their largest operating expenses.

Private credit: the crack nobody wants to talk about...

The second and arguably more structurally important storyline of the day was the increasingly visible stress in the private credit market. Private credit continued to grapple with fund redemptions, questions about underwriting standards, and concerns that advances in artificial intelligence could disrupt some borrowers, particularly software companies.

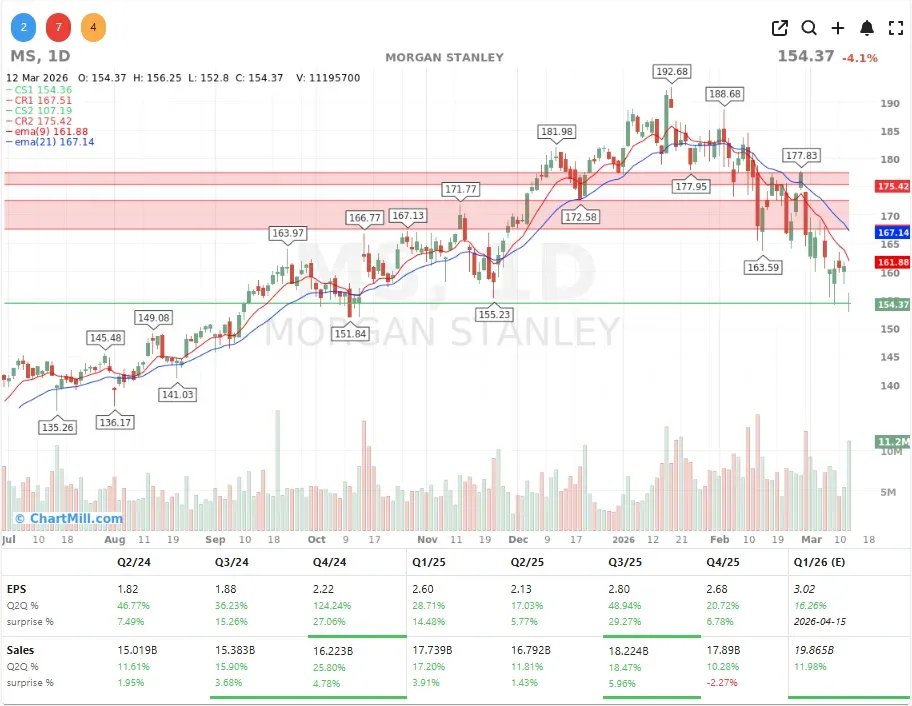

Morgan Stanley's (MS | –4.05%) North Haven Private Income Fund received redemption requests totaling 10.9% of shares outstanding.

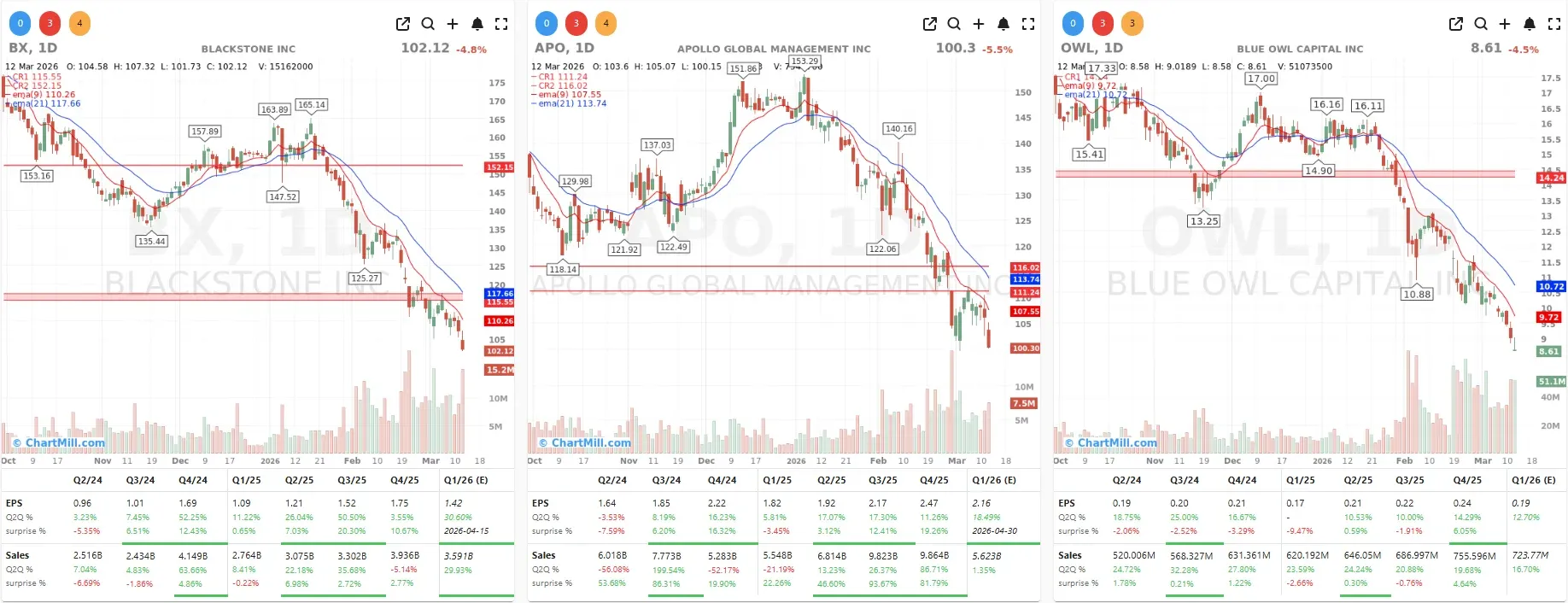

Blue Owl Capital (OWL | -4.55%) lost 4.55%, while Blackstone (BX | -4.78%) and Apollo Global (APO | -5.47%) shed around 5% each, after Morgan Stanley and Cliffwater imposed caps on withdrawals from their multi-billion-dollar private credit funds. Deutsche Bank's disclosure of a €26 billion private credit exposure didn't help sentiment either.

According to Bloomberg Intelligence analyst Herman Chan, the direct exposure of individual banks is relatively contained, but the market tends to shoot first and ask questions later. That dynamic was clearly on display Thursday.

What's interesting here, it turns out JPMorgan has a structural advantage in its private credit agreements: unlike most of its peers, it retains the right to revalue the collateral backing its back-leverage loans at any time based on its own assessment.

That gives the bank earlier and more decisive control over tightening conditions and more negotiating leverage to demand better terms or additional collateral before problems escalate. It's a subtle but meaningful contractual edge.

Goldman Sachs (GS | –4.4%) meanwhile became the first major brokerage to push its rate cut forecast to September from June, citing inflation concerns.

Adobe beats, but the real story is the CEO

After the close, Adobe (ADBE | –7,8% AH) reported what CEO Shantanu Narayen called a record first quarter. Adobe posted record Q1 FY2026 revenue of $6.40 billion, non-GAAP EPS of $6.06, and $2.96 billion in operating cash flow. The company beat consensus on both the top and bottom lines and its AI-related annual recurring revenue more than tripled year-over-year.

On paper, this is exactly what the market wanted. In practice, Adobe shares fell about 7% in extended trading and the culprit wasn't the numbers. Narayen announced he intends to hand over the CEO role after 18 years once a successor is identified, though he will remain as executive chairman.

Coming at a moment when the software sector faces existential questions about AI commoditization, losing the architect of Adobe's creative ecosystem introduces a layer of uncertainty the market is clearly not comfortable pricing in. I'd argue the sell-off is an overreaction to the headline, but the timing is undeniably awkward.

Lennar struggles as housing remains frozen

Homebuilder Lennar (LEN | –4.17%) delivered a Q1 that reminded everyone how difficult the housing market continues to be. The company's revenue dropped from $7.63 billion a year ago to $6.62 billion, missing the $6.84 billion consensus estimate.

Net income fell from $519 million to $229 million, a decline that reflects the brutal combination of elevated mortgage rates, constrained affordability, and - as CEO Stuart Miller noted - the additional overhang of the conflict in Iran.

The forward guidance was modest: 21,000 to 22,000 deliveries in Q2 at average sale prices of $370,000–$375,000. That's not the kind of visibility that gets institutional buyers excited. The housing sector remains one of the most rate-sensitive corners of the market, and until the Fed starts moving, it's hard to see a meaningful catalyst for re-rating.

Where the money actually went: fertilizers and forgotten names

With most sectors painting red, the real action Thursday was in a handful of contrarian plays.

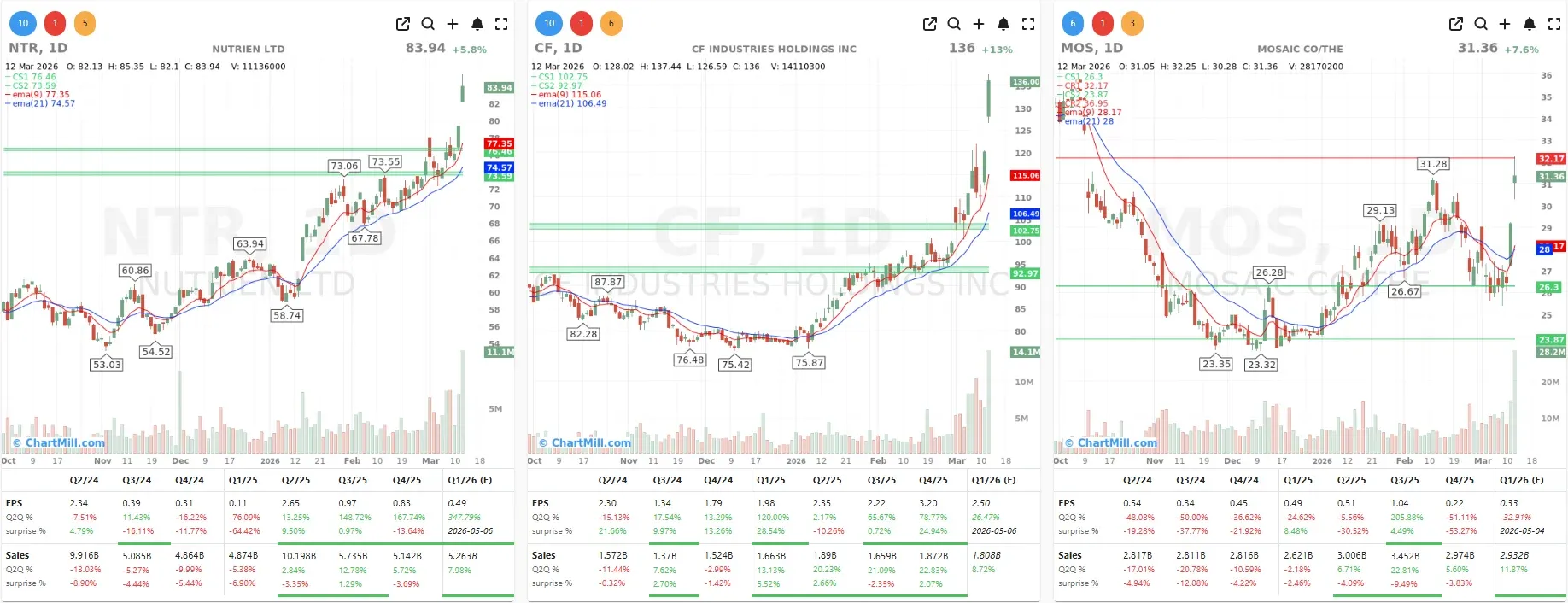

Fertilizer producers surged as traders connected the dots between a closed Strait of Hormuz and the global supply of inputs for agricultural chemicals. CF Industries (CF | +13.21%), Mosaic Company (MOS | +7.58%), and Nutrien (NTR | +5.84%) all gained sharply, with Jefferies analysts warning that fertilizer prices could stay elevated through the first half of 2027 due to the crisis.

Then there were the earnings surprises that cut through the macro noise:

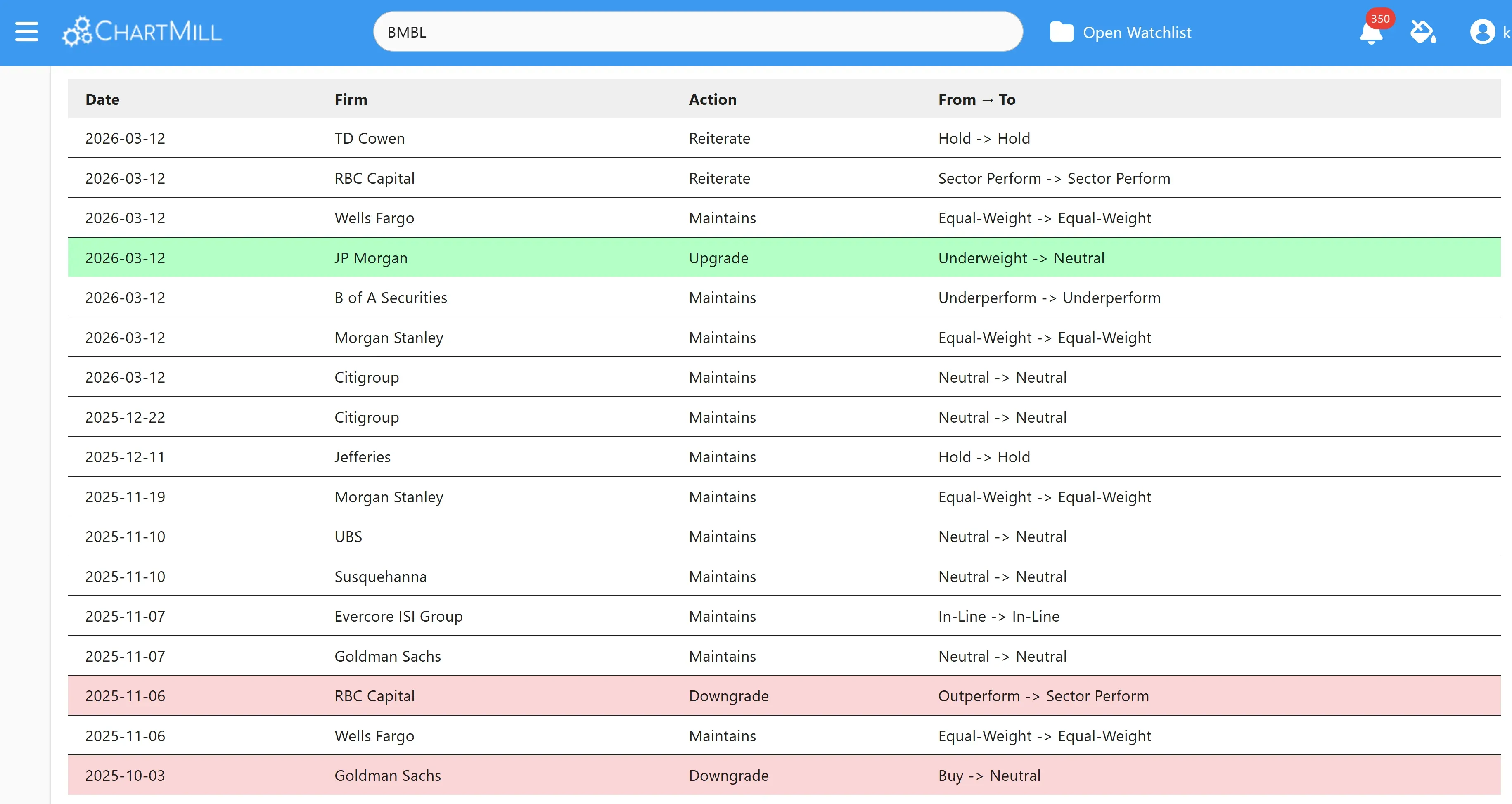

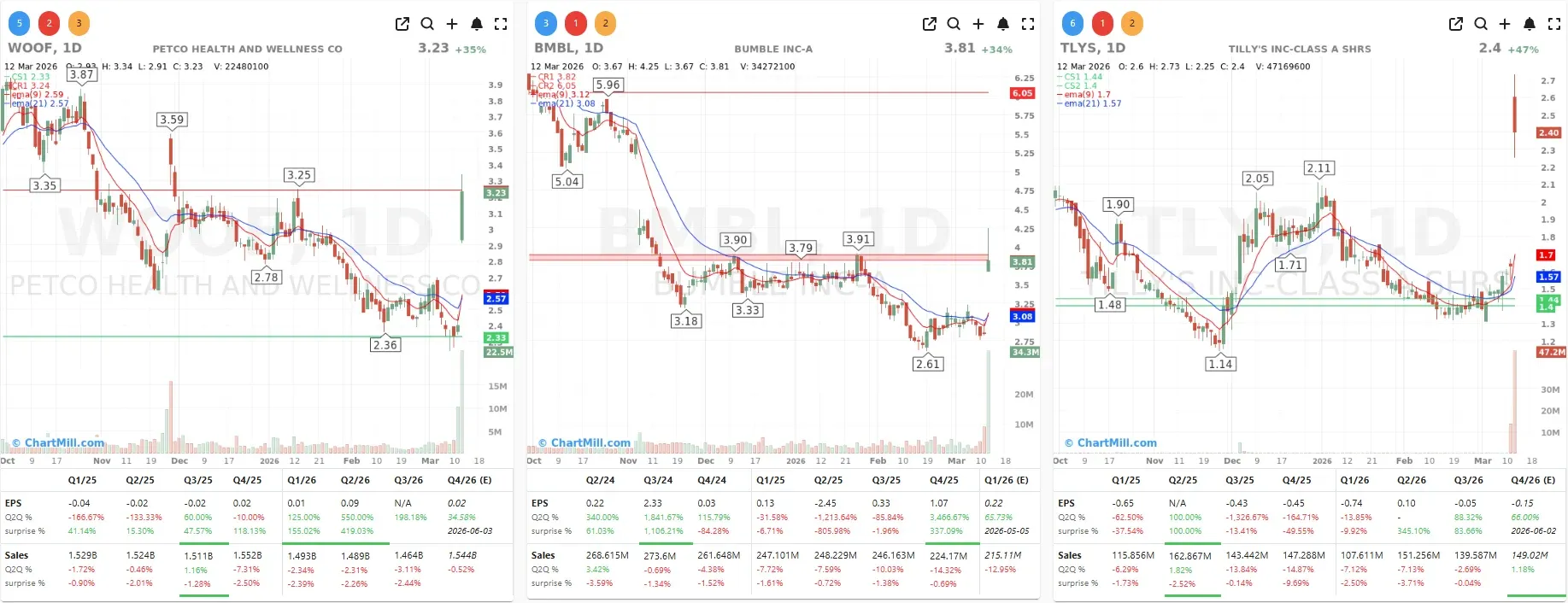

Bumble (BMBL | +34.15%) surged over 34% after beating revenue expectations and reporting a higher average revenue per paying user. JPMorgan upgraded the stock to neutral, with analysts broadly noting that focus now shifts to the company's upcoming product overhaul planned for later in the year.

Tilly's (TLYS | +47.24%) rocketed 47% after reporting double-digit comparable store sales growth in Q4 and returning to profitability.

Petco Health & Wellness (WOOF | +34.58%) jumped 35% on a restructuring-driven outlook for a return to revenue growth.

On the losing side beyond the banks: UiPath (PATH | –8.16%) offered below-consensus revenue growth guidance, and Lucid Group (LCID | –7.87%) failed to inspire with new targets at its investor day.

Dollar General disappoints the optimists

Dollar General (DG | -6.14%) was among the worst performers in the S&P 500, shedding around 4–5% after guiding for comparable sales growth of 2.2%–2.7% in its new fiscal year.

In isolation, that guidance isn't alarming. The problem is that DG has built a reputation for underpromising and overdelivering and the stock had already rerated sharply higher (+84% over the past twelve months). When expectations are that elevated, anything less than a clear beat becomes an excuse to take profits. That's exactly what happened.

Macro data: a rare bright spot

Amid the geopolitical and credit noise, the economic data was actually quite decent.

-

Jobless claims came in at 213,000, slightly below the 215,000 expected and the U.S. trade deficit for January contracted by 25%, as exports rose 5.5% and imports edged lower.

-

The deficit with the EU narrowed by $5 billion, while the shortfall with China stood at nearly $32 billion. Housing starts rose more than 7%, though building permits fell 5%, a mixed but not alarming picture for housing supply.

-

On the currency side, the euro-dollar rate was trading around 1.1518, while gold, silver, and bitcoin saw modest declines.

Bottom line

Thursday was a session where macro events completely overwhelmed company fundamentals. Adobe beat estimates and still sold off after-hours. Lennar missed and barely moved.

The market's attention is squarely on oil, the Strait of Hormuz, and the cascading implications for inflation and Federal Reserve policy. With rate cut bets now pushed firmly into late 2026 or beyond, the path of least resistance for equities remains uncertain in the near term.

The fertilizer trade is worth watching as a genuine geopolitical hedge. And the private credit story is far from over, I'd expect more headlines over the coming weeks as fund redemptions and collateral markdowns continue to surface.

Investors with exposure to alternative asset managers should be reassessing risk carefully.

Stay sharp heading into Friday's session.

ChartMill Market Desk

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Market Breadth Deteriorates Further as Participation Keeps Narrowing