Peter Lynch’s investment strategy, described in One Up on Wall Street, centers on finding companies with consistent growth at fair prices. His method combines growth and value investing, stressing strong fundamentals, earnings, and controlled debt. The approach steers clear of overly hyped or rapidly expanding businesses, preferring those with stable, clear operations that can deliver returns over time.

One stock that matches Lynch’s standards is CF INDUSTRIES HOLDINGS INC (NYSE:CF), a nitrogen fertilizer producer with a focus on decarbonization and low-carbon hydrogen solutions. The company’s financials show several metrics Lynch valued:

Why CF Industries Matches the Lynch Approach

-

Consistent Earnings Growth

- Lynch looked for firms with 5-year EPS growth between 15% and 30%, fast but not unstable. CF’s EPS has increased by 24.8% per year over the last five years, fitting this range.

- The company’s revenue growth, at 5.3% yearly, shows steadiness in its core markets, avoiding the unpredictability of high-growth industries.

-

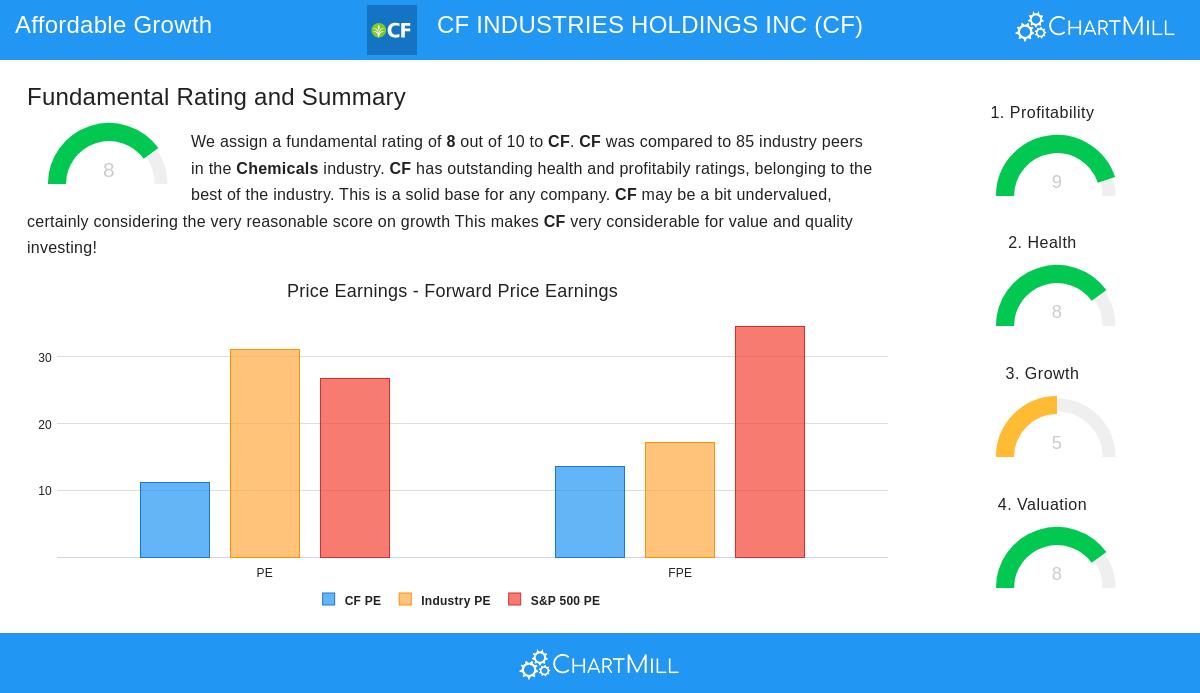

Reasonable Valuation (PEG Ratio ≤ 1)

- A key part of Lynch’s strategy is the PEG ratio, which accounts for growth. CF’s PEG of 0.45 (based on past 5-year growth) suggests it is undervalued compared to its earnings path.

- Its P/E of 11.1 is also below the industry average (31.2) and the S&P 500 (26.7), adding to its appeal.

-

Solid Balance Sheet

- Lynch preferred companies with limited debt. CF’s debt-to-equity ratio of 0.60 falls within his acceptable range (he favored <0.25 but allowed up to 0.6).

- Liquidity is strong, with a current ratio of 3.22, well above the minimum of 1, showing it can easily meet short-term needs.

-

High Profitability (ROE > 15%)

- CF’s return on equity (26.2%) places it in the top 4% of its industry, a sign of efficient capital use—something Lynch admired.

- Its operating margin (29.2%) and profit margin (20.2%) also beat most competitors, confirming its strong market position.

Financial Strength and Other Advantages

The fundamental analysis report gives CF an 8/10 score, noting:

- Profitability: High margins and ROE, with reliable earnings and cash flow.

- Dividend Stability: A 2.4% yield with a 10-year history of growth, though payouts remain low.

- Industry Standing: Beats 85–97% of chemical sector peers in metrics like ROIC and liquidity.

Potential Concerns

- Slower Growth: Analysts expect future EPS growth at 5.6% yearly, a slowdown from past rates. Lynch might see this as a warning, requiring closer study of market cycles or saturation.

- Moderate Debt: While within Lynch’s limits, the debt/equity ratio has edged up slightly.

Final Thoughts

CF Industries fits Lynch’s model of “growth at a fair price”: a profitable, steadily expanding business trading below its true worth. Its sound financials, combined with a low valuation, make it a strong option for long-term investors.

For more stocks filtered using Peter Lynch’s criteria, see the full list here.

Disclaimer: This article is not investment advice. Do your own research or consult a financial advisor before making decisions.