BARRICK MINING CORP (NYSE:B) was identified by our Decent Value stock screener as a candidate with solid fundamentals and an attractive valuation. The company operates gold and copper mines across multiple countries, with strong profitability metrics and reasonable growth prospects. Here’s why B stands out as a potential value play.

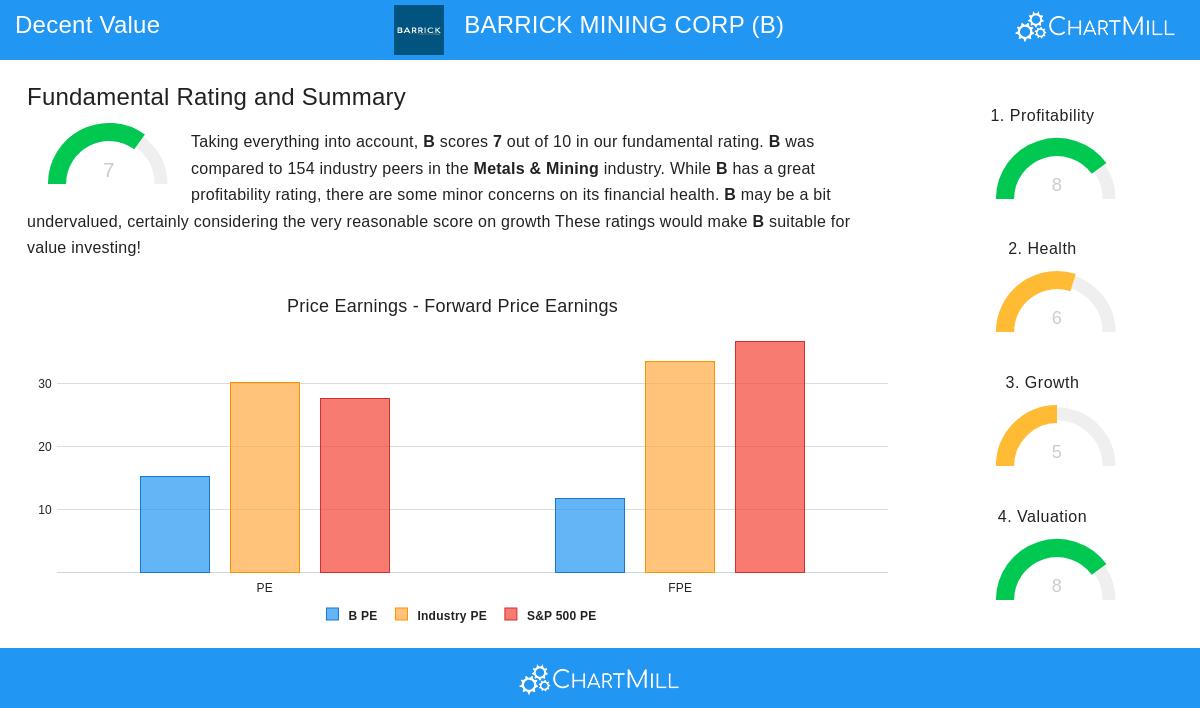

Valuation

Barrick Gold’s valuation metrics suggest the stock may be trading below its intrinsic value:

- P/E Ratio: At 15.20, B’s P/E is lower than 85.7% of its industry peers and well below the S&P 500 average of 27.53.

- Forward P/E: The forward P/E of 11.62 indicates further earnings growth is expected, yet the stock remains cheaper than 76% of competitors.

- Enterprise Value/EBITDA: 88.3% of industry peers are more expensive based on this metric.

- PEG Ratio: A low PEG ratio suggests the stock is reasonably priced relative to its earnings growth potential.

Profitability

Barrick scores an 8/10 in profitability, with several strengths:

- Operating Margin: At 36.66%, it outperforms 90.9% of industry peers.

- Return on Equity (ROE): 9.5%, better than 76% of competitors.

- Profit Margin: 17.46%, ranking in the top 15% of the sector.

Despite a slight decline in profit margins recently, operating margins have improved, reflecting cost efficiency.

Financial Health

With a Health rating of 6/10, Barrick maintains a stable financial position:

- Debt Management: A Debt/Equity ratio of 0.19 indicates low reliance on borrowing.

- Liquidity: Strong current and quick ratios (2.87 and 2.16, respectively) suggest ample short-term financial flexibility.

- Concerns: The Altman-Z score of 1.55 signals some financial risk, though the company’s free cash flow covers debt obligations comfortably.

Growth

Barrick’s Growth rating of 5/10 reflects moderate but stable expansion:

- Past Performance: EPS grew 60.7% in the last year and 19.6% annually over five years. Revenue increased 15.7% YoY.

- Future Expectations: Analysts project 12.9% annual EPS growth, though revenue growth may slow to 4.7%.

Dividend

The company offers a 1.9% dividend yield, slightly below the industry average but with a sustainable payout ratio of 29.8%. Dividend growth has been modest at 1.4% annually.

Our Decent Value screener lists more stocks with strong valuations and fundamentals.

For a deeper dive, review the full fundamental report on BARRICK MINING CORP.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should conduct your own analysis before making investment decisions.