A “Santa Rally” Starts With a Stumble

After a powerful rebound last week, major U.S. indices opened the final month of 2025 on the back foot. The Dow Jones slid about 0.6%, the S&P 500 lost roughly 0.3%, and the Nasdaq Composite gave up just under 0.3%, trimming part of November’s late surge.

Breadth was clearly risk-off: decliners outpaced advancers on both the NYSE and Nasdaq, and the move came alongside a noticeable jump in Treasury yields and another leg down in cryptocurrencies.

In other words: the party isn’t over, but the DJ definitely turned the volume down.

Manufacturing PMI Stuck in Contraction, Yields Pop

The main macro driver was the ISM Manufacturing PMI for November, which slipped to 48.2, down from 48.7 in October and marking the ninth straight month of contraction in U.S. factory activity.

Sub-indices for new orders and employment weakened further, while prices paid ticked higher, exactly the kind of mix that keeps both growth worriers and inflation hawks awake at night.

Several survey respondents explicitly pointed to President Donald Trump’s tariff regime as a key headwind, citing higher input costs and the need to consider moving production offshore.

Bond markets reacted quickly. The 10-year U.S. Treasury yield climbed roughly 7 basis points to around 4.09%, its highest level in about two weeks, as a spike in Japanese government bond yields and speculation about a future Bank of Japan rate hike spilled over into global rates.

For equity investors, that’s a classic double whammy: weaker growth signals on one side, higher discount rates on the other.

Fed Cut Still “Baked In,” but Politics Hover in the Background

Despite Monday’s jitters, futures markets continue to price an ~85–90% probability of a 25 bps rate cut at the December 9–10 FOMC meeting, following October’s earlier quarter-point move.

The story is less about whether the Fed cuts and more about what comes next:

-

A growing bloc of FOMC members is openly skeptical about additional easing.

-

Chair Jerome Powell’s term ends in May, and President Trump has hinted he has already chosen the next Fed chair - widely speculated to be White House economic adviser Kevin Hassett - but hasn’t confirmed anything yet.

That political overhang matters. A Fed seen as less independent typically commands a higher risk premium in both bonds and equities, something to keep in mind as we move deeper into December.

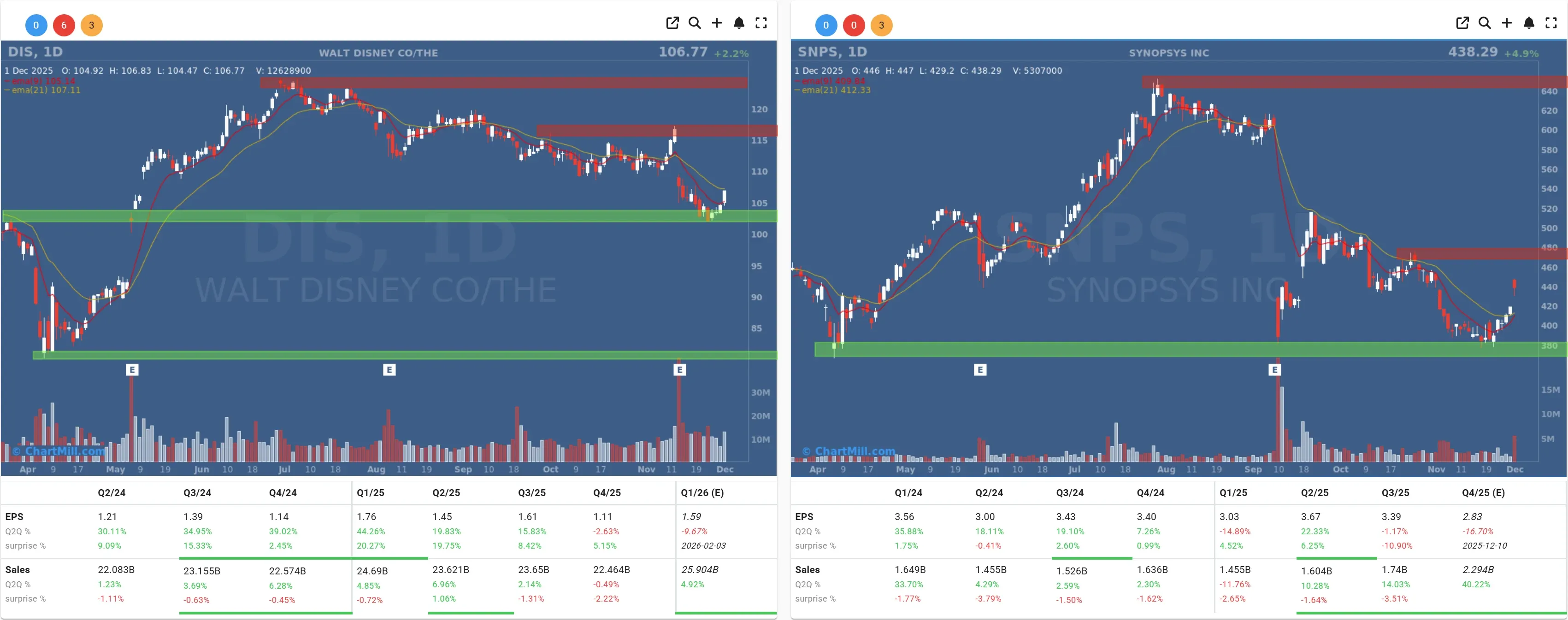

Stock Stories: Disney and Synopsys Buck the Trend

Amid the macro noise, a few single-name stories stood out.

Walt Disney (DIS | +2.2%) rode a surprisingly old-school catalyst: a blockbuster animated sequel. “Zootopia 2” pulled in roughly $556 million worldwide in its first week, with an eye-catching $260 million coming from China alone, despite ongoing U.S.–China trade frictions.

The stock added a bit more than 2% on Monday as investors rewarded the combination of strong box office momentum and the signal that Disney’s content engine is still very much alive.

Synopsys (SNPS | +4.85%) did even better, jumping close to 5% after Nvidia disclosed a $2 billion equity stake alongside an expanded collaboration around chip-design software.

For me, that deal is a useful tell: even as investors cool a bit on richly valued AI names in aggregate, the plumbing of the AI ecosystem - design tools, infrastructure and enabling software - is still attracting serious capital.

By contrast, Apple (AAPL | +1.52%) managed only a modest gain and Alphabet (GOOGL | -1.65%) slipped slightly, a reminder that the “race for the top dog in market cap” can be brutal when valuations are already stretched.

Crypto Crash: Bitcoin Takes the Stairs Down

The real shock absorber of the day wasn’t equities, it was Bitcoin.

The cryptocurrency tumbled roughly 7%, briefly dipping below $85,000 before clawing back to the mid-$80,000s.

The move was tied to a toxic mix of:

- Rising global yields and an unwind of yen-funded carry trades.

- Concerns about Fed and BOJ policy trajectories.

- Old-fashioned risk aversion after a long, speculative run-up.

Strategy’s (MSTR | -3.25%) move is particularly telling: the company - the largest corporate holder of Bitcoin - effectively admitted that its previous earnings guidance assumed BTC near $150,000 by year-end. It now pencils in a much wider $85,000–$110,000 range and is raising equity to build a fiat cushion.

In plain English: when the loudest “never sell” voice in Bitcoin starts quietly stockpiling dollars, I take note.

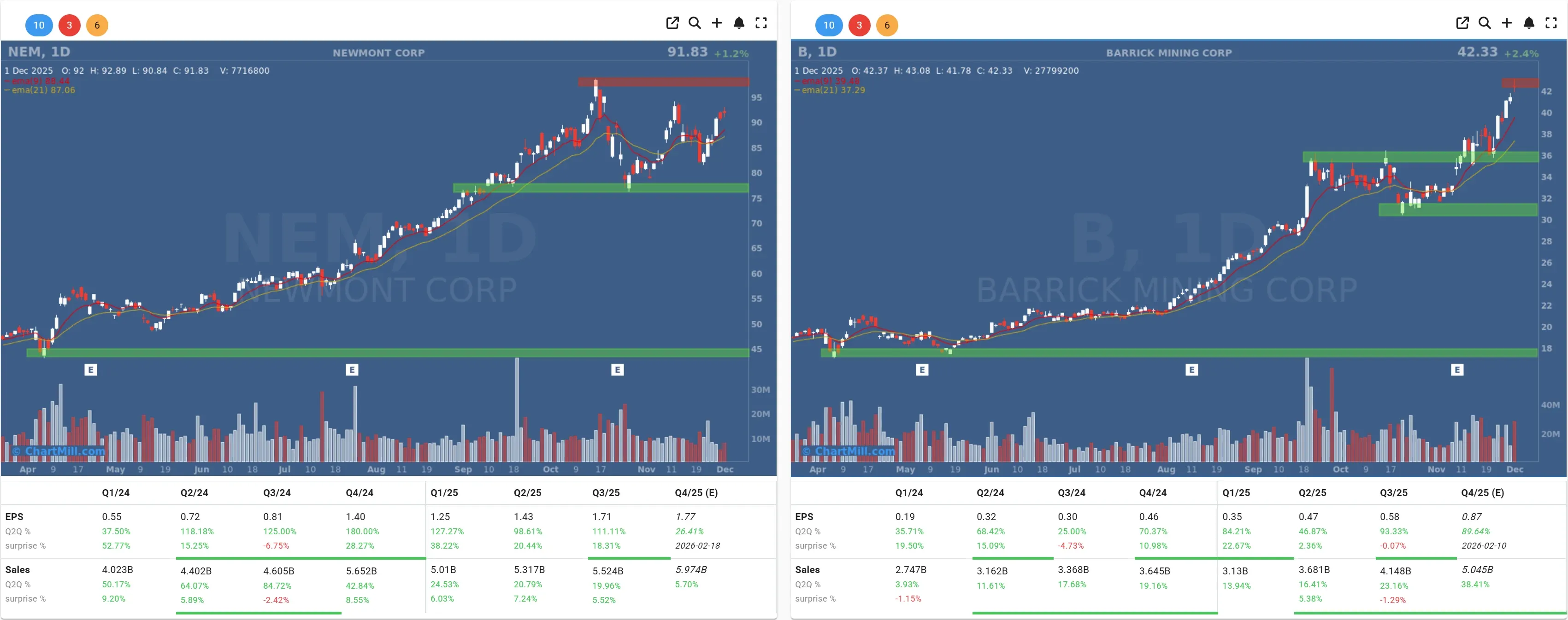

Silver Steals the Commodity Spotlight, Barrick Considers an IPO

While crypto imploded, precious metals continued their very different kind of melt-up.

Silver futures broke to fresh record highs near $58 per ounce, more than doubling year-to-date, powered by a cocktail of industrial demand (notably from solar and EVs) and a rotation from gold into “cheaper” hedges.

That strength helped gold and silver miners:

Barrick Mining (B | +2.39%) and Newmont (NEM | +1.21%) both advanced, with Barrick adding another catalyst by confirming it is evaluating an IPO of its North American gold assets into a separate, publicly listed vehicle.

The idea is straightforward: carve out the “crown jewels” - Nevada, Pueblo Viejo, and other low-risk, high-quality operations - into a purer gold play that might command a higher multiple, while Barrick retains control and uses proceeds to de-risk the rest of the portfolio.

If silver and gold stay anywhere near these levels and the Fed does indeed cut next week, I’d expect more corporate engineering like this across the sector.

Meanwhile, OPEC+ decided over the weekend to keep oil output unchanged for Q1 2026, choosing stability over grabbing market share at a time when demand questions and non-OPEC supply growth are keeping a lid on prices. Crude reacted with a modest bounce, but nothing that fundamentally changed the energy narrative.

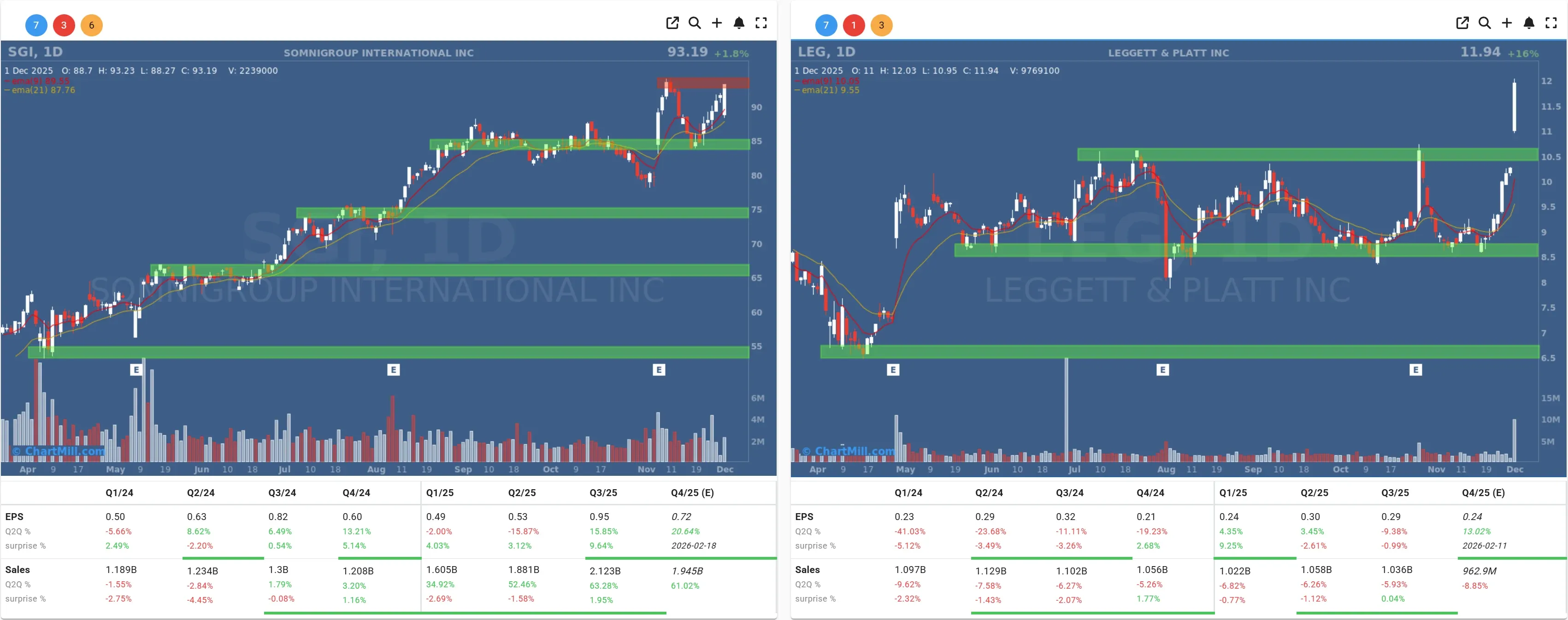

Deal Talk in the Mattress Aisle: Somnigroup Goes Shopping

Away from the headline-grabbing sectors, we also saw some good old-fashioned M&A.

Leggett & Platt (LEG | +16.37%) soared more than 16% after Somnigroup International (SGI | +1.82%) - the newly named bedding giant formed from Tempur Sealy’s roll-up of Mattress Firm - proposed an all-stock acquisition valuing Leggett at $12 per share, roughly a 30% premium to its 30-day average.

For Somnigroup, the logic is scale and vertical integration in the global sleep market. For Leggett shareholders, the offer crystallizes value after a difficult few years and gives them equity in a more diversified, higher-margin group.

It’s not Nvidia-buys-Synopsys-type fireworks, but it does fit a broader pattern: in a slower-growth, higher-rate environment, boards are more willing to use their stock as currency to rationalize capacity and chase synergies.

How I Read the Market Mood

Put together, Monday’s tape tells a fairly coherent story:

Macro: Manufacturing is in a clear, tariff-driven contraction, but services and consumption remain resilient enough that the Fed can move slowly rather than panic.

Rates: Higher long yields are re-introducing valuation discipline, especially for “bond-proxy” sectors like utilities and REITs.

Risk: Frothiest pockets - crypto and some hyper-growth AI plays - are seeing the sharpest air pockets, while solid franchises with real cash flows (think Disney, Synopsys) still find buyers on good news.

I wouldn’t call this a regime change; it looks more like a healthy check-up after a strong rally into year-end hopes. But the combination of:

-

a binary-feeling Fed decision next week,

-

an increasingly political rates backdrop under a second Trump administration, and

-

clear stress in speculative corners like Bitcoin

means volatility can pick up very quickly if the data or the Fed’s messaging disappoints.

What I’m Watching Next

Going into the rest of this week and next, here’s what I’ll be watching most closely:

-

Fed communication around the December cut, does Powell frame this as “one and done” or the start of a mini-cycle?

-

Follow-through in crypto and high-beta tech, another leg lower there could start to spill more aggressively into broader risk assets.

-

Positioning in cyclicals vs. defensives, if manufacturing weakness deepens and yields stay elevated, we may see a more pronounced rotation rather than the modest rebalancing we saw yesterday.

For now, the message from Monday is simple: December may still deliver a Santa rally, but the sleigh is going to have to navigate tariffs, central bank politics and some very nervous crypto traders on the way.

Kristoff - ChartMill

Next to read: Market Breadth Cools at Resistance: Strong November Thrust Meets First Real Test