Carvana Co (NYSE:CVNA) operates an e-commerce platform for buying and selling used cars, offering a streamlined digital experience for consumers. The company has gained attention for its innovative approach, including vehicle vending machines and same-day delivery options.

Louis Navellier’s The Little Book That Makes You Rich outlines eight key rules for identifying high-growth stocks. These principles focus on earnings revisions, sales growth, profitability, and cash flow strength. Carvana (NYSE:CVNA) aligns with several of these criteria, making it a potential candidate for growth investors.

How Carvana (NYSE:CVNA) Fits the Little Book Criteria

-

Positive Earnings Revisions

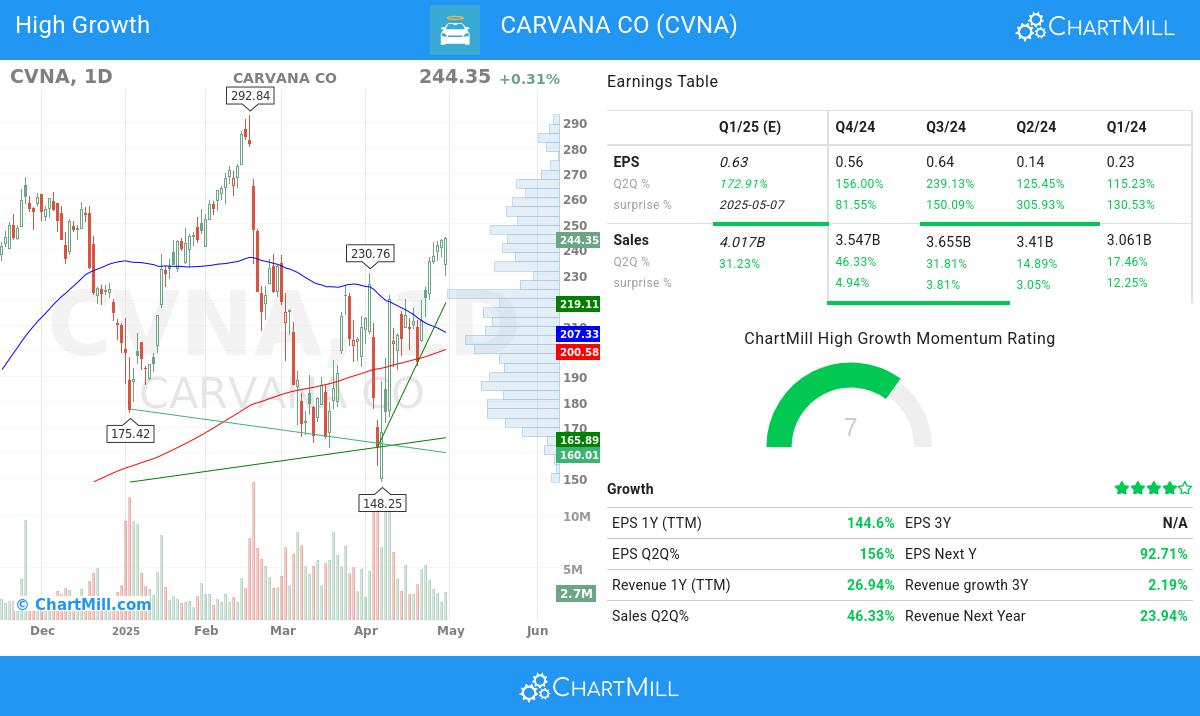

Analysts have raised EPS estimates for the next quarter by 25.59% over the past three months, indicating improving confidence in Carvana’s near-term performance. -

Positive Earnings Surprises

The company has beaten EPS estimates in all of the last four quarters, with an average surprise of 167.03%. -

Increasing Sales Growth

Revenue grew 26.94% year-over-year, while quarterly sales surged 46.33% compared to the same period last year. -

Expanding Operating Margin

Operating margin growth over the past year stands at an impressive 1,198.42%, reflecting improved profitability. -

Strong Cash Flow

Free cash flow increased by 15.50% year-over-year, supporting the company’s ability to fund operations and growth. -

Earnings Growth

EPS grew 144.60% year-over-year, with quarterly EPS up 156.00% compared to the prior year. -

Positive Earnings Momentum

The latest quarterly EPS growth (156.00%) significantly outpaces the same quarter’s performance from a year ago (-356.41%). -

High Return on Equity

Carvana’s ROE of 16.67% is above the industry average, indicating efficient use of shareholder capital.

Fundamental Analysis Summary

Carvana (NYSE:CVNA) holds a fundamental rating of 5 out of 10, reflecting mixed financial health but strong growth potential. Key takeaways include:

- Profitability: Solid operating margin (7.24%) and improving gross margins.

- Financial Health: High debt levels (Debt/Equity of 4.22) but strong liquidity (Current Ratio of 3.64).

- Valuation: Expensive on traditional metrics (P/E of 155.64), but growth prospects may justify the premium.

- Growth: Revenue and earnings are expanding rapidly, with expectations for continued double-digit growth.

For a deeper analysis, review the full fundamental report here.

Finding More Growth Stocks

Investors looking for similar high-growth candidates can explore our pre-configured Little Book growth screen.