Value investing focuses on finding stocks priced below their true worth while keeping strong financial foundations—a method introduced by Benjamin Graham and improved by Warren Buffett. This strategy looks for companies with good earnings, solid financial positions, and steady growth potential, all while being available at lower prices. Zimmer Biomet Holdings Inc (NYSE:ZBH) stands out as a potential match for this method, performing well on price measures without compromising financial strength or earnings quality.

Valuation: An Attractive Discount

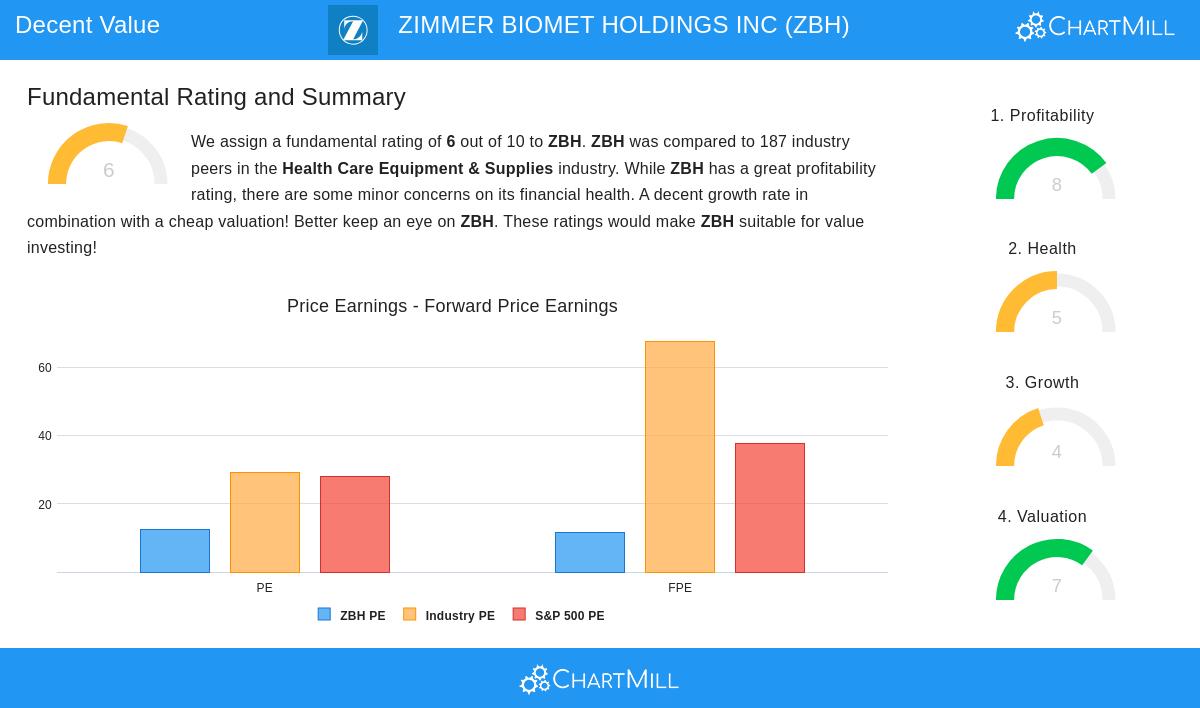

ZBH’s price metrics indicate it is priced much lower than its sector and the overall market. Key points from its fundamental analysis report include:

- Price/Earnings (P/E) of 12.40, far below the sector average of 29.10 and the S&P 500’s 28.04. This puts ZBH in the top 10% of its industry for affordability.

- Price/Forward Earnings of 11.62, showing steady earnings expectations at a lower price.

- Enterprise Value/EBITDA and Price/Free Cash Flow ratios are both more favorable than nearly 90% of similar companies, confirming its undervalued position.

For value investors, these numbers suggest a safety net—a key idea in Graham’s approach. The low P/E and strong cash flow ratios hint that the market might not fully recognize ZBH’s earnings potential.

Profitability: Strong Performance

Even with its lower price, ZBH maintains high profitability, earning 8/10 in ChartMill’s evaluation:

- Operating Margin of 19.59% beats 92.5% of healthcare equipment competitors.

- Return on Equity (7.37%) and Return on Invested Capital (5.99%) are above industry averages, showing effective use of capital.

- Consistent Gross Margins (71.05%) highlight pricing strength and cost efficiency.

Strong profitability is vital for value stocks, as it lessens the need for risky growth bets and supports steady returns. ZBH’s margins suggest it can handle economic shifts better than weaker rivals.

Financial Health: Balanced Risks

With a Health rating of 5/10, ZBH has minor issues but no major warnings:

- Debt/Equity of 0.53 is acceptable, though slightly higher than sector standards.

- Current Ratio of 2.44 means it has enough liquidity to meet short-term needs.

- Altman-Z Score of 2.63 points to low near-term bankruptcy risk.

While the debt level should be watched, ZBH’s steady cash flow (positive for over 5 years) and share repurchases show careful financial management—a positive for value investors focused on reducing risk.

Growth: Steady and Improving

ZBH’s Growth rating of 4/10 reflects slower past trends but brighter future prospects:

- Revenue and EPS are expected to grow around 5% yearly, recovering from earlier drops.

- Positive EPS momentum indicates operational gains are starting to show.

For value investors, even slight growth can boost returns when paired with a low starting price. ZBH’s direction fits the strategy’s emphasis on "inexpensive but stable" businesses.

Conclusion

Zimmer Biomet represents the core of value investing: a financially healthy company trading at a discount due to overlooked or short-term factors. Its mix of low price, high profitability, and balanced debt makes it worth considering—especially for investors interested in the durable healthcare sector.

To find more stocks like this, check the Decent Value Stocks screener.

Disclaimer: This analysis is not investment advice. Always do your own research or consult a financial expert before making investment choices.