The close: green screens, but with some very loud red exceptions

Stocks ended Friday, December 19, 2025, higher for a second day as tech regained its footing. The Dow closed at 48,134.89 (+0.4%), the S&P 500 at 6,834.50 (+0.9%), and the Nasdaq at 23,307.62 (+1.3%).

The broad takeaway I’m left with: the market is still willing to pay up for “AI + certainty,” but it has zero patience for “consumer + uncertainty,” especially when China exposure and pricing power look wobbly.

The catalyst: TikTok drama flips into an Oracle-powered relief rally

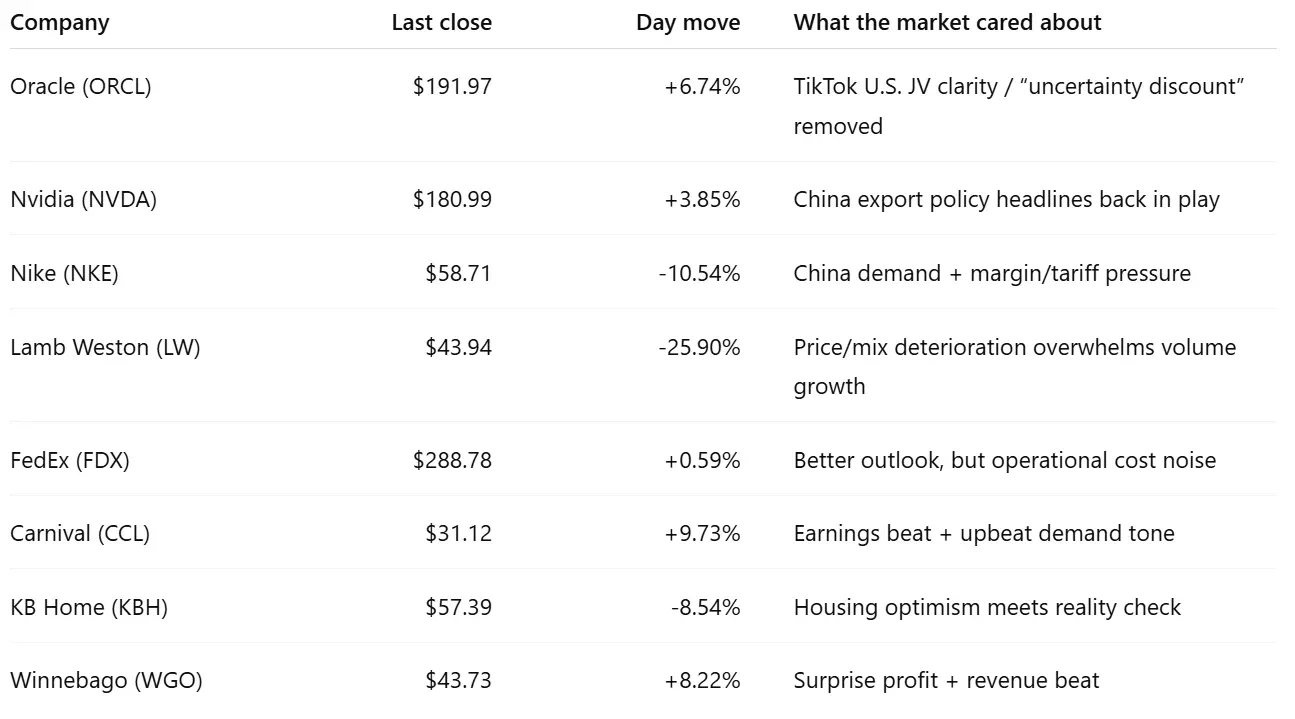

The day’s headline move belonged to Oracle (ORCL | +6.63%), after news around a TikTok U.S. joint venture involving Oracle, Silver Lake, and Abu Dhabi-backed MGX, with ByteDance retaining a minority stake.

Whether you love or hate the policy backdrop, markets love reduced uncertainty even more. This story has dragged on for years; the moment it started to look like a concrete structure (board control, data hosting, governance), traders treated it like an all-clear signal.

AI trade mood: Nvidia back on its feet, but geopolitics is still the chaperone

Nvidia (NVDA | +3.93%) joined the rebound as the market reacted to reporting that the U.S. is reviewing/considering pathways around advanced AI chip sales to China, after earlier policy signals around allowing certain shipments with conditions.

This is bullish for headline momentum, but it’s not “clean bullish.” Export rules are now basically a tradable asset class. Every new phrase like “approved customers” or “review” can move billions in market cap before lunch.

The two faceplants: Nike and Lamb Weston remind everyone what “pricing pressure” looks like

Not every company got invited to the AI afterparty.

Nike (NKE | -10.54%) slid hard after quarterly results reignited concerns about China weakness and margin pressure tied to tariffs and promotions.

And then there was Lamb Weston (LW | -25.94%), a one-day crater. The market wasn’t impressed that volumes rose if it came alongside an ugly price/mix decline, which is the corporate version of “we sold more, but made it worse.”

Quick scoreboard: the session’s loudest movers

Here’s the clean snapshot of the names that actually moved the narrative:

Macro pulse: soft-ish inflation vibes, but consumers still look tired

A cooler November CPI backdrop helped risk appetite, though the data has had caveats because the government shutdown disrupted some month-to-month collection.

Meanwhile, consumer confidence improved a touch, the University of Michigan sentiment index rose to 52.9, but it remains deeply depressed versus last year.

Housing offered a small positive: existing home sales rose 0.5% in November to a 4.13 million annual pace, per the NAR, though affordability and inventory dynamics still keep the sector from feeling “healthy.”

Geopolitics and policy: oil firm, drug pricing pressure, and the risk nobody can model

Oil pushed higher as geopolitics intruded again, including U.S. actions around Venezuelan-linked supply flows and ongoing Russia/Ukraine uncertainty. Brent settled near $60.47 and WTI around $56.66 on Friday.

Policy also hit the tape: the White House announced agreements tied to “most-favored-nation” style pricing access for state Medicaid programs across products from nine drugmakers. If you’re watching pharma, this is the kind of headline that can sit quietly for a day… and then suddenly matter a lot when guidance season starts.

And for currency context, the ECB reference rate showed EUR/USD at 1.1712 on Dec. 19.

What I’m watching into Monday

If Friday was about relief, Monday is about follow-through.

-

Does the AI bid broaden beyond the usual suspects, or does it stay concentrated in a handful of “policy-sensitive” winners?

-

Do consumer-facing names stabilize, or does the market keep punishing anything that smells like discounting and China weakness?

-

Does crude keep climbing on geopolitics, nudging inflation expectations back up right when investors want the “soft landing” story to stay simple?

Kristoff - ChartMill

Next to read: Market Breadth Update - Repair Crew Still on the Job, But Resistance Overhead