Peter Lynch’s investment strategy, described in One Up on Wall Street, centers on finding companies with steady growth at fair prices. His method combines growth and value investing, focusing on key financial measures like earnings growth, profitability, and financial stability. The aim is to identify firms capable of providing reliable long-term returns without paying too much for their future prospects.

One stock that meets Lynch’s standards is WESTERN DIGITAL CORP (NASDAQ:WDC). The firm, a major player in data storage, supplies cloud, client, and consumer markets with hard disk drives (HDDs) and solid-state drives (SSDs). Here, we explore why WDC fits the GARP (Growth at a Reasonable Price) model.

Key Metrics Matching Peter Lynch’s Approach

-

Steady Earnings Growth

Lynch preferred firms with reliable earnings growth, usually between 15% and 30%. WDC’s 5-year EPS growth of 16.66% fits this range, showing stable profitability without overextension.

Although revenue has dropped recently (-15.7% YoY), the company’s earnings recovery (EPS up 1,828.95% YoY) points to better operational efficiency. -

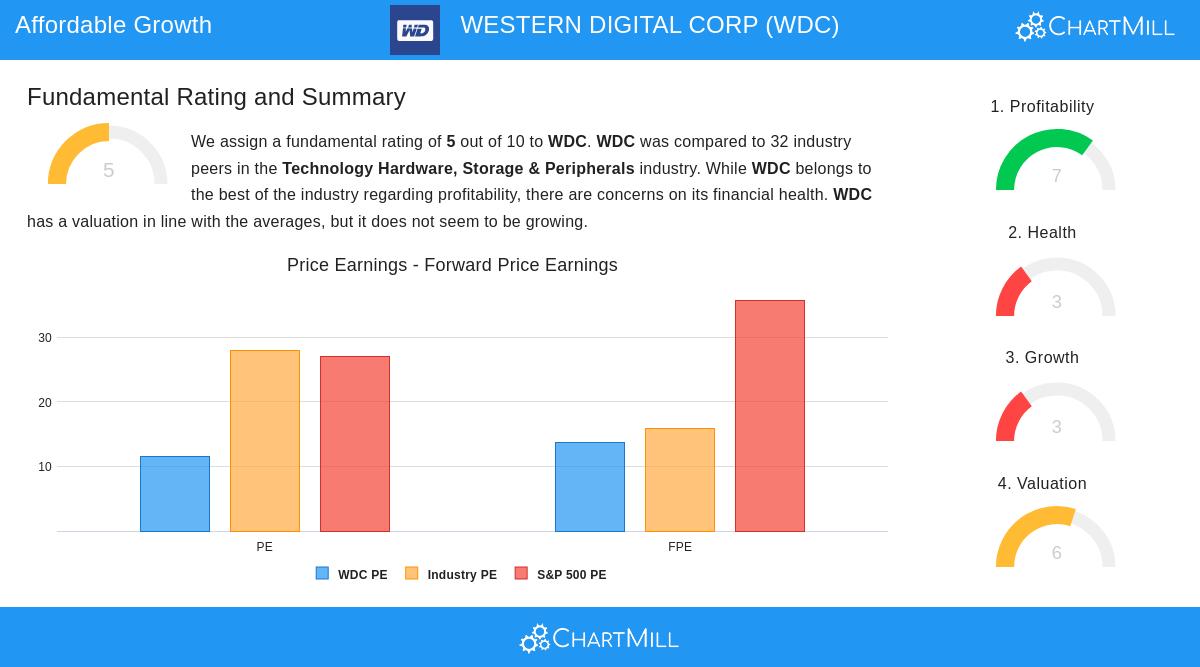

Fair Valuation (PEG Ratio ≤ 1)

A key Lynch measure, the PEG ratio (0.69), adjusts the P/E ratio by earnings growth. A PEG under 1 suggests the stock is priced below its growth potential.

WDC’s P/E of 11.58 is also lower than the industry (27.97) and S&P 500 (27.11) averages, supporting its reasonable price. -

High Profitability (ROE > 15%)

Lynch valued strong Return on Equity (ROE) as a sign of efficient capital use. WDC’s ROE of 33.25% places it in the top 7% of its sector, reflecting solid profitability.

Similarly, its Return on Invested Capital (ROIC) of 25.82% beats 87.5% of competitors, showing effective earnings reinvestment. -

Solid Balance Sheet (Debt/Equity < 0.6)

Financial health was important to Lynch. WDC’s Debt/Equity ratio of 0.45 is well under the 0.6 limit, indicating a cautious capital structure.

However, liquidity measures like the Current Ratio (1.08) and Quick Ratio (0.84) are less strong, an area for closer review.

Fundamental Overview

WDC’s fundamental report shows strengths in profitability and valuation but flags issues like falling revenue and liquidity. The company’s margins (38% Gross, 21% Operating) lead its industry, and its debt is under control. While short-term growth forecasts are modest (EPS expected to drop -0.37% yearly), the stock’s low price and high capital returns hint at long-term promise.

Why This Appeals to GARP Investors

Lynch’s strategy skips overpriced growth stocks for fairly priced firms with strong track records. WDC’s metrics—especially its PEG ratio, ROE, and debt levels—match this thinking. The stock carries risks (e.g., fluctuating storage demand), but its valuation and profitability offer some protection.

For investors hunting similar opportunities, the Peter Lynch screen lists other stocks meeting these standards.

Disclaimer: This analysis is for educational purposes only and is not investment advice. Do your own research or consult a financial advisor before investing.