The "Decent Value" screen finds stocks with solid fundamentals that seem priced lower than their true worth, a key idea in value investing. This approach, based on the methods of Benjamin Graham and improved by Warren Buffett, looks for companies priced below their fair value while showing good financial health, earnings, and growth prospects. By selecting stocks with a high ChartMill Valuation Rating (7 or higher) and fair scores in Growth, Health, and Profitability, the screen tries to spot chances where the market may not yet recognize the company’s real strength.

United Parcel Service-CL B (NYSE:UPS) appears as a match for this approach, with a fundamental rating of 6 out of 10, showing a mix of positives and areas to watch.

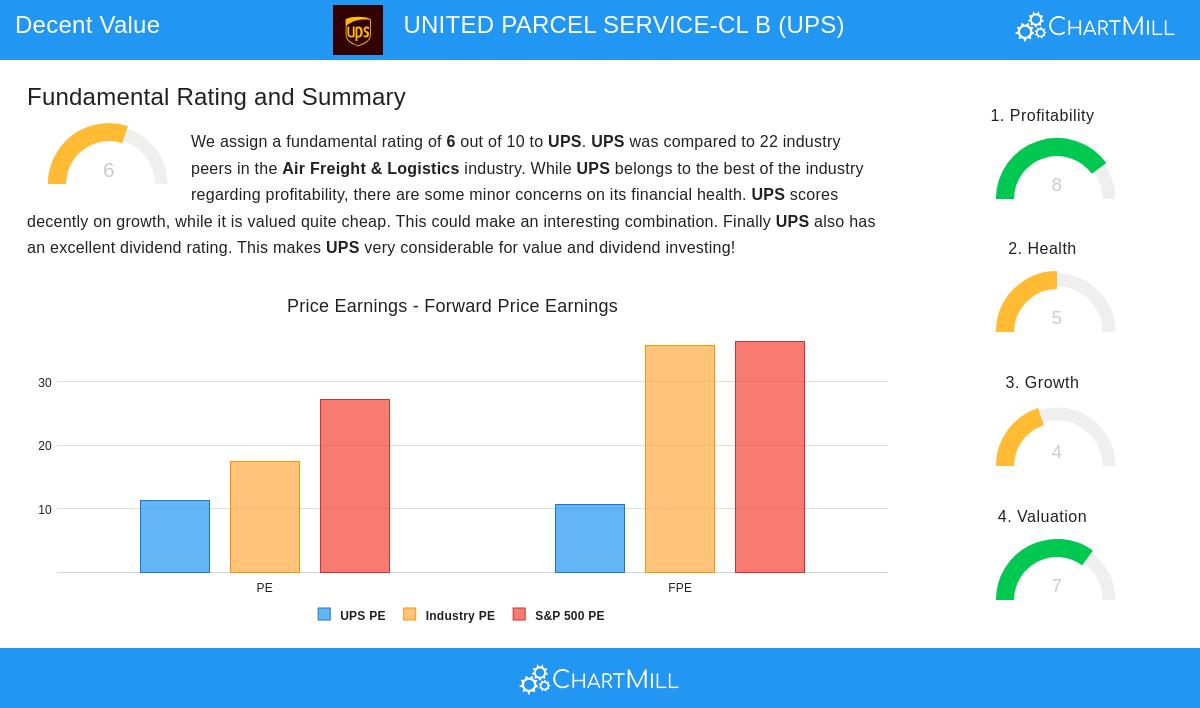

Valuation: An Attractive Price

UPS’s valuation numbers stand out, with a ChartMill Valuation Rating of 7. Key points include:

- Price/Earnings (P/E) Ratio of 11.26, well below the industry average (17.47) and the S&P 500 (27.24), meaning the stock is priced low compared to earnings.

- Price/Forward Earnings of 10.72, lower than 90.9% of peers in the Air Freight & Logistics sector.

- Enterprise Value/EBITDA and Price/Free Cash Flow ratios also show UPS trades at a lower price than most competitors.

For value investors, these numbers suggest a possible safety net—a way to avoid paying too much for future growth or unexpected risks.

Profitability: Strong but Slipping Slightly

UPS scores an 8 in Profitability, supported by:

- High margins: Gross Margin of 81.6% (best in its sector) and Operating Margin of 9.41%, better than 86% of peers.

- Good returns: Return on Equity (36.38%) and Return on Invested Capital (11.69%) rank among the top in the industry.

However, falling Operating Margin trends need attention, as they could hurt future earnings if not corrected.

Financial Health: Some Debt but Enough Cash

With a Health Rating of 5, UPS has both strengths and weaknesses:

- Solvency: A Debt/Equity ratio of 1.51 is higher than 72% of peers, showing debt use. Still, its Altman-Z score (2.92) and Debt/FCF ratio (6.97) are acceptable for the industry.

- Liquidity: Current and Quick Ratios (both 1.32) are enough to cover short-term needs.

While not perfect, UPS’s balance sheet works for its costly operations, but investors should keep an eye on debt.

Growth: Steady but Not Fast

UPS’s Growth Rating of 4 reflects slow but consistent progress:

- Revenue and EPS growth have averaged 4.2% and 0.5% yearly in recent years, with estimates suggesting a small rise (7.1% EPS growth expected).

- Dividend growth of 11.2% yearly over the past ten years shows management’s focus on shareholder returns, though the high payout ratio (94% of income) raises concerns about keeping it up.

For value investors, UPS’s growth fits a "slow and steady" style—favoring reliability over rapid expansion.

Conclusion: A Value Choice with Income Benefits

UPS makes a case for value investors looking for a financially stable company priced below its sector’s usual levels. Its strong earnings, dividend history, and lower price create an appealing balance of risk and reward, though debt and margin trends are worth noting.

For those wanting to find similar options, the Decent Value Stocks screen provides a list of stocks meeting these standards.

Disclaimer: This analysis is not investment advice. Investors should do their own research or talk to a financial advisor before making choices.