Universal Health Services (NYSE:UHS) functions as a principal healthcare service provider, owning and running a system of acute care hospitals and behavioral health facilities throughout the United States and in other countries. The company's wide collection contains about 359 inpatient facilities and 60 outpatient sites, presenting a full scope of medical services from general surgery to specific behavioral health treatments. This well-established operational base offers a firm base for steady revenue creation and market position in the healthcare industry.

Valuation Analysis

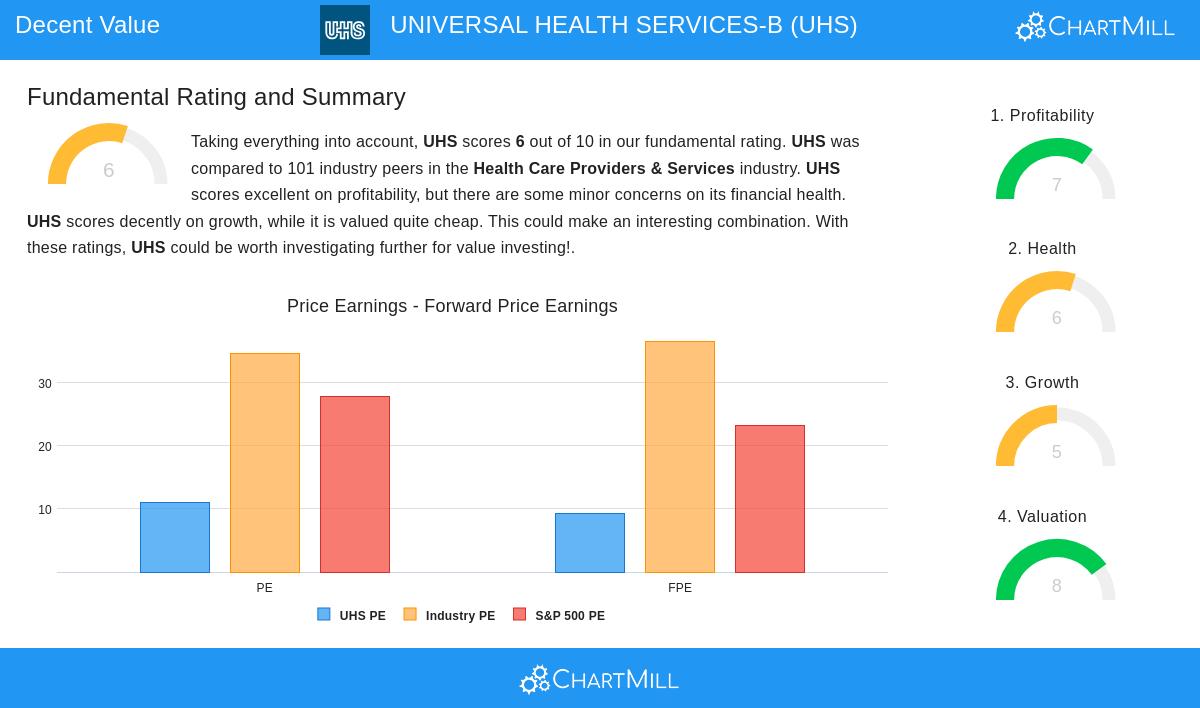

The fundamental review shows notable valuation measures that place Universal Health Services as possibly priced below its true worth compared to both industry counterparts and wider market indicators. The company's present valuation ratios indicate considerable potential for price growth, matching value investing ideas that look for securities priced under their inherent value.

Important valuation measures consist of:

- Price/Earnings ratio of 11.01, much below the industry average of 34.72

- Price/Forward Earnings ratio of 9.36, less expensive than 92% of industry rivals

- Enterprise Value to EBITDA ratio placing the company as more reasonably priced than 83% of sector counterparts

- PEG ratio showing acceptable payment for anticipated growth

These valuation traits are especially significant for value investors, as they offer the necessary buffer that Benjamin Graham highlighted in his initial value investing structure. The large price difference from industry averages implies the market could be mispricing Universal Health Services' operational soundness and future profit possibility.

Financial Health Assessment

Universal Health Services displays acceptable financial health with a ChartMill Health Rating of 6 out of 10. The company keeps a moderate capital framework and indicates progress in various important financial measures over recent quarters.

Observable health signs:

- Altman-Z score of 3.19 shows low bankruptcy danger and does better than 63% of industry counterparts

- Debt to Equity ratio of 0.65 matches industry standards while preserving financial adaptability

- Steady decrease in shares available via buybacks over one and five-year spans

- Current ratio of 1.29 gives sufficient immediate liquidity

For value investors, good financial health lessens the danger of lasting capital loss, a vital factor when investing in possibly underpriced securities. The company's controllable debt amounts and bettering balance sheet measures give extra certainty in its capacity to endure economic variations.

Profitability Profile

The company receives a firm ChartMill Profitability Rating of 7 out of 10, indicating effective operations and good returns on invested capital. Universal Health Services has shown steady profitability across numerous measures and time frames.

Profitability features:

- Return on Assets of 8.41% puts the company in the leading 8% of the industry

- Return on Equity of 17.94% does better than 86% of healthcare service companies

- Operating Margin of 11.01% is with the industry's top performers

- Positive profits and operating cash flow sustained during the previous five years

Lasting profitability is basic to value investing strategy, as it confirms the company's business structure and backs the estimation of inherent value. The good and steady profit creation offers confidence that the present undervaluation might signify a market mispricing rather than basic business decline.

Growth Trajectory

With a ChartMill Growth Rating of 5 out of 10, Universal Health Services indicates moderate but important growth across key financial measures. The company mixes past growth accomplishment with sensible future prospects.

Growth attributes:

- Earnings Per Share expanded 37.47% in the latest year

- Five-year average EPS growth of 10.74% shows steady increase

- Revenue rose 9.61% year-over-year with 6.82% average yearly growth

- Anticipated future EPS growth of 11.65% yearly supports continued valuation betterment

While not showing rapid growth, the company's stable development fits nicely with value investing concepts that favor lasting business progress over speculative fast-growth. The mix of sensible growth with major valuation discount forms a pleasing risk-return outline for persistent investors.

Investment Considerations

The fundamental review of Universal Health Services shows a company trading at a large discount to its inherent value while keeping firm operational performance. The full fundamental report gives extra information on these measures and their meanings for long-term investors. The company's good profitability, acceptable financial health, and steady growth, when joined with its pleasing valuation multiples, indicate possibility for price growth as the market acknowledges the difference between price and value.

Value investors looking for similar chances can review extra candidates using our Decent Value Stocks screening tool, which finds companies with good valuation traits together with acceptable basics across growth, health, and profitability measures.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice, recommendation, or endorsement of any security. Investors should conduct their own research and consult with financial advisors before making investment decisions. Past performance does not guarantee future results.