For investors looking for chances in the market, one lasting method is to search for companies trading below their estimated true worth. This method, called value investing, requires finding stocks that seem priced too low based on key measures while still showing good basic business condition. A typical filter used to locate such possibilities selects for stocks with good valuation scores, meaning they are inexpensive compared to their earnings or assets, while also keeping acceptable scores in earnings ability, money stability, and expansion. This pairing tries to steer clear of "value traps"—stocks that are inexpensive for a cause—and instead find companies where a low price may not match a basically healthy operation.

Universal Health Services (NYSE:UHS) is a well-known operator of acute care hospitals and behavioral health centers in the United States and the United Kingdom. Lately, this healthcare company has appeared on filters made to find acceptable value chances, offering a reason for investors to look at its basics more carefully.

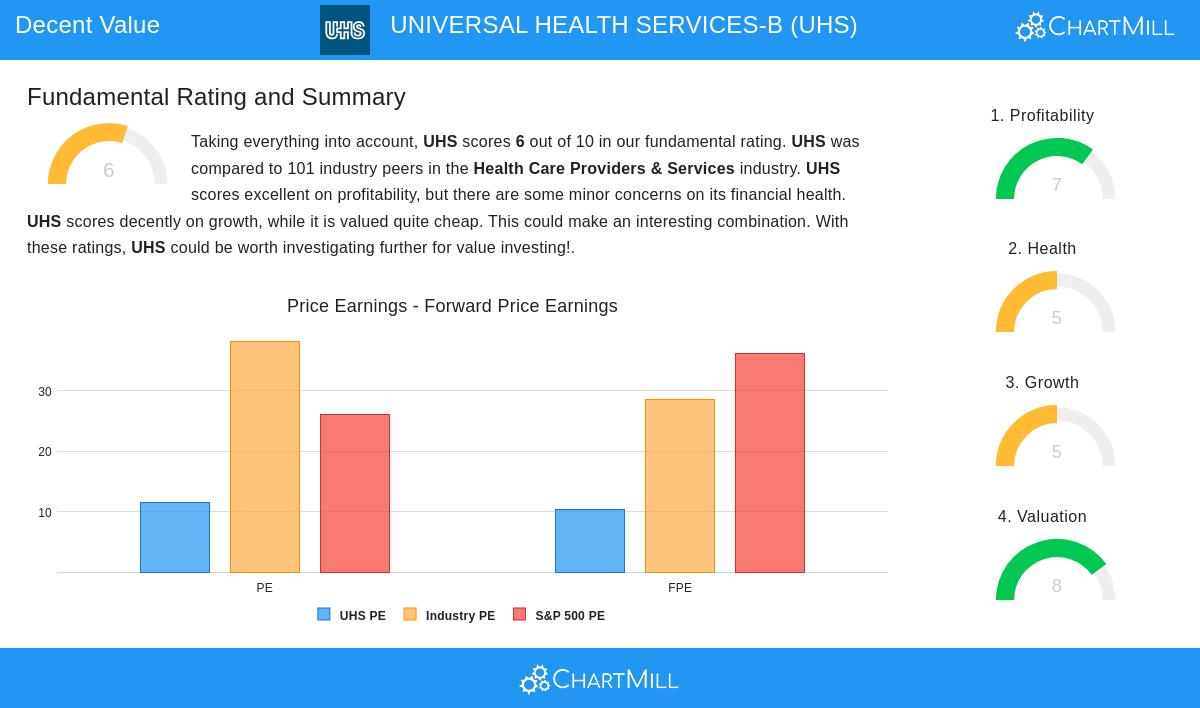

An Interesting Valuation View

The base of any value investment idea is a good price. Universal Health Services does well in this group, getting a high ChartMill Valuation Rating of 8 out of 10. The company's stock looks low-cost across several important measures when judged against both its industry group and the wider market.

- Price-to-Earnings (P/E) Ratio: At 11.51, the P/E ratio for UHS is much lower than the industry average of 38.23 and the S&P 500 average of 26.11. This makes it less expensive than about 89% of companies in the Health Care Providers & Services field.

- Forward P/E Ratio: The price assessment stays interesting looking forward, with a forward P/E of 10.27. This is also much lower than industry and market averages.

- Enterprise Value to EBITDA: This measure, which includes debt, gives more support to the low-price argument, with 82% of industry group companies having a higher price than UHS.

For a value investor, these numbers imply the market may be valuing UHS cautiously, possibly creating a buffer if the company's true worth is greater.

Evaluating Money Stability and Earnings Ability

An inexpensive stock is only a worthwhile investment if the company is financially stable and able to produce earnings. This is where the "acceptable" scores in stability and earnings become important, as they help remove troubled businesses. The basic report for UHS shows a varied but generally steady view.

Money Stability (Rating: 5/10): The company's financial condition is satisfactory, though not free from small issues. Its Altman-Z score of 3.28 shows a small short-term failure risk, and it does better than 69% of its group on this gauge. The debt-to-equity ratio of 0.55 shows some use of debt funding but is still better than 60% of the industry. The main point for care is cash availability: both its Current and Quick ratios are under industry averages, suggesting it may have less ease to meet immediate responsibilities compared to some group companies.

Earnings Ability (Rating: 7/10): This is a definite positive for UHS. The company has been regularly profitable with positive cash flow over the last five years. Its return gauges are especially notable:

- Return on Assets (ROA): 8.96%, doing better than 94% of the industry.

- Return on Equity (ROE): 19.18%, doing better than 88% of the industry.

- Return on Invested Capital (ROIC): 12.33%, also doing better than 88% of group companies.

Good and steady earnings ability is a central part for value investors, as it shows the company's skill in using its money well and creating profits—the very profits that support a higher true worth.

Expansion Path and Future View

While pure value stocks sometimes miss expansion, the filter looks for companies with an acceptable expansion outline to give a reason for price increase. The Growth Rating of 5/10 for UHS shows a good, if not amazing, path.

The company has posted good recent results, with Earnings Per Share (EPS) increasing 40.07% over the past year and Revenue increasing 10.21%. Over a longer time, EPS has increased at an average yearly rate of 10.74%. Looking ahead, experts expect EPS expansion to continue at a good rate of about 13.53% on average. This expected quickening in earnings expansion, when joined with a low P/E ratio, leads to a good PEG ratio, giving more support to the price assessment argument.

Conclusion: A Subject for Value-Focused Inspection

Universal Health Services presents an outline that matches the ideas of searching for low-priced stocks with good basics. Its notable valuation measures suggest the market may be missing its steady earnings ability and stable expansion potential. The small cash availability points in its stability score are seen but look balanced by good solvency and very high returns on capital. For investors using a value-centered plan, UHS represents a situation where a low price may be joined with a basically sound business in the necessary healthcare field, calling for more review.

You can see the full basic analysis report for Universal Health Services here: UHS Fundamental Analysis.

Want to find more stocks that match this outline? Our "Decent Value" filter is made to find companies with good valuation scores along with acceptable basics. Click here to see the current filter results and look at other possible chances.

Disclaimer: This article is for information only and does not make up financial guidance, a suggestion to buy or sell any security, or a support of any investment plan. Investors should do their own study and talk with a registered financial advisor before making any investment choices.