Travel + Leisure Co (NYSE:TNL) has been found using a methodical screening process made to find investment possibilities that may be undervalued. The selection process concentrates on businesses showing good basic valuation measurements while keeping acceptable results in profitability, financial condition, and expansion. This method fits with value investing ideas, where investors look for securities priced under their real worth while making sure the main business keeps acceptable operational basics. The screening rules specifically aim for stocks with valuation grades over 7, supported by satisfactory results in other basic groups, forming a well-rounded profile that could interest investors searching for value possibilities without extreme basic dangers.

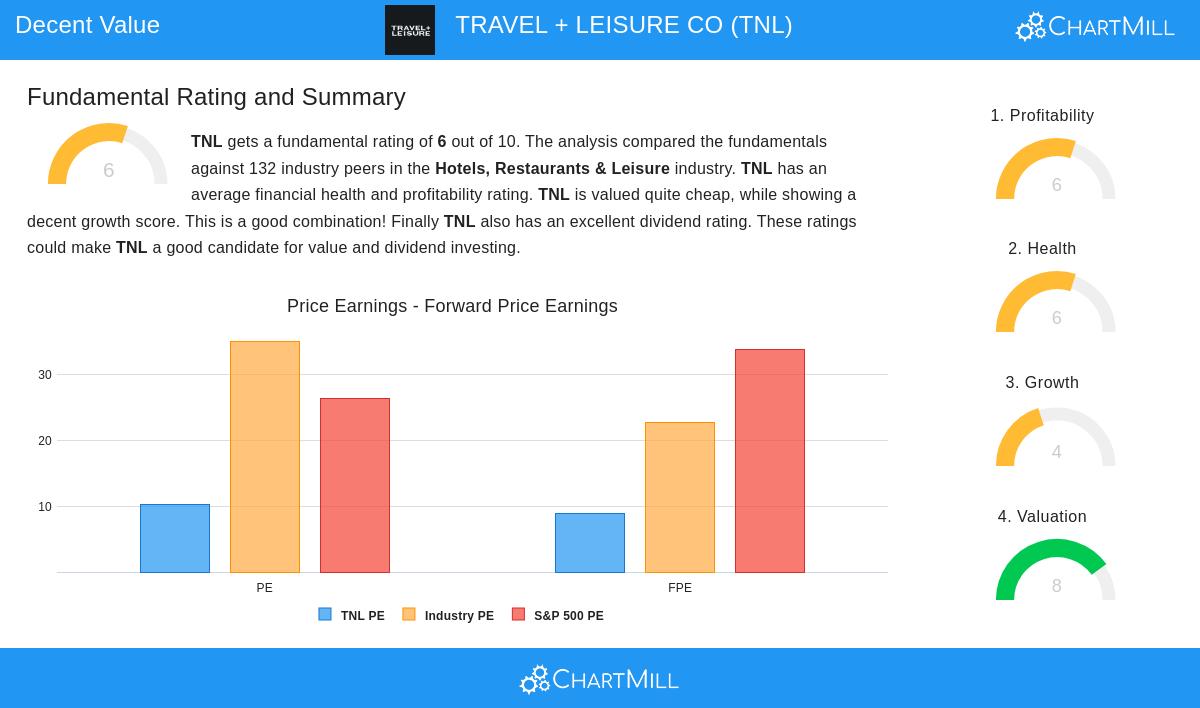

Valuation Review

The company's valuation measurements show a strong case for possible undervaluation. Travel + Leisure Co trades at notable price reductions when measured against both industry counterparts and wider market benchmarks, implying the market may not be completely acknowledging the company's earnings capacity.

• Price-to-Earnings ratio of 10.18, much lower than the industry average of 35.06 and S&P 500 average of 26.35 • Forward P/E ratio of 8.83, showing expected earnings expansion at a good valuation • Enterprise Value to EBITDA ratio placing the company more inexpensive than 61% of industry rivals • Price-to-Free Cash Flow ratio more inexpensive than 92% of industry counterparts

These valuation measurements are especially significant for value investors since they give numerical proof that the stock could be trading under its real value. The lower multiples relative to both the industry and wider market form a possible safety buffer, a key idea in value investing where investors look for security against calculation mistakes in their valuation assessments.

Financial Condition and Stability

Travel + Leisure Co shows acceptable financial condition with specific force in liquidity measurements, although some debt matters need observation. The company's balance sheet indicates good short-term financial adaptability.

• Current Ratio of 3.79 and Quick Ratio of 2.76, both doing better than about 95% of industry counterparts • Lowering debt-to-assets ratio compared to the prior year • Steady share count decrease over one and five-year spans • Altman-Z score of 2.39 shows limited bankruptcy danger, although not in the most secure group

For value investors, financial condition is important because it lessens the danger of lasting capital loss. Businesses with good liquidity situations can endure economic slumps and maintain operations without turning to share-diluting funding or extreme steps that could damage shareholder value. The bettering debt measurements and share count decrease show management's dedication to reinforcing the balance sheet.

Profitability Examination

The company keeps acceptable profitability with several measurements doing better than industry averages, although some margin tightening has appeared lately.

• Return on Invested Capital of 10.73%, doing better than 74% of industry rivals • Profit Margin of 10.36% puts the company in the top quarter of the industry • Operating Margin of 19.84% is higher than almost 79% of industry counterparts • Positive earnings and operating cash flow in four of the last five years

Profitability is necessary in value investing because it confirms the business model's longevity. A company trading at lower valuations must show the capacity to produce steady returns, or else the low multiples might just show basic business decline rather than market mispricing.

Expansion Outlook

While past expansion has been moderate, future signs point to speeding up performance, especially in earnings expansion.

• Expected EPS expansion of 14.61% each year over coming years • Revenue expansion speeding up from past drops to estimated 4.14% yearly rises • Bettering expansion path with both EPS and revenue expansion rates speeding up

Expansion thoughts supplement value study by giving background for whether current valuations could be warranted by future performance. The expected speeding up in both earnings and revenue expansion implies the company may be moving into a more positive operational stage, possibly stimulating a re-rating by the market.

Dividend Attractiveness

The company provides a good income part with a maintainable dividend profile that improves its value offer.

• Dividend yield of 3.61%, notably higher than the S&P 500 average of 2.36% • Payout ratio of 36.01% shows maintainable dividend payments • Ten-year dividend payment history showing dependability • Dividend expansion going beyond earnings expansion, although at a moderate 2.47% yearly rate

For value investors, dividends give actual returns while waiting for market acceptance of the basic value. A maintainable and increasing dividend can repay investors during times when the stock price does not show bettering basics.

The mix of lower valuation multiples, acceptable financial condition, adequate profitability, and bettering expansion outlook places Travel + Leisure Co as an interesting option for investors using value-focused plans. The stock seems to provide several paths for possible returns, including valuation multiple widening, earnings expansion, and dividend income.

Find more undervalued stocks with solid fundamentals using our Decent Value screening tool.

Disclaimer: This examination is based on basic data and screening rules for informational reasons only. It does not form investment guidance, and investors should do their own investigation and think about their personal financial situations before making investment choices. Past performance and basic measurements are not assurances of future outcomes.