The search for undervalued companies remains a cornerstone of value investing, a strategy pioneered by Benjamin Graham and later popularized by Warren Buffett. This approach focuses on identifying stocks trading below their intrinsic value, determined through fundamental analysis of financial health, profitability, growth prospects, and valuation metrics. By applying a disciplined screening process, investors aim to uncover opportunities where the market has potentially mispriced a security, offering a margin of safety. One such candidate identified through a "Decent Value" screen, which emphasizes good valuation scores alongside acceptable health, profitability, and growth, is Travel + Leisure Co (NYSE:TNL).

Travel + Leisure Co operates in the hospitality and travel sector, providing vacation ownership services, travel memberships, and exchange platforms. Its business spans two main segments: Vacation Ownership, which develops and markets vacation interests and offers financing and property management, and Travel and Membership, which includes exchange brands and travel technology. The company’s focus on experiential travel positions it in a market with cyclical elements but also long-term demand drivers.

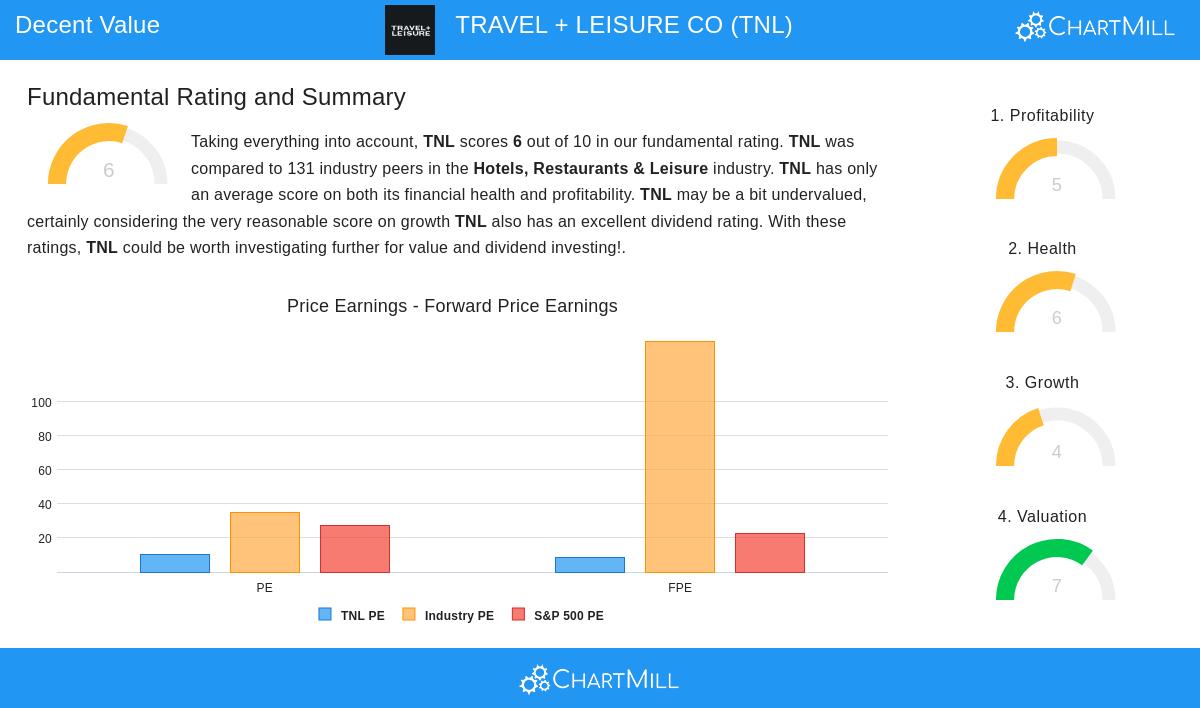

A detailed review of the fundamental analysis report reveals why TNL stands out as a potential value opportunity. The report evaluates the stock across five critical areas, valuation, health, profitability, growth, and dividend, each of which aligns with the principles of value investing.

Valuation TNL scores a solid 7 out of 10 in valuation, indicating it is priced attractively relative to its fundamentals. Key metrics support this: the company’s Price/Earnings (P/E) ratio of 10.28 is not only well below the industry average of 35.18 but also significantly lower than the S&P 500 average of 27.14. Similarly, its forward P/E of 8.64 compares favorably to both industry and broader market benchmarks. The Enterprise Value to EBITDA and Price/Free Cash Flow ratios further reinforce that TNL is trading at a discount to many peers. For value investors, these valuation metrics are crucial, they signal a potential gap between market price and intrinsic value, providing that essential margin of safety Graham emphasized.

Financial Health With a health rating of 6, TNL demonstrates reasonable financial stability. The company has strong liquidity, evidenced by a Current Ratio of 3.71 and a Quick Ratio of 2.70, both ranking in the top tier of its industry. This suggests TNL can comfortably meet short-term obligations, reducing near-term risk. However, solvency metrics present a mixed picture: while the Altman-Z score indicates limited bankruptcy risk, the Debt to Free Cash Flow ratio of 11.31 is elevated, implying a longer debt repayment timeline. Value investors prioritize financial health to ensure the company can withstand economic downturns and avoid value traps, situations where apparent cheapness masks underlying weaknesses.

Profitability TNL’s profitability rating of 5 reflects adequate but not exceptional earnings power. The company maintains a solid Profit Margin of 10.14% and an Operating Margin of 19.84%, outperforming many industry competitors. Return on Invested Capital (ROIC) stands at 10.78%, though the three-year average is slightly below industry norms. These figures indicate efficient operations and an ability to generate returns, which value investors look for to confirm that low valuation isn’t simply a result of poor execution or declining profits.

Growth and Dividend Growth is TNL’s weakest area, with a rating of 4. Historical revenue and EPS growth have been modest, but analysts project improvement: EPS is expected to grow by 12.84% annually, and revenue by 4.10%. This anticipated acceleration, combined with a strong dividend rating of 7, adds appeal. The yield of 3.78% exceeds the industry average, and the payout ratio is sustainable at 37.03% of earnings. For value investors, dividends provide income while waiting for price appreciation, and expected growth helps close the valuation gap over time.

In summary, TNL presents a strong case for value-oriented scrutiny. Its low valuation multiples suggest market undervaluation, while decent health and profitability scores indicate fundamental resilience. The dividend offers income, and projected growth could catalyze a re-rating. Investors using a value strategy often seek such profiles, where quantitative metrics hint at hidden worth, balanced against manageable risks.

For those interested in exploring similar opportunities, further results from the "Decent Value" screen can be found here.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Readers should conduct their own research or consult a financial advisor before making investment decisions.