Tidewater Inc (NYSE:TDW) operates in the offshore marine support sector, providing transportation and support services to the global energy industry through its fleet of about 211 vessels in over 30 countries. The company's activities cover multiple geographic areas including the Americas, Asia Pacific, Middle East, Europe/Mediterranean and West Africa, serving all stages of offshore energy exploration, development, production and maintenance work.

Investment Strategy Context

The selection of Tidewater follows a disciplined value investing approach that looks for companies trading below their intrinsic value while having good fundamental traits. This method, based on the ideas set by Benjamin Graham and later improved by investors like Warren Buffett, stresses buying securities with an adequate margin of safety. The approach concentrates on finding companies with good profitability and financial condition that are still priced cautiously by the market, creating possibility for price increase as the difference between market price and intrinsic value narrows over time.

Valuation Assessment

Tidewater's valuation metrics present a strong case for value-focused investors. The company trades at multiples that indicate market pricing may not completely show its operational strength and future possibility.

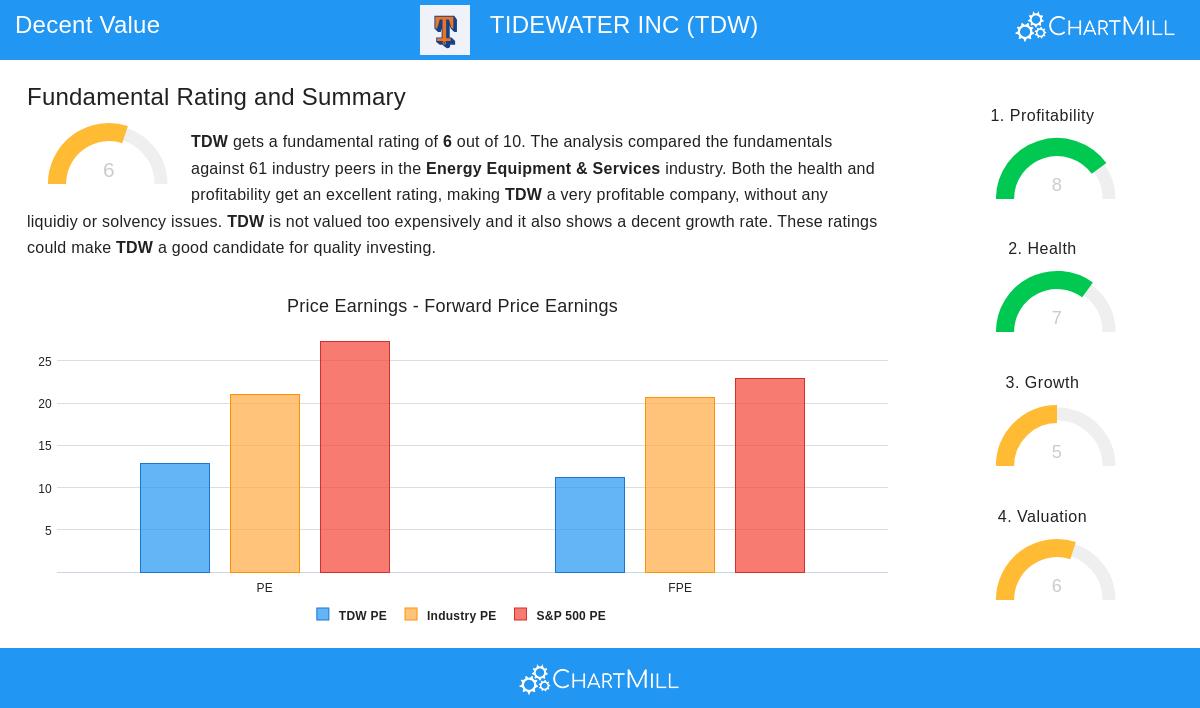

- Price-to-Earnings ratio of 12.86, much lower than the S&P 500 average of 27.34

- Forward P/E ratio of 11.14 compared to the market average of 22.86

- Enterprise Value to EBITDA in line with industry averages

- Good Price-to-Free Cash Flow ratio more inexpensive than 79% of industry peers

These valuation metrics are especially notable given the company's good operational performance. The lower multiples relative to both the wider market and many industry competitors suggest possible undervaluation, a main factor for value investors looking for companies trading below their intrinsic worth.

Financial Health Analysis

Tidewater shows good financial health with a ChartMill Health Rating of 7 out of 10, indicating a stable financial base that can handle economic changes. This part is important for value investors who focus on companies with strong balance sheets to endure possible market declines.

- Current Ratio of 2.11 indicates good short-term liquidity

- Quick Ratio of 2.04 shows ability to meet immediate obligations

- Debt-to-Equity ratio of 0.47 reflects careful leverage

- Debt-to-Free Cash Flow ratio of 2.19 indicates capacity to handle debt

The company's solid liquidity position and workable debt levels provide the financial flexibility needed to manage the cyclical character of the offshore energy sector while keeping operational stability during industry downturns.

Profitability Metrics

Tidewater's operational efficiency is clear in its profitability metrics, receiving a ChartMill Profitability Rating of 8 out of 10. Good profitability is necessary for value investments as it confirms the company's ability to generate returns and supports the case for intrinsic value being higher than market price.

- Return on Assets of 9.59% performs better than 89% of industry peers

- Return on Equity of 17.45% is higher than 84% of competitors

- Profit Margin of 14.62% is in the top quartile of the industry

- Operating Margin of 21.80% shows operational efficiency

These notable profitability metrics suggest Tidewater has competitive strengths in its operations, possibly creating a lasting advantage that supports continued earnings power, a key element in determining long-term intrinsic value.

Growth Trajectory

While value investing usually favors current valuation over fast growth, maintainable growth stays important for long-term value creation. Tidewater displays balanced growth characteristics with a ChartMill Growth Rating of 5 out of 10.

- Earnings Per Share growth of 27.81% over the past year

- Three-year average Revenue growth of 22.57% each year

- Expected EPS growth of 21.89% in coming years

- Modest forward Revenue growth projection of 3.59%

The company's past growth joined with expected earnings expansion suggests possibility for continued value increase, while the moderate revenue growth expectations help keep realistic valuation assumptions.

Investment Considerations

Tidewater presents an interesting case for value investors looking for exposure to the energy services sector. The company's mix of good valuation multiples, strong financial health, notable profitability, and reasonable growth prospects creates a profile that fits well with value investment criteria. The offshore energy sector's cyclical character may add to the lower valuation, possibly creating opportunity for investors with a longer-term view.

The company's global presence and varied service offerings across multiple offshore energy segments provide some protection against regional economic changes, while its focus on both traditional energy and new windfarm development services places it to gain from energy transition trends.

For investors interested in looking into similar opportunities, more screening results using the Decent Value method can be found through this screening link.

,

Disclaimer: This analysis is based on fundamental data and investment method discussion only and should not be considered as investment advice. All investments carry risk, and readers should do their own research and talk with financial advisors before making investment decisions. The offshore energy sector is subject to commodity price volatility and economic cycles that may affect company performance.