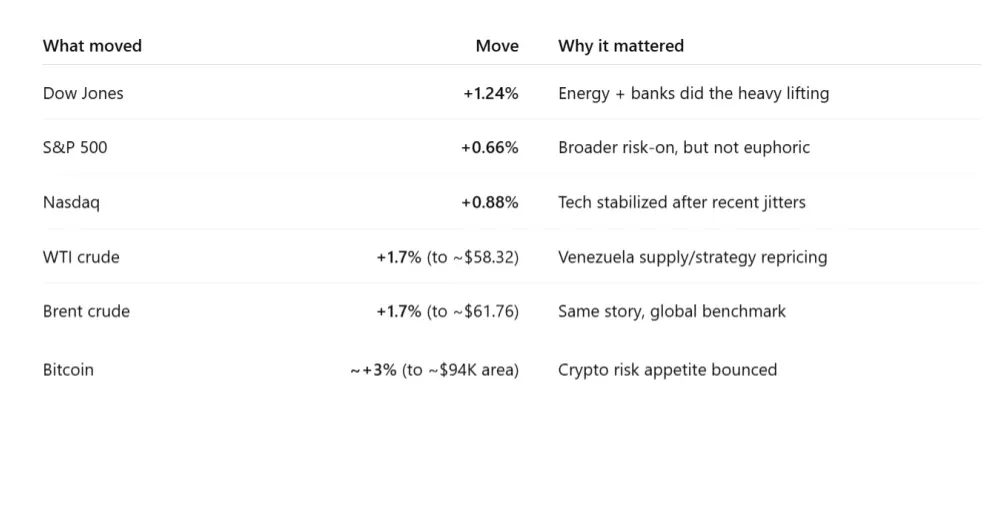

The opening scene: chaos headline, calm market

If you only read the Venezuela headlines, you’d expect risk-off panic. Instead, Wall Street basically shrugged, then hit the gas. The Dow pushed to fresh highs (briefly above 49,000 intraday) and ended up solidly higher, with investors treating the arrest of Venezuela’s leader Nicolás Maduro as a contained event rather than a global contagion.

Venezuela: the “oil optionality” trade is back

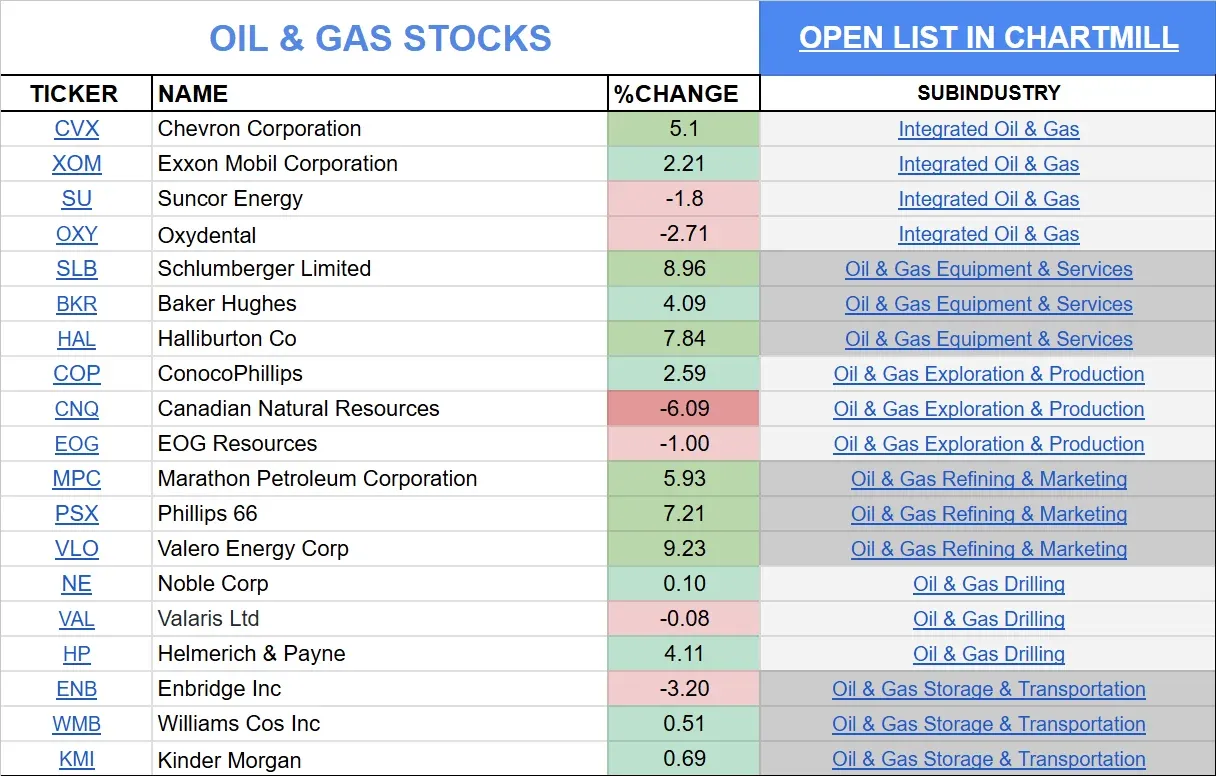

The market’s immediate reaction was simple: if the U.S. is serious about reshaping Venezuela’s oil future, U.S. energy firms (and anyone who fixes pipes) might be first in line.

-

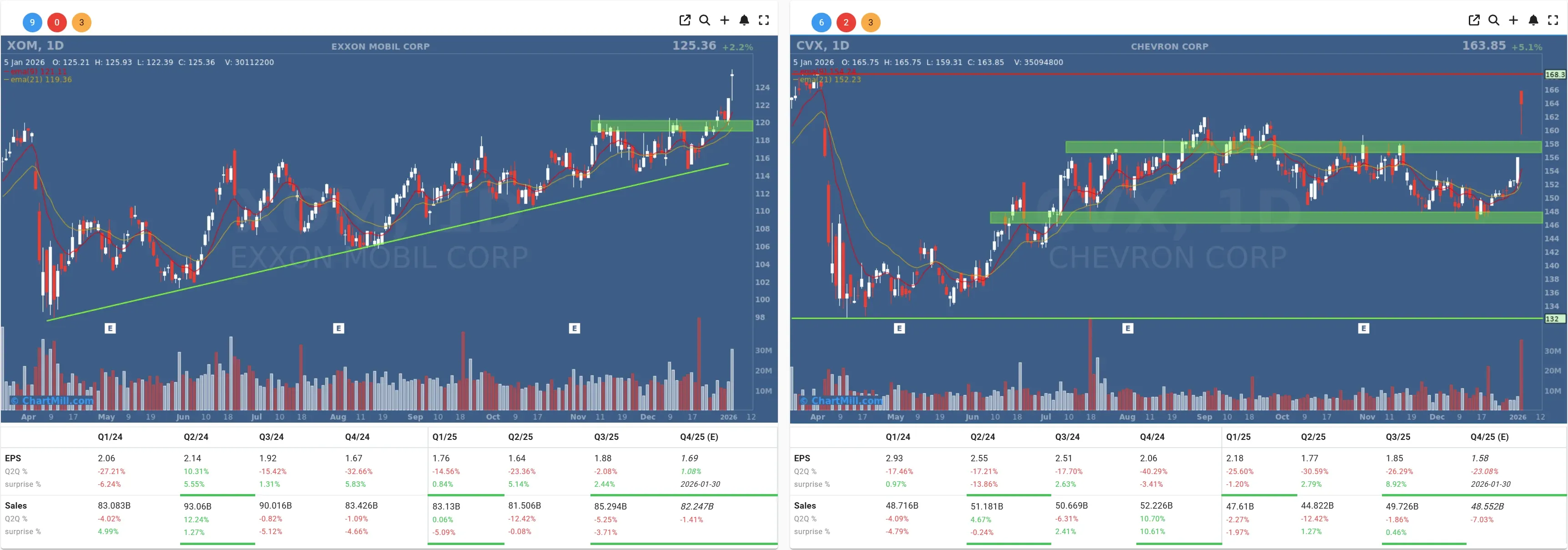

Chevron (CVX | +5.1%) looked like the cleanest way to express the theme, given its history in Venezuela.

-

Exxon Mobil (XOM | +2.21%) rode the same wave.

The real fireworks were in oil services: Halliburton (HAL | +7.84%) and SLB (SLB | +8.96%).

Refiners joined the party too, with Valero Energy (VLO | +9.23%).

Direct link to oil & gas stocks in ChartMill

Defense caught a bid as well? because when geopolitics gets louder, defense usually doesn’t whisper:

- General Dynamics (GD | +3.54%) and Lockheed Martin (LMT | +2.92%).

Direct link to defense contractor stocks in ChartMill

My takeaway: this is less “Venezuela is fixed” and more “the market just repriced the option value.” Rebuilding a heavy-oil system with aging infrastructure is not a weekend DIY project.

Banks drove the Dow? because they love a clean risk-on day

While energy grabbed headlines, financials did a lot of the actual index work. Big-cap banks and payments names marched higher:

-

Goldman Sachs (GS | +3.73%)

-

JPMorgan Chase (JPM | +2.63%)

-

American Express (AXP | +1.9%)

-

Visa (V | +2.11%)

This felt like classic early-year positioning: investors leaning into liquid bellwethers when the tape is green and the narrative is “contained risk.”

Crypto and high-beta: the fun stuff woke up

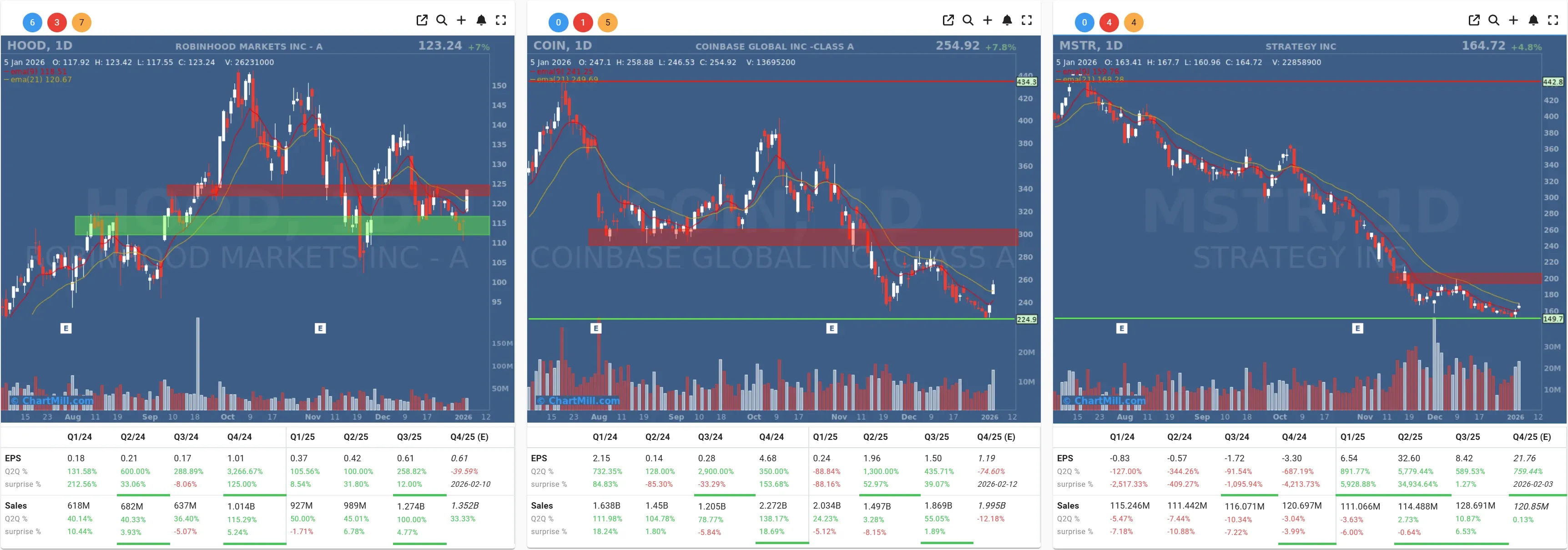

Bitcoin’s bounce pulled the usual crew with it:

-

Coinbase (COIN | +7.77%) jumped after a bullish call from Goldman, with “tokenization” and prediction markets getting airtime again.

-

Robinhood (HOOD | +6.97%) moved in sympathy.

-

Strategy (MSTR | +4.81%) rose even as the company continues to live and die by bitcoin mark-to-market math.

In megacap/AI land, it was more of a pause than a party:

-

Tesla (TSLA | +3.1%) bounced after recent delivery-related pressure.

-

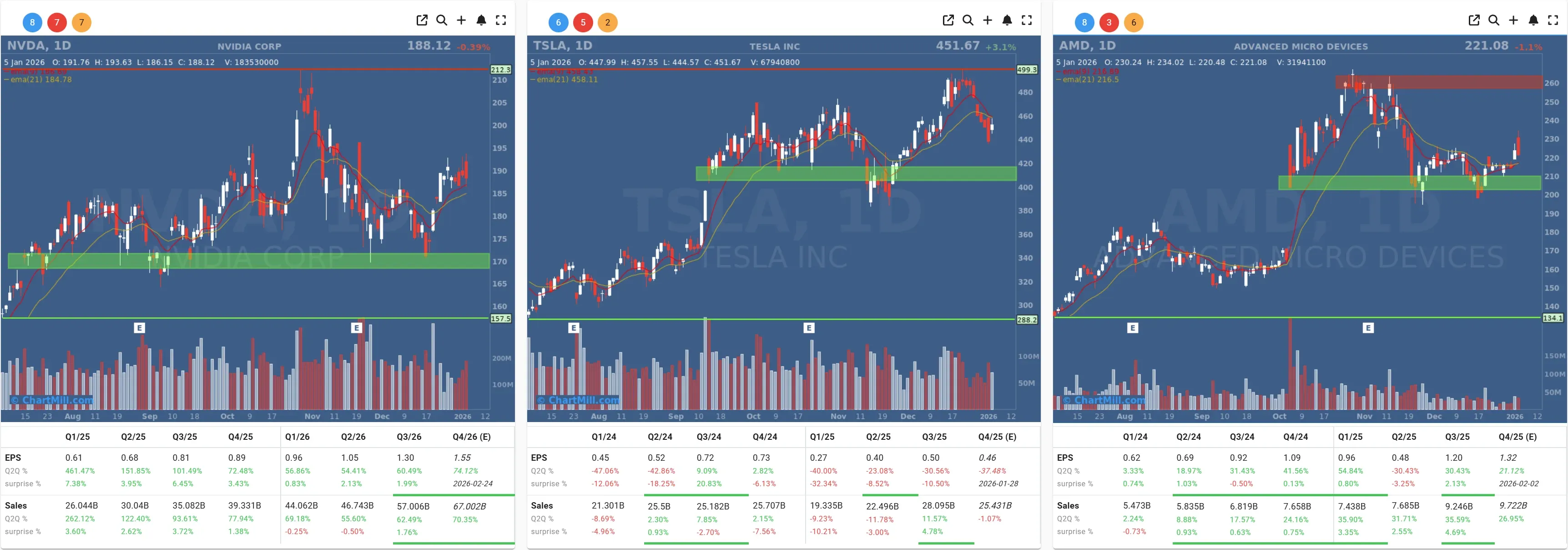

Advanced Micro Devices (AMD | -1.07%) and Nvidia (NVDA | -0.39%) didn’t join the celebration.

Macro reality check: manufacturing still looks tired

Under the surface, the data kept hinting that the economy isn’t exactly doing victory laps.

-

The ISM Manufacturing PMI for December came in at 47.9, down from 48.2—deeper in contraction territory.

-

S&P Global’s manufacturing PMI was 51.8 (still expansion), but down from 52.2.

One more company note: Novo’s pill moment

Healthcare also had a headline mover: Novo Nordisk (NVO | +5.85%) rose after launching an oral version of Wegovy in the U.S., with a reported starter price of $149/month for self-pay customers.

What I’m watching next

Markets now pivot from geopolitics to the usual heavyweight catalysts:

-

U.S. labor-market data (the week’s main macro event)

-

Services PMIs (after manufacturing showed mixed signals)

If risk stays bid, the “early January tailwind” narrative holds. If the data disappoints, Monday may end up looking like a headline-driven sugar rush.

Kristoff - ChartMill

Next to read: Breadth Kicks Off 2026 With a Strong Participation Rebound