QIFU TECHNOLOGY INC (NASDAQ:QFIN) stands out as a compelling pick for investors seeking growth at a reasonable price (GARP). The company, a Chinese credit technology services provider, meets key criteria from Peter Lynch’s investment strategy, combining solid growth, strong profitability, and an attractive valuation.

Why QFIN Fits the GARP Approach

- Sustainable Growth: QFIN has delivered a 5-year average EPS growth of 19.96%, aligning with Lynch’s preference for steady but not excessive expansion.

- Attractive Valuation: With a PEG ratio of 0.32 (well below the preferred threshold of 1), the stock appears undervalued relative to its growth prospects.

- Strong Profitability: The company boasts a 29.92% Return on Equity (ROE), significantly above the 15% minimum Lynch recommends.

- Healthy Balance Sheet: A Debt/Equity ratio of 0.27 and a Current Ratio of 3.08 reflect financial stability and liquidity strength.

Fundamental Strengths

QFIN’s fundamental analysis highlights several positives:

- High Margins: Operating margins of 45.98% and profit margins of 38.98% rank among the best in the Consumer Finance industry.

- Efficient Capital Use: A 16.09% Return on Invested Capital (ROIC) indicates effective allocation of resources.

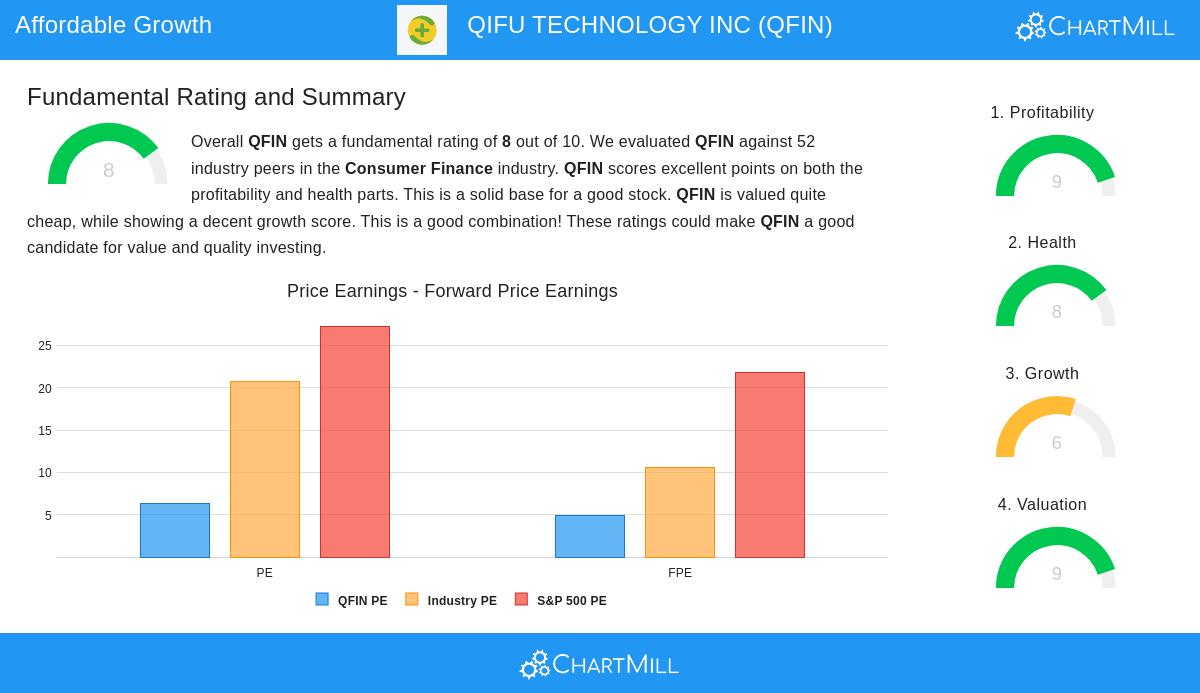

- Undervalued Metrics: A P/E of 6.29 and Forward P/E of 4.87 suggest the stock is priced below industry and S&P 500 averages.

For a deeper dive, review the full fundamental analysis report.

Our Peter Lynch Strategy screener lists more stocks matching these criteria and is updated regularly.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should conduct your own research before making investment decisions.