The investment philosophy of legendary fund manager Peter Lynch has long been a foundation for investors aiming to build lasting, long-term wealth. Central to his method is the idea of Growth at a Reasonable Price (GARP), which concentrates on finding companies with solid, persistent earnings growth that are not priced too high by the market. Lynch supported a systematic, fundamental screening process to locate these chances, searching for businesses with high profitability, sound financial condition, and a stock price that is fair relative to future potential. A filter built on his main ideas can act as a beginning for more study into possible long-term investments.

One company that recently appeared from this filter is QFIN Holdings Inc-ADR (NASDAQ:QFIN), a Shanghai-based credit technology service provider. The company runs a platform that links borrowers with financial institutions and provides a group of technology-based services, such as intelligent marketing and risk management software. For investors following Lynch's ideas, QFIN displays an interesting profile that deserves more examination.

Alignment with Core Lynch Criteria

Peter Lynch stressed that persistent growth, not fast but erratic growth, is essential. He also maintained that even the finest growing company must be bought at a fair price. The screening measures taken from his strategy give a numerical structure to find candidates, and QFIN's numbers match these rules closely.

- Sustainable Earnings Growth: Lynch favored companies with an established history of earnings per share (EPS) growth between 15% and 30% each year, considering this range maintainable. QFIN's five-year average EPS growth rate of 19.96% fits well within this preferred zone, showing a history of solid but controlled increase.

- Reasonable Valuation (The PEG Ratio): Possibly the most well-known Lynch measure is the Price/Earnings to Growth (PEG) ratio, which tries to price a stock in relation to its earnings growth. A PEG ratio of 1 or lower implies the market might be pricing the growth too low. QFIN's PEG ratio, calculated from its past five-year growth, is very low at about 0.13. This shows the stock is trading at a large markdown to its historical growth rate, a main sign for value-aware growth investors.

- Strong Profitability (Return on Equity): Lynch searched for companies that effectively produce profits from shareholder equity. A high Return on Equity (ROE) is a sign of a good business. QFIN's ROE of 30.15% is excellent, not only exceeding Lynch's proposed 15% level but also placing it with the best in its field.

- Financial Health and Stability: To steer clear of poor value and confirm strength, Lynch gave importance to companies with firm balance sheets. His filters involved a Debt/Equity ratio under 0.6 (ideally under 0.25) and a Current Ratio above 1 to make sure short-term debts can be paid.

- QFIN's Debt/Equity ratio of 0.26 shows a careful capital structure leaning heavily toward equity, matching exactly with Lynch's stricter preference.

- The company's Current Ratio of 3.48 shows strong liquidity, indicating it has more than sufficient current assets to pay its current debts many times.

Fundamental Health Check: A High-Level Summary

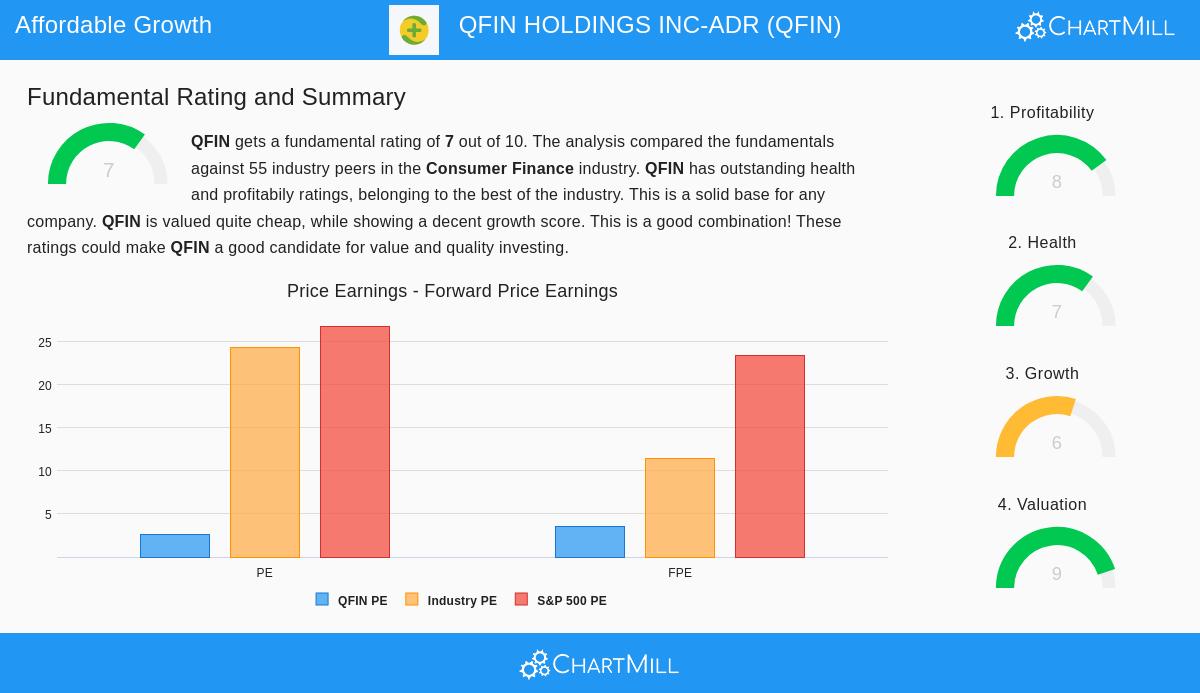

A wider look at QFIN's fundamental condition supports the image shown by the Lynch filter. The company gets high scores for both profitability and health. Its profit margins are with the best in the consumer finance field, and its balance sheet is strong with high liquidity and low debt compared to cash flow. From a valuation viewpoint, the stock seems inexpensive using several measures, including standard P/E and forward P/E ratios, particularly when measured against both industry competitors and the wider S&P 500.

The primary area for thought for a long-term investor, as noted in the growth study, is the forecast of a reduction in earnings growth. While past results have been good, future EPS growth estimates are low. This points to the significance of Lynch's rule of knowing the business—an investor must study whether this slowdown is temporary, due to market fullness, or a planned change, and judge if the current very low price properly accounts for this different expectation. A complete listing of these positives and points to think about is available in the full fundamental analysis report.

Is QFIN a Lynch-Style Opportunity?

For an investor using a GARP method influenced by Peter Lynch, QFIN Holdings offers a standard example. It shows the characteristics Lynch prized: a history of good, maintainable earnings growth, excellent profitability, and a very strong balance sheet. Most significantly, it is priced at a level—shown by its very small PEG ratio—that suggests the market is not currently valuing that quality and growth. This mix of elements makes it a leading candidate for more detailed investigation.

The following action, as Lynch would suggest, is to go past the statistics. This requires studying the company's business model, its competitive strengths in the Chinese fintech industry, the regulatory setting, and management's plan for addressing the expected growth reduction. The numerical filter finds the chance; the non-numerical research decides its role in a long-term portfolio.

Interested in examining other companies that match the Peter Lynch investment pattern? You can execute the filter yourself and view the present outcomes here.

Disclaimer: This article is for informational and educational reasons only and does not form financial advice, a suggestion, or an offer to buy or sell any securities. The study is based on data and a preset screening method; it is not a replacement for your own complete research. Investing in stocks includes risk, including the possible loss of principal. You should think about your own financial position, investment goals, and risk tolerance before making any investment choice.