In long-term investing, few strategies have earned as much respect and practical success as the approach promoted by Peter Lynch. His methodology, detailed in One Up on Wall Street, highlights identifying companies with solid growth potential that are trading at sensible valuations, a philosophy often called Growth at a Reasonable Price (GARP). Lynch’s framework avoids speculative market timing and instead concentrates on fundamental health, sustainable profitability, and understandable business models. Investors using this strategy look for firms that are not only growing but doing so in a financially prudent way, with manageable debt, solid returns on equity, and appealing valuations relative to their growth paths.

QUALCOMM INC (NASDAQ:QCOM) appears as a noteworthy candidate when measured against Lynch’s standards. The company, a frontrunner in developing essential technologies for mobile devices and wireless products, functions in a sector that is central to modern connectivity and innovation. Its business segments, Qualcomm CDMA Technologies (QCT), Qualcomm Technology Licensing (QTL), and Qualcomm Strategic Initiatives, use wide intellectual property and advanced semiconductor design, placing it at the lead of 5G, IoT, and automotive progress. This operational clarity and industry importance fit well with Lynch’s preference for investing in what you understand: businesses with concrete products and services that have lasting demand.

When using Lynch’s specific investment rules, QUALCOMM shows solid alignment across several important metrics:

- Earnings Per Share (EPS) Growth: Lynch preferred companies with EPS growth between 15% and 30% over five years to confirm sustainability. QUALCOMM’s EPS has increased at a notable average of 23.53% yearly over this time, indicating solid profitability growth without passing the upper limit that might indicate unsustainable rapid expansion.

- PEG Ratio: This measure, which modifies the price-to-earnings ratio for growth, is key to Lynch’s valuation test. A PEG ratio under 1 implies a stock may be undervalued relative to its growth outlook. QUALCOMM’s PEG ratio of about 0.58 is well below this mark, emphasizing a possibly appealing valuation when growth is considered.

- Debt-to-Equity Ratio: Financial strength is critical in Lynch’s strategy, with a liking for low debt. QUALCOMM’s debt-to-equity ratio of 0.54, while a bit above Lynch’s perfect of under 0.25, stays below the screen’s limit of 0.6 and shows a measured use of leverage, backed by strong cash flows and profitability.

- Current Ratio: Liquidity is evaluated through this gauge, with a value over 1 showing good short-term financial strength. QUALCOMM’s current ratio of 3.19 greatly exceeds this need, indicating a firm capacity to meet obligations without difficulty.

- Return on Equity (ROE): Lynch searched for ROE above 15% as a signal of efficient capital use and high profitability. QUALCOMM’s ROE of 42.55% is outstanding, not only meeting but far exceeding this standard, reflecting excellent management effectiveness and earnings strength.

These metrics together describe a company that is increasing earnings at a good rate, keeps prudent financial health, and is valued in a way that does not exaggerate its future possibilities. This mix is precisely what Lynch wanted: a business that can build value over time without depending on extreme optimism or debt.

Outside the screen-specific standards, QUALCOMM displays other positives that match Lynch’s wider investment thinking. The company has a moderate dividend yield of 2.21%, with a record of steady payments and raises, attractive to investors who appreciate income together with growth. Its fundamental health is further supported by high marks in profitability and solvency measures, such as return on invested capital (ROIC) of 20.40% and an Altman-Z score suggesting low bankruptcy risk. Lynch frequently highlighted the significance of insider confidence and shareholder-friendly behavior; QUALCOMM’s share buyback program and steady insider activity fit with these points, though they are not directly needed in the basic screen.

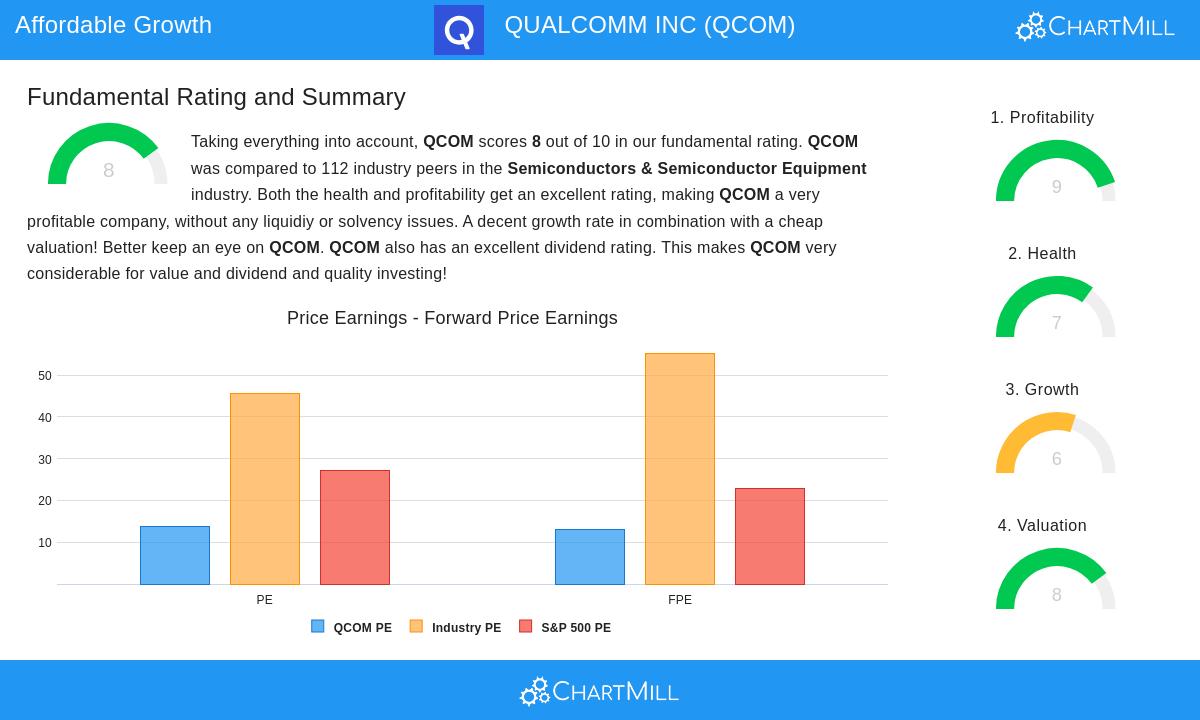

A high-level summary of QUALCOMM’s fundamental report supports this favorable view. The report gives QUALCOMM a solid rating of 8 out of 10, noting superb profitability and health scores, with good growth and appealing valuation. Specifically, it mentions exceptional margins, high returns on equity and assets, and a dividend policy that is both maintainable and increasing. The valuation review indicates the stock is less expensive than most industry peers based on multiples like P/E and EV/EBITDA, while the growth part points to firm historical performance, even with some anticipated slowing in future expansion, a typical feature in established yet forward-thinking firms.

For investors wanting to examine other companies that satisfy Peter Lynch’s standards, more screening results can be found using this dedicated stock screener link. This tool enables more customization and finding of possible investments matching a disciplined, fundamental method.

In summary, QUALCOMM stands as a significant example of a stock that fits with Peter Lynch’s ideas of finding growth at a sensible price. Its solid historical performance, financial steadiness, and sensible valuation form a noteworthy case for long-term investors looking for quality compounding chances. Still, as with any investment, complete due diligence and thought of personal financial aims and risk tolerance are necessary.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Readers should conduct their own research or consult a financial advisor before making investment decisions.