In the search for long-term investment opportunities, many investors turn to strategies that balance growth potential with reasonable valuations. One such approach is the GARP (Growth at a Reasonable Price) methodology, which shares significant overlap with the principles famously used by Peter Lynch during his time at the Magellan Fund. Lynch’s strategy focuses on finding companies with strong, sustainable earnings growth that are not overvalued by the market, emphasizing financial health and profitability. This method avoids speculative high-flyers in favor of businesses that can deliver consistent returns over many years. A recent screen based on these Lynch principles has identified QUALCOMM INC (NASDAQ:QCOM) as a candidate for more research for investors with a long-term view.

Meeting the Lynch Criteria

QUALCOMM’s fundamental profile matches the key filters of a Peter Lynch-inspired screen. The strategy looks for companies growing earnings at a sustainable pace, trading at a valuation that compensates for that growth, and keeping a strong financial foundation. QUALCOMM meets these criteria on several important points.

- Sustainable Earnings Growth: A key part of the Lynch approach is a 5-year earnings per share (EPS) growth rate between 15% and 30%. Growth above 30% is often seen as unsustainable. QUALCOMM’s EPS has grown at an average of 23.53% each year over the past five years, placing it within this target range and indicating a strong, yet manageable, growth path.

- Reasonable Valuation via PEG Ratio: Lynch used the PEG ratio (Price/Earnings to Growth) to find stocks that are fairly priced relative to their growth rate. A PEG ratio at or below 1.0 is usually seen as attractive. QUALCOMM’s PEG ratio, based on its past five years of growth, is about 0.62, suggesting the market may be undervaluing its growth prospects.

- Strong Profitability: The screen requires a Return on Equity (ROE) above 15% to ensure the company is efficiently generating profits from shareholder equity. QUALCOMM far exceeds this, with an ROE of 42.55%, signaling high profitability.

- Solid Financial Health: To avoid over-leveraged companies, the strategy requires a Debt-to-Equity ratio below 0.6. QUALCOMM’s ratio of 0.54 indicates a balanced approach to financing. Also, its Current Ratio of 3.19 shows more than enough liquidity to cover short-term obligations, exceeding the required level of 1.0.

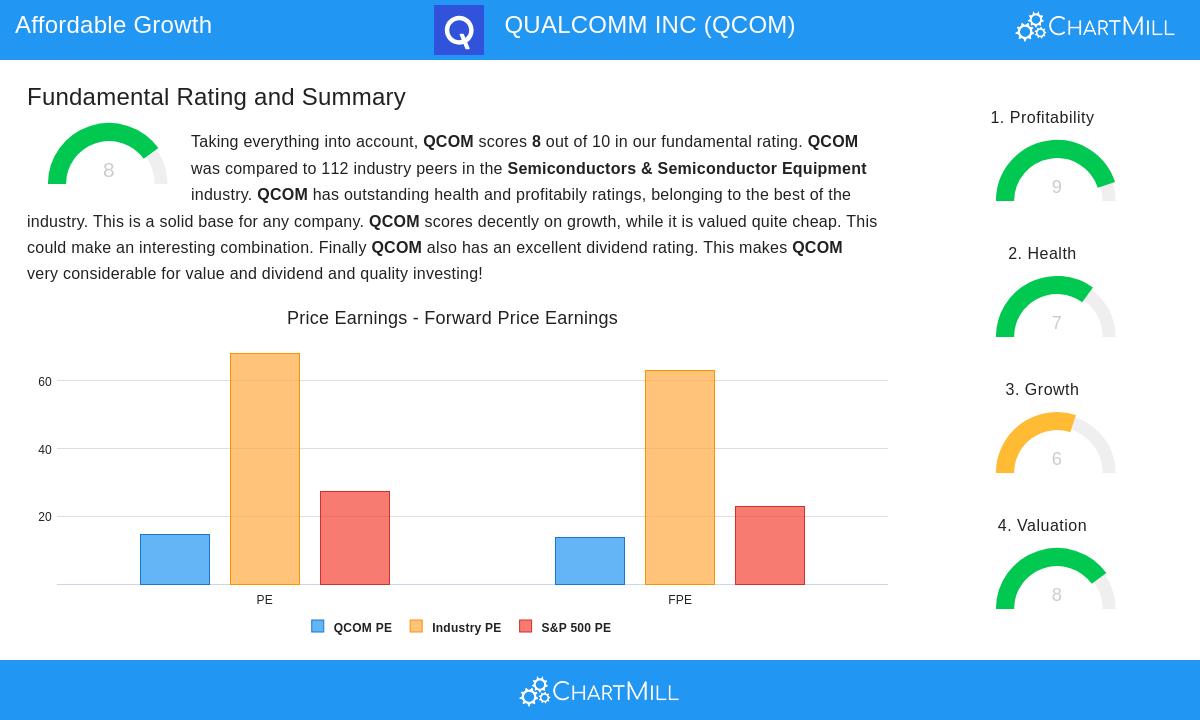

Fundamental Report Summary

A closer look at QUALCOMM’s fundamental analysis shows a company in good health. The full report gives QUALCOMM a high overall score of 8 out of 10, reflecting good performance across profitability, financial health, and valuation. The company’s margins are some of the best in its industry, and it shows high returns on both equity and invested capital. From a valuation point of view, its price-to-earnings ratios are appealing compared to both the wider S&P 500 and its industry peers. While future growth estimates are more moderate than its historical performance, the company’s strong financial position and profitability provide a good foundation. For a detailed view, you can see the full fundamental analysis report.

Investment Thesis for GARP Investors

For investors seeking growth at a reasonable price, QUALCOMM presents a strong case. The company is a key player in the wireless technology sector, with its semiconductors and licensing intellectual property being important to mobile devices and the growing Internet of Things (IoT) market. This places it in a "understandable" industry, another Lynch preference. The mix of its strong historical growth, high profitability, reasonable debt level, and appealing valuation metrics creates a profile that fits well with a long-term, patient investment strategy. It is not a speculative bet but an established company trading at a price that seems to discount its future potential.

The Peter Lynch screen is a useful starting point for finding companies that deserve more research. QUALCOMM is one of a number of stocks that currently pass this strict set of criteria. Investors interested in seeing other companies that fit this profile can find the full, current list of results by visiting the Peter Lynch Strategy stock screener.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions.