Investors looking for growth chances at fair prices often use screening methods that find companies showing good expansion potential without high valuations. The "Affordable Growth" method focuses on stocks with strong growth traits, good profitability, and sound finances while steering clear of overpriced cases. This system balances the search for expansion with price awareness, trying to find companies set for continued results without paying high multiples.

PTC INC (NASDAQ:PTC) appears as a choice matching this investment method, getting an overall fundamental score of 6 out of 10 based on ChartMill's detailed study. The Boston software company focuses on digital answers for engineering, making, and service of physical goods, with products covering computer-aided design, product lifecycle management, and industrial IoT systems.

Growth Path

PTC shows good growth traits that match the affordable growth method's focus on expansion potential. The company's past results display notable speed, while future estimates point to continued growth at acceptable levels.

- Earnings Per Share grew 27.79% over the past year with an average yearly growth rate of 23.66% over recent years

- Revenue went up 11.42% in the last year, keeping a good 12.85% average yearly growth rate in the past

- Forward estimates predict 14.34% EPS growth and 10.49% revenue growth each year

This steady growth picture across both past and estimated numbers meets the screening need for good expansion potential while keeping steadiness in growth rates, lowering the instability often linked with high-growth investments.

Valuation Review

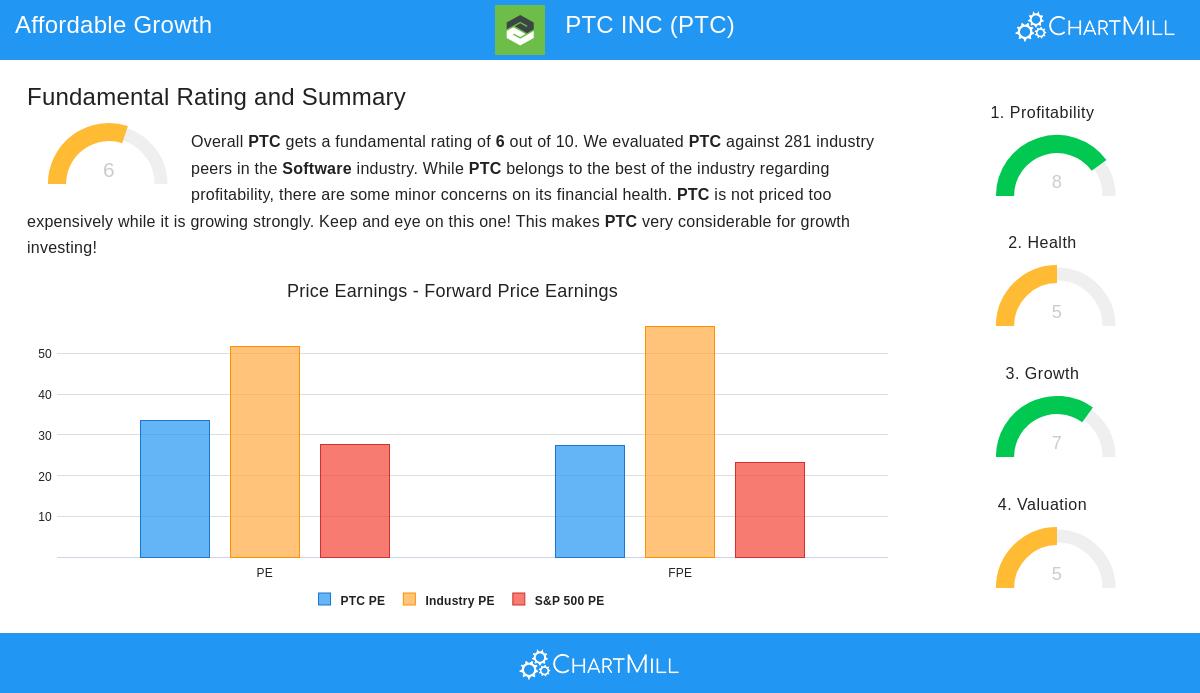

The valuation study shows why PTC fits as "affordable" within the growth setting. While some standard measures seem high, several reasons support the current price relative to growth outlooks.

- P/E ratio of 33.58 looks costly next to the S&P 500 average of 27.67

- Forward P/E of 27.45 matches more closely with market averages

- Enterprise Value to EBITDA and Price/Free Cash Flow ratios are lower priced than 74% and 74% of industry friends respectively

- Low PEG ratio shows acceptable valuation when including growth expectations

The valuation view becomes more interesting when thinking about PTC's growth payback. The company's good profitability and expected earnings growth of over 17% help explain current multiples, creating the valuation-growth balance that affordable growth methods look for.

Profitability Quality

PTC's very good profitability measures give basic support for its growth story and valuation reasoning. The company shows effectiveness in changing revenue to profits across several checks.

- Return on Assets of 8.23% does better than 82% of software industry friends

- Return on Equity of 14.60% and Return on Invested Capital of 11.54% are higher than 83% and 88% of rivals respectively

- Operating Margin of 30.32% sits in the top group of the industry

- Profit Margin of 20.74% and Gross Margin of 82.16% are much better than industry averages

These profitability measures not only show operational quality but also give the money base to maintain growth plans, a key part for affordable growth investing where companies must pay for expansion through operational strength instead of high borrowing.

Financial Soundness Points

While PTC's growth and profitability scores are good, the financial soundness rating of 5 out of 10 brings up some points for investors. The company shows mixed signs across solvency and liquidity checks.

- Good solvency signs with Altman-Z score of 6.55 and Debt to FCF ratio of 1.46 years

- Medium debt levels with Debt/Equity ratio of 0.34 showing limited need for loans

- Liquidity questions with Current and Quick ratios of 0.89, below industry averages

The soundness check points out that while PTC keeps acceptable solvency and workable debt, the lower liquidity ratios need watching. However, given the company's good cash flow creation and profitability, these liquidity measures may be less worrying within the setting of its business model and industry place.

Investment Points

PTC presents an interesting case for affordable growth investors looking for exposure to the software field. The company's good growth path, very good profitability, and acceptable valuation relative to growth outlooks create an appealing picture for this method. The balance between these parts is important—while pure growth investors might follow faster expansion and value investors might look for lower-priced multiples, PTC gives a middle area with maintainable growth at explainable valuations.

The company's place in industrial software and digital change answers gives exposure to long-term lasting trends, while its mixed delivery model (on-premises, cloud, or mixed) gives flexibility in adjusting to market needs. These operational strengths support the financial traits that make PTC fitting for affordable growth methods.

For investors wanting to look into similar chances, more affordable growth choices can be found through this screening tool that uses similar rules across the market.

Disclaimer: This study is based on fundamental data and scores given by ChartMill and shows an objective check of the company's financial measures. It is not investment advice and should not be seen as a suggestion to buy or sell any security. Investors should do their own research and think about their personal money situation before making investment choices.