Growth investing typically focuses on companies with notable revenue and earnings increases, though prices can sometimes rise too high. The "Affordable Growth" method looks for stocks that offer both growth opportunities and fair prices, backed by good profitability and financial stability. This method helps investors avoid paying too much for growth while still targeting companies with significant potential.

PINTEREST INC-CLASS A (NYSE:PINS) matches this approach, as seen in its fundamental analysis. Here’s how it meets the Affordable Growth standards:

Growth: A Major Factor

Pinterest shows strong growth, receiving a ChartMill Growth Rating of 8/10. Key points include:

- Revenue Growth: The company’s revenue rose by 17% compared to the previous year, with a 5-year average annual growth rate of 26.1%, well above many competitors in the Interactive Media & Services sector.

- Earnings Growth: EPS grew by 16.9% over the past year, with an expected future growth rate of 15.4%, showing continued progress.

- Positive Trends: Analysts predict better EPS growth compared to past results, indicating improved operational efficiency.

For Affordable Growth investors, these numbers matter—steady growth in revenue and earnings supports investment, as long as prices stay reasonable.

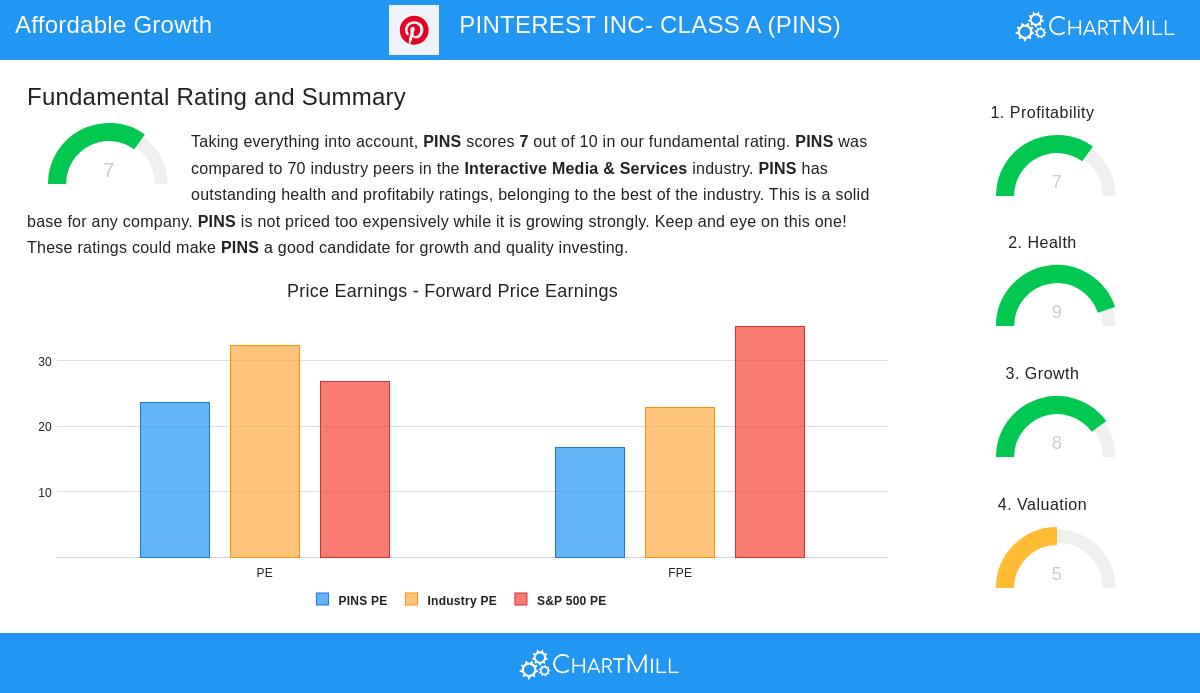

Valuation: Fair Pricing for Growth

Despite its growth, Pinterest’s valuation remains moderate (ChartMill Valuation Rating: 5/10), avoiding the high premiums seen in some fast-growing stocks:

- P/E Ratio: At 23.5, Pinterest trades below the industry average (32.3) and the S&P 500’s 26.8. Its forward P/E of 16.7 is even more appealing, priced lower than both the market and sector.

- Price/FCF: The stock’s price-to-free-cash-flow ratio is better than 67% of industry peers, showing efficient cash generation relative to its share price.

- PEG Ratio: When factoring in expected earnings growth, Pinterest’s valuation seems balanced, lowering the risk of overpaying.

This mix of growth and fair pricing is key to the Affordable Growth strategy, as it limits downside risk while keeping room for gains.

Profitability and Financial Health: Key Strengths

While growth and valuation are primary factors, Pinterest’s profitability (7/10) and financial health (9/10) add to its appeal:

- Strong Margins: A 49.3% net profit margin places it in the top 3% of its industry, while an 80% gross margin highlights strong pricing control.

- No Debt: The company has no debt, with a current ratio of 8.8, showing plenty of liquidity to support operations and growth plans.

- ROE/ROA: Returns on equity (40%) and assets (35.6%) lead the industry, reflecting smart use of capital.

These metrics lower fundamental risk, ensuring the company can maintain growth without excessive borrowing—an important factor for Affordable Growth investors.

Conclusion

Pinterest’s mix of strong growth, fair pricing, and solid financials makes it a strong choice for investors looking for growth at a reasonable price. The stock’s fundamentals fit well with the Affordable Growth strategy, offering a balanced risk-reward outlook.

For more stocks that fit similar criteria, check out the Affordable Growth Screen.

Disclaimer: This analysis is not investment advice. Investors should do their own research or consult a financial advisor before making decisions.