For investors aiming to build a portfolio focused on generating passive income, a disciplined screening process is important. One useful strategy involves identifying companies that not only offer an attractive dividend today but also possess the fundamental financial capacity to maintain and possibly increase those payments over time. This approach gives priority to stocks with high dividend ratings, which assess yield, growth, and sustainability, while also ensuring a foundation of acceptable profitability and financial condition to reduce risk. This method helps filter out companies where a high yield might be misleading, caused by a falling share price due to operational problems.

Murphy Oil Corp (NYSE:MUR) appears as a candidate worth examining through this perspective. The independent oil and gas exploration and production company, with operations mainly in the U.S. and Canada, presents a profile that matches the central principles of a careful dividend-investing strategy.

Dividend Appeal

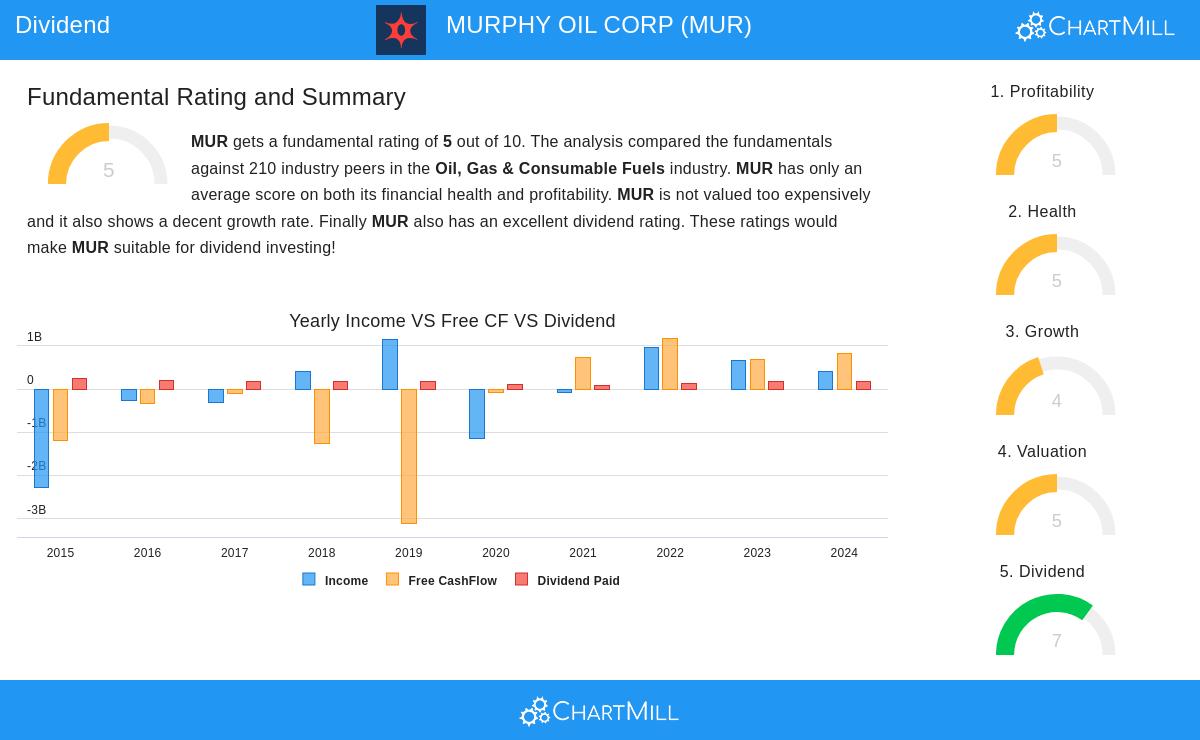

The main attraction for an income-focused investor is, without question, the dividend itself. Murphy Oil is notable with a yearly dividend yield of 4.81%, which is more than double the current average yield of the S&P 500. This offers a significant immediate income stream. Furthermore, the company has a dependable history, having paid dividends for at least ten years without a decrease in the last three years, and showing a small annual growth rate of 3.72%. This history of steady payments is an important factor for the strategy, as it shows a corporate dedication to returning capital to shareholders.

- Attractive Yield: 4.81% (vs. S&P 500 average of ~2.38%)

- Proven Track Record: Over 10 years of dividend payments.

- Modest Growth: A 5-year annualized dividend growth rate of 3.72%.

Sustainability and Fundamental Condition

A high yield is only useful if it is sustainable, which is why the screening criteria require acceptable profitability and financial condition. Murphy Oil’s fundamental report shows a varied but generally acceptable picture in these areas, which supports the dividend story. The company is profitable, with positive earnings and cash flow from operations over the past year. Its gross margin of nearly 69% is strong compared to industry peers, indicating efficient operations.

Financially, the company displays solvency capacity with a manageable debt-to-equity ratio of 0.28, performing better than a majority of its industry competitors. However, investors should note a point of consideration in its liquidity, as shown by current and quick ratios below 1.0, suggesting possible difficulties in meeting short-term obligations without depending on future cash flows. This is a key area for observation but is offset by the good solvency metrics. This mix of acceptable profitability and satisfactory condition is exactly what the screening method aims to confirm the dividend is not being paid from an unstable financial situation.

- Profitability Metrics:

- Positive earnings and operating cash flow (TTM).

- Gross Margin: 68.91% (performs better than 78% of industry peers).

- Financial Health Highlights:

- Debt-to-Equity Ratio: 0.28 (good, performs better than 64% of peers).

- Point of Caution: Lower liquidity ratios (Current Ratio: 0.84).

Valuation and Growth Context

From a valuation viewpoint, Murphy Oil seems fairly priced. Its price-to-earnings ratio of 15.18 is a discount to the broader S&P 500 and is consistent with its industry average. Looking ahead, analysts project earnings per share to increase at a good rate of about 13.60% annually. This expected growth is important as it provides a way for future dividend increases, making the current payout more sustainable. If the company can achieve this growth while keeping its financial discipline, it could support both capital appreciation and continued income growth for investors.

For a detailed breakdown of all these factors, you can review the complete fundamental analysis report for Murphy Oil.

Conclusion

Murphy Oil Corp represents an interesting case study for the "high dividend rating with acceptable fundamentals" screening strategy. It offers a high yield supported by a long history of payments, all while operating from a base of reasonable profitability and a generally sound balance sheet, especially concerning its long-term debt structure. While the liquidity position requires attention, the overall profile indicates a company able to maintain its dividend. For investors building an income-generating portfolio, MUR meets many of the important criteria, combining immediate yield with the possibility for consistent, long-term income growth.

This analysis of Murphy Oil was obtained from a systematic screen for good dividend payers. If you are interested in finding other companies that meet similar criteria, you can run the "Best Dividend Stocks" screen yourself to see the full list of results.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation to buy, sell, or hold any security, or an endorsement of any investment strategy. All investments involve risk, including the possible loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.