MICRON TECHNOLOGY INC (NASDAQ:MU): A Prime Candidate for Value Investors

By Mill Chart

Last update: Sep 1, 2025

In value investing, finding companies trading below their intrinsic value while having good fundamentals is a key strategy. This method, started by Benjamin Graham and developed further by investors such as Warren Buffett, aims to find chances where the market might have incorrectly priced a security, providing a safety buffer for investors focused on the long term. One way to simplify this hunt is to use set screens that sort for stocks with good valuation numbers combined with acceptable health, profitability, and growth. These factors are important for lowering risk while taking advantage of possible price increases. MICRON TECHNOLOGY INC (NASDAQ:MU) appears as a candidate from this type of screening process, deserving a more detailed examination for those curious about value-focused chances.

Valuation Strengths

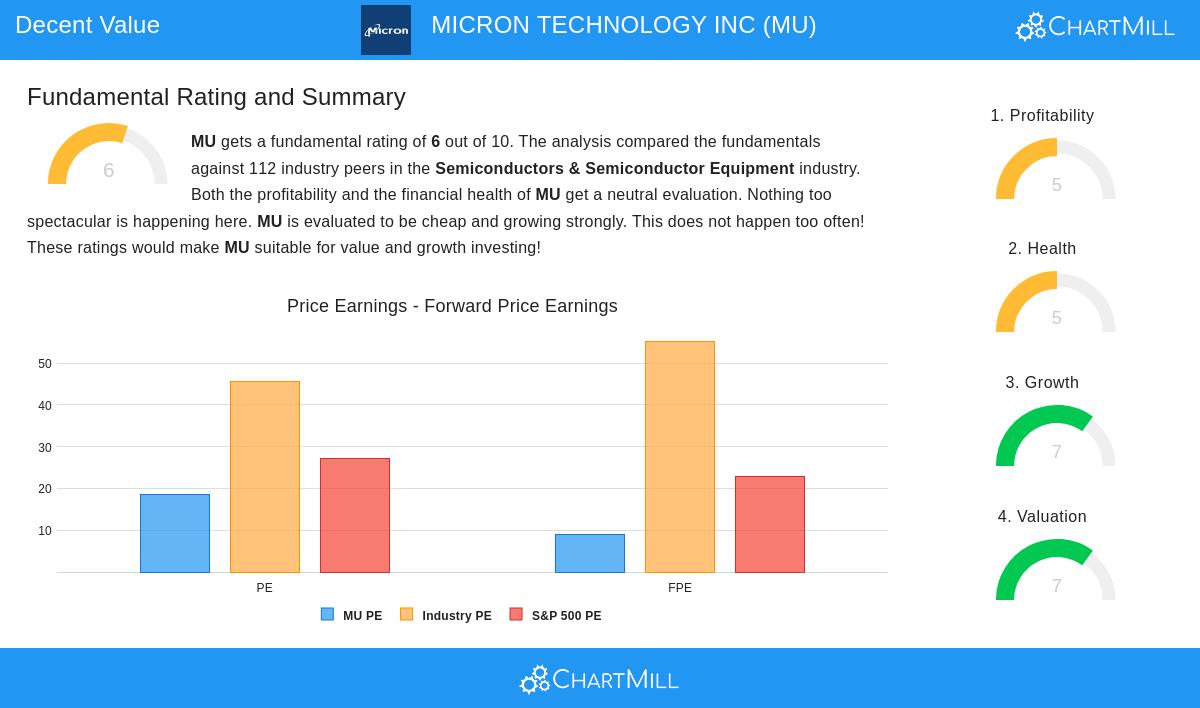

Micron’s attraction starts with its valuation picture, which gets a 7 out of 10 in ChartMill’s review, a score that fits with the value investing idea of looking for undervalued assets. The company’s forward price-to-earnings ratio of 9.00 is especially interesting, seen as lower cost than both the industry average and the S&P 500. This implies that, compared to forecasted earnings, the stock might be priced cautiously. Also, numbers such as enterprise value to EBITDA show Micron is valued more positively than many others in the semiconductors sector. For value investors, these numbers are important: they hint at a possible gap between market price and intrinsic value, giving a buffer against paying too much and matching Graham’s focus on numerical safety margins.

Financial Health and Profitability

While valuation grabs notice, financial health and profitability form the base for lasting undervaluation. Micron’s health score of 5 shows a varied but acceptable situation: its Altman-Z score of 4.73 points to low bankruptcy danger, and a current ratio of 2.75 shows good short-term cash availability. Still, a debt-to-free-cash-flow ratio of 8.26 implies that borrowing needs watching. For profitability, the company receives a 5 score, with notable points containing a return on equity of 12.27% and an operating margin of 22.77%, both doing better than a large number of industry competitors. These figures are significant to value investors since they lower the danger of value traps, companies that look inexpensive but are basically weak. Micron’s capacity to produce profits and keep operational effectiveness backs the idea that its undervaluation could be short-lived instead of a sign of worsening.

Growth Path

Growth is frequently ignored in classic value investing, but it acts as a trigger for achieving intrinsic value. Micron’s growth score of 7 is solid, pushed by a 58.22% rise in revenue over the previous year and an estimated earnings growth rate of 54.74% for the next years. This speed-up in both revenue and profit performance suggests the company is not only low-cost but also set to grow, which might close the difference between its market price and intrinsic value. For value investors, growth confirms the investment theory: it means the undervaluation might adjust as earnings get better, depending less on market mood by itself.

Dividend Considerations

Although not a main point for all value plans, Micron’s dividend picture includes an element of steadiness. With a yield of 0.38% and a record of steady payments, it gives a small income flow while the market re-evaluates the stock’s value. The dividend’s growth rate of 72.66% each year is notable, but questions about how long it can last are present because of slower earnings growth. For investors, this is an extra benefit rather than a central attraction, fitting with value beliefs that emphasize protecting capital and overall return over high income.

Conclusion

Micron Technology offers an interesting case for value-focused investors, mixing appealing valuation with adequate fundamentals in health, profitability, and growth. Its low forward P/E and good growth forecasts imply the market might be undervaluing its future cash flows, while acceptable margins and financial steadiness lessen the danger of lasting capital loss. As with all investments, personal research is needed, particularly in a changing industry like semiconductors, but the numbers point to a possible chance worth more investigation. For those curious to find comparable screened chances, more outcomes are available using this Decent Value Stocks screen.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consult with a financial advisor before making any investment decisions.

258.46

-5.25 (-1.99%)

Find more stocks in the Stock Screener

MU Latest News and Analysis