In the world of long-term investing, few strategies have shown as much endurance as the growth-at-a-reasonable-price (GARP) method made famous by legendary fund manager Peter Lynch. His system highlights finding companies with good but maintainable growth paths, firm financial standing, and prices that do not assume too much future success. This middle-ground way tries to steer clear of both the speculative extremes of pure growth investing and the value traps found in traditional value plans, concentrating instead on fundamentally good businesses available at fair prices.

JD.COM INC-ADR (NASDAQ:JD), China's technology-led e-commerce leader, recently appeared through a filter built on Lynch's investment rules. The company's presence in this filter justifies a more detailed look for investors looking for companies that mix growth traits with fair prices.

Growth Measures and Maintainability

Lynch highlighted the need for maintainable growth, usually looking for companies with earnings growth between 15-30% each year, fast enough to push shareholder gains but not so quick that it cannot continue. JD.com displays good growth traits that match this thinking:

- 5-year EPS growth of 26.75%: This puts the company well within Lynch's chosen growth span, pointing to solid but controlled increase

- Revenue growth path: The company has reached 14.97% average yearly revenue growth over recent years, with experts predicting continued growth ahead

- Forward EPS expectations: Expected yearly EPS growth of 24.95% indicates the company keeps its growth speed

These measures show JD's effective performance in China's competitive e-commerce field, where it has become a frontrunner in electronics and general goods retail while moving into logistics, healthcare, and foreign markets.

Price Evaluation

The heart of Lynch's method involves finding companies whose prices do not completely show their growth possibility. JD.com offers several good price traits:

- P/E ratio of 7.68: Much lower than both industry averages and wider market multiples

- Forward P/E of 7.77: Shows continued good price compared to future earnings expectations

- PEG ratio of 0.29: Far under Lynch's limit of 1.0, hinting the market may be pricing the company's growth possibilities too low

These price measures become especially notable when thinking about JD's market place as China's second-biggest e-commerce company. The lower price compared to growth rates makes what Lynch might call a chance to buy a good growth company at a fair price.

Financial Standing and Earnings

Lynch favored companies with firm balance sheets and earnings measures, thinking these traits offered protection during market drops. JD.com shows several strong points here:

- Return on Equity of 17.02%: Goes beyond Lynch's 15% limit, showing effective use of shareholder money

- Debt-to-Equity ratio of 0.25: Well under the plan's top limit of 0.6 and even below Lynch's stricter liking for ratios under 0.25

- Current Ratio of 1.22: Meets the lowest need for short-term financial steadiness

While the company shows some worries in cash flow measures, its general financial standing seems firm, with positive operating cash flow kept through the past five years and better profit margins showing operational efficiency improvements.

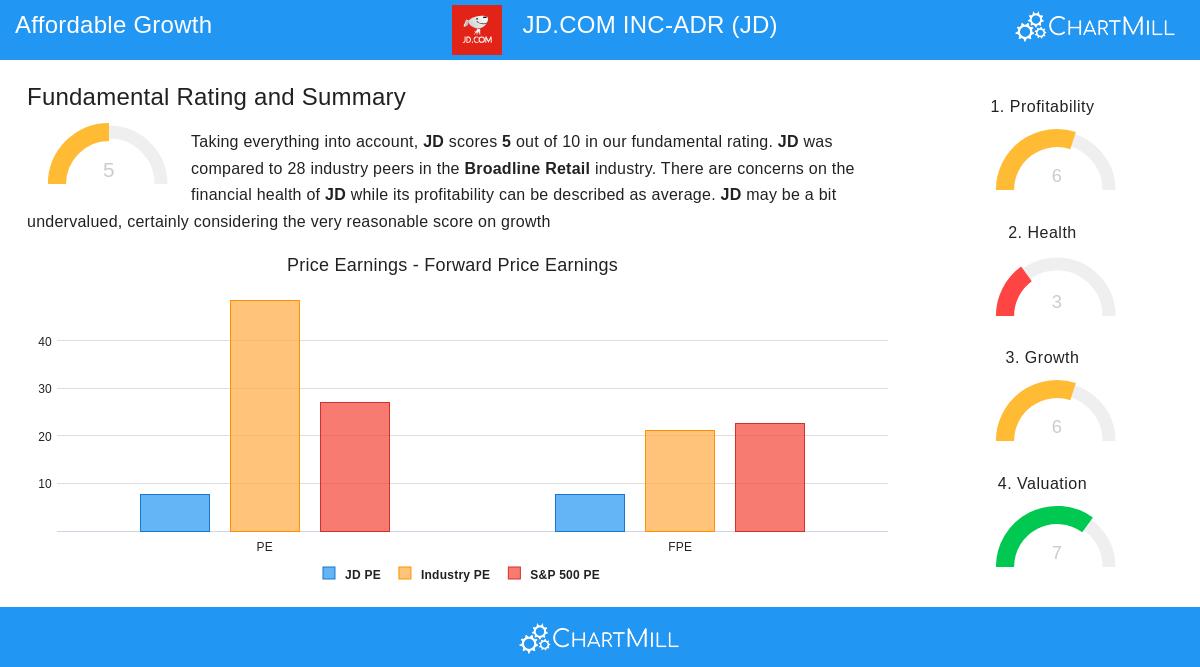

Basic Rating Summary

According to Chartmill's full basic review, JD.com gets a 5 out of 10 overall, with specific strong points in price and growth measures balanced by some worries about financial standing. The company's earnings rating of 6/10 shows acceptable returns on equity and assets, while its growth rating of 6/10 accepts strong past performance with some slowing expected in revenue increase. The price rating of 7/10 emphasizes the stock's good multiples compared to both industry friends and wider market indexes.

Detailed fundamental analysis shows extra details, including the company's fairly new dividend start and specific strong points in debt measures despite some cash flow worries.

Investment Points

For investors thinking about JD.com through a Lynch-style view, several factors deserve notice. The company works in a quickly changing Chinese consumer market, dealing with competition from both traditional sellers and other e-commerce platforms. Rules affecting Chinese technology companies are another factor needing watch. However, JD's set logistics network, increasing healthcare part, and move into new business areas offer multiple growth paths that match Lynch's liking for companies with lasting competitive edges.

The company's fair price offers a safety buffer, while its growth measures hint at possibility for gain if performance continues well. Lynch often noted that investors should know the businesses they own, and JD's fairly clear e-commerce model, though complicated in performance, fits this need for investors knowing the retail and technology areas.

Finding Like Chances

Investors keen on finding other companies that fit Peter Lynch's investment rules can look at more filter results through our specialized stock screener. This tool allows for more changes based on specific investment likes while keeping the main ideas of the Lynch system.

Disclaimer: This review is given for information only and does not make investment guidance, a suggestion, or a deal to buy or sell any securities. Investors should do their own study and talk with a qualified financial advisor before making investment choices. Past performance does not show future results, and all investments hold risk, including possible loss of original money.