JD.COM INC-ADR (NASDAQ:JD) stands out as a potential fit for investors seeking growth at a reasonable price (GARP). The company, a major player in China’s e-commerce sector, meets several key criteria from Peter Lynch’s investment strategy, combining solid growth with sound financial health and an attractive valuation.

Why JD Fits the GARP Approach

- Strong Earnings Growth: JD has delivered an impressive 5-year average EPS growth of 26.75%, well above the minimum 15% threshold in Lynch’s strategy. This indicates sustained profitability without excessive growth that could be unsustainable.

- Attractive Valuation: With a PEG ratio of 0.25 (based on past 5-year growth), JD is priced attractively relative to its earnings growth. A PEG below 1 suggests the stock may be undervalued given its growth trajectory.

- Healthy Profitability: The company’s Return on Equity (ROE) of 19.26% exceeds Lynch’s 15% benchmark, reflecting efficient use of shareholder capital.

- Conservative Debt Levels: JD’s Debt/Equity ratio of 0.24 is well below the 0.6 limit Lynch preferred, indicating a strong balance sheet with minimal reliance on borrowing.

- Solid Liquidity: A Current Ratio of 1.26 ensures the company can meet short-term obligations, though liquidity metrics are slightly weaker than some peers.

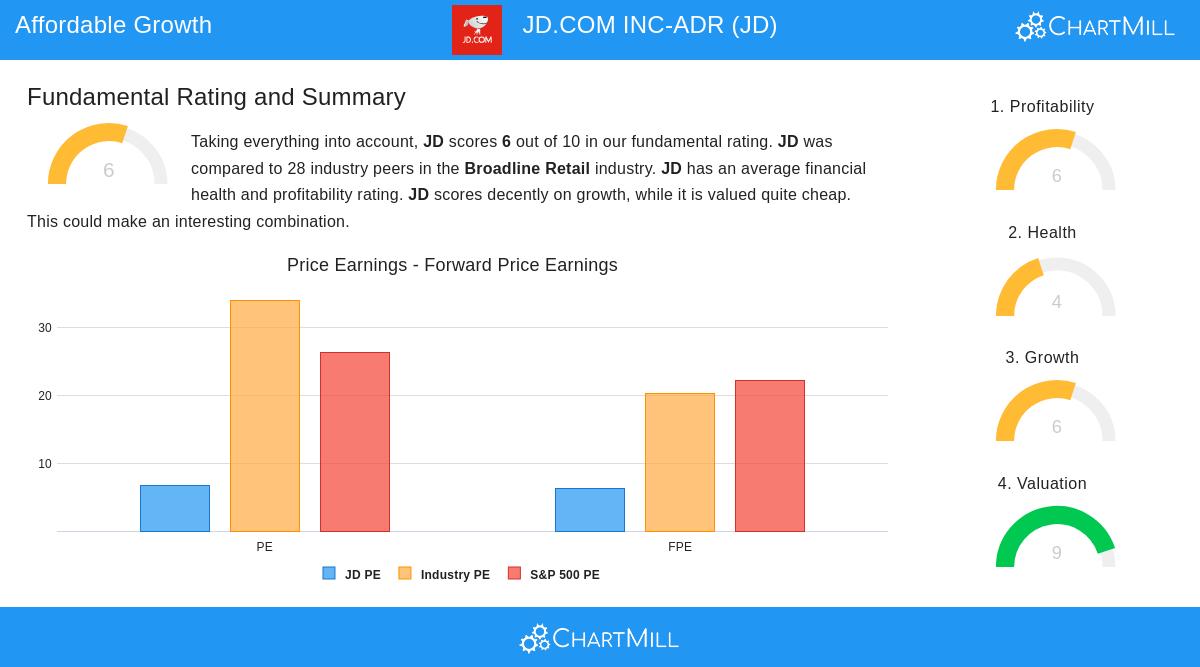

Fundamental Snapshot

JD’s overall fundamental rating of 6/10 reflects balanced strengths in profitability and valuation, though liquidity metrics are a minor concern. Key highlights:

- Valuation: JD trades at a P/E of 6.63, significantly below both industry and S&P 500 averages, suggesting undervaluation.

- Growth: Revenue has grown at 14.97% annually over the past 5 years, with EPS expected to grow 25.85% yearly in the near term.

- Dividend: A yield of 2.99% adds income appeal, though the company’s dividend history is relatively short.

For a deeper dive, review the full fundamental analysis report.

Our Peter Lynch Strategy screener lists more stocks matching these criteria and is updated daily.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should always conduct your own analysis before making investment decisions.