In value investing, the search for undervalued stocks often involves finding companies whose market price does not match their intrinsic worth, based on an analysis of financial health, profitability, growth potential, and valuation measures. This method, built on the ideas of Benjamin Graham and later developed by investors like Warren Buffett, focuses on buying securities that seem underpriced according to fundamental analysis. One way to simplify this process is with screening tools that assess stocks using composite scores across important areas, like valuation, health, profitability, and growth. A stock that rates well in valuation while also having acceptable scores in other fundamental areas might be an opportunity for value-focused investors looking for a margin of safety.

ILLUMINA INC (NASDAQ:ILMN) recently appeared through such a screening process, specifically a "Decent Value" screen that looks for equities with good valuation ratings along with satisfactory health, profitability, and growth measures. This screening approach fits with value investing principles, as it focuses on stocks that may be undervalued by the market but still show solid underlying fundamentals, reducing the risk of value traps and raising the chance of price improvement as the market adjusts its view.

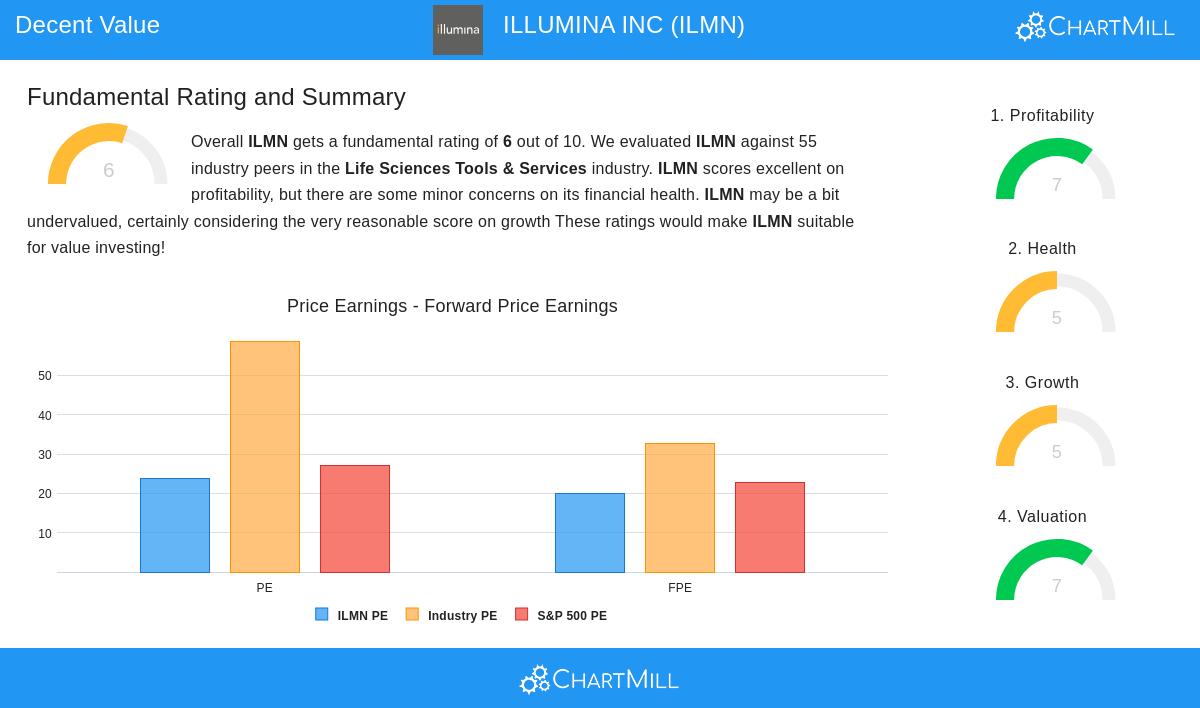

Valuation Metrics

The valuation rating for Illumina is notable, with a score of 7 out of 10, showing the stock is priced well compared to its fundamentals and industry peers. Key points from the fundamental analysis report include:

- Enterprise Value to EBITDA: Illumina is valued more cheaply than 87.27% of its industry peers, suggesting it may be undervalued based on cash flow generation.

- Price/Free Cash Flow: Similarly, 90.91% of companies in the Life Sciences Tools & Services industry are more expensive on this measure, pointing to a possible discount.

- PEG Ratio: Accounting for growth, the PEG ratio shows a rather cheap valuation, supported by an expected earnings growth rate of 31.99% in the next few years.

For value investors, these valuation measures are important because they help find differences between market price and intrinsic value. A lower valuation multiple, along with good growth expectations, can indicate an opportunity where the market has not yet fully recognized the company's future potential, offering that key margin of safety.

Financial Health

Illumina's financial health rating is a moderate 5 out of 10, showing some strengths and some minor concerns. Important aspects include:

- Solvency: The company has an Altman-Z score of 3.57, which indicates financial health and a low risk of bankruptcy, doing better than 72.73% of industry peers.

- Debt Management: With a debt-to-free-cash-flow ratio of 1.93, Illumina shows high solvency, requiring less than two years to pay off all debts, which is better than 85.45% of competitors.

- Liquidity: Current and quick ratios are acceptable but are behind some peers, indicating room for improvement in short-term financial flexibility.

A good financial health score is important for value investors, as it lowers the risk of insolvency or financial trouble that could reduce intrinsic value. While Illumina displays strong solvency, the varied liquidity measures remind investors to watch working capital management carefully.

Profitability

Scoring a 7 out of 10 for profitability, Illumina shows strong earnings power and efficiency:

- Margins: The company has a profit margin of 29.37%, doing better than 98.18% of the industry, and an operating margin of 20.59%, better than 87.27% of peers.

- Returns: Return on assets (20.67%) and return on equity (55.71%) are near the top in the sector, showing effective use of resources.

- Cash Flow: Steady positive operating cash flow over the past five years shows reliable profitability.

High profitability is a key part of value investing, as it suggests a company can maintain earnings and cash flows, supporting a higher intrinsic value. Illumina's excellent margins and returns confirm its competitive position and ability to generate shareholder value.

Growth Prospects

With a growth rating of 5 out of 10, Illumina presents a mixed but hopeful outlook:

- Past Performance: Earnings per share (EPS) grew 352.17% in the last year, though five-year annualized EPS growth is negative at -17.93%, and revenue decreased slightly recently.

- Future Expectations: EPS is expected to grow 23.70% each year in the next few years, with revenue projected to rise by 3.57%.

Growth is significant in value investing because it can push future cash flows and intrinsic value higher. While past growth has been uneven, the good forward EPS expectations suggest a possible recovery, making Illumina an interesting candidate for investors expecting better performance.

Conclusion

Illumina Inc represents an interesting case for value investors, mixing appealing valuation multiples with strong profitability, acceptable financial health, and positive growth forecasts. Its screening profile, highlighting a valuation score of 7 along with satisfactory ratings in other fundamental areas, suggests it may be undervalued compared to its peers and future potential. However, investors should do more due diligence, thinking about industry trends, competitive factors, and wider market conditions.

For those interested in finding similar investment opportunities, more results from the "Decent Value" screen can be found here.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Readers should perform their own research and consult with a qualified financial advisor before making any investment decisions.