When evaluating dividend-paying stocks, investors often look for companies that not only offer good yields but also show lasting financial strength and profit. The process for choosing these stocks usually includes looking for high dividend ratings while making sure there are acceptable scores in profit and financial strength measures. This method helps find companies able to keep and possibly increase their dividends over time, instead of those with high yields that might be in danger because of basic operational or financial problems.

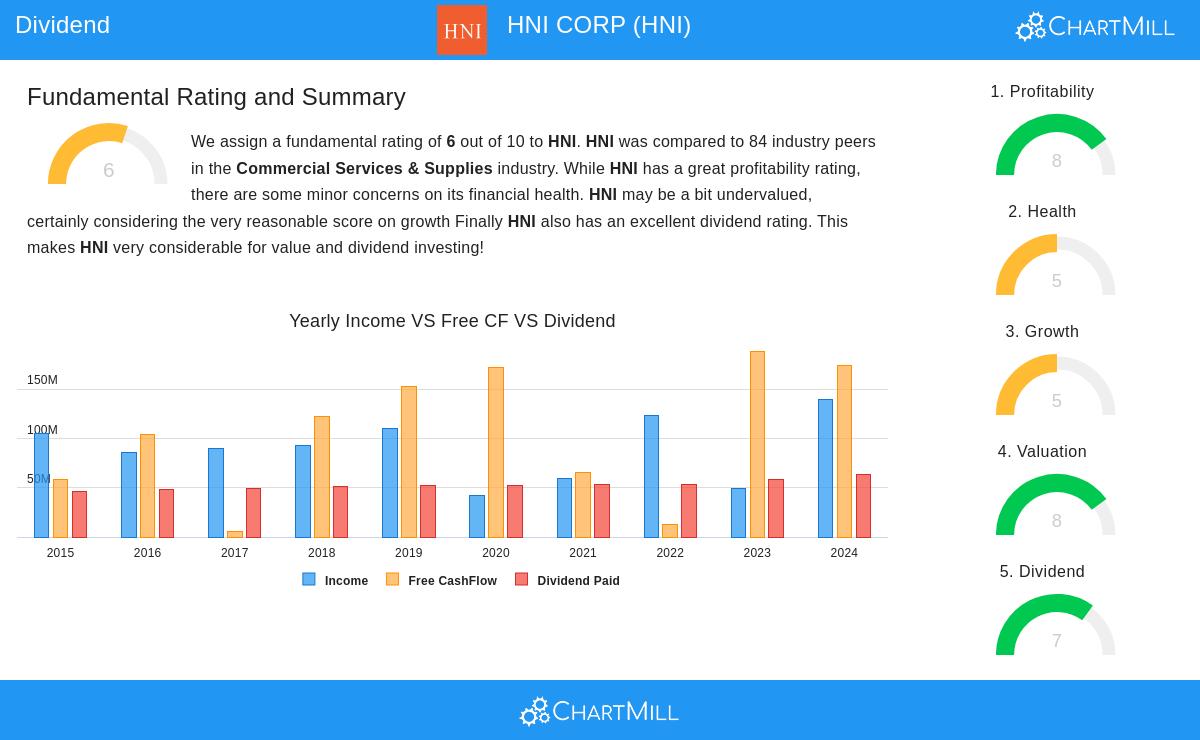

HNI CORP (NYSE:HNI) appears as a candidate to look at through this view. The company, which supplies workplace furnishings and residential building products, works in a steady industry and has a history of steady results. Its basic report shows a dividend rating of 7 out of 10, helped by a yield of 3.07% that is higher than both the industry average of 2.30% and the S&P 500 average of about 2.36%. Most importantly, HNI has kept a dependable dividend history, with no reductions for at least ten years, and a small yearly growth rate of 3.58% in its payments. This steadiness is an important point for dividend investors, as it lowers the chance of sudden cuts and supports long-term income security.

Apart from the dividend-specific numbers, HNI shows good profit, with a rating of 8 out of 10. The company’s return on equity is 18.24%, doing better than 85.71% of others in the commercial services and supplies industry, while its profit margin of 5.73% also puts it ahead of most competitors. These numbers point to efficient use of money and strong operational results, which are important for maintaining dividend payments. Profit makes sure a company has enough earnings to pay its dividends without hurting growth or financial security, matching the screening method’s focus on lasting income creation.

Financial strength, though not outstanding with a rating of 5, still meets the "acceptable" level needed by the screen. HNI’s solvency numbers are satisfactory, with an Altman-Z score of 3.43 pointing to no near-term bankruptcy risk, and a debt-to-equity ratio of 0.56 that matches industry standards. However, investors should be aware of the lower quick ratio of 0.93, which might show some near-term cash flow limits. Even with this, the total strength profile supports the idea that the company is not carrying too much debt and can handle its duties, which is needed for continuous dividend payments.

Valuation numbers add to HNI’s attractiveness, with a price-to-earnings ratio of 12.76 that is less expensive than 83.33% of industry peers and much lower than the S&P 500 average. This lower price, along with expected EPS growth of 15.76%, hints at possibility for price increase together with dividend income. For dividend investors, such valuations give a safety buffer, lowering risk while offering yield and growth potential.

In summary, HNI presents a well-rounded opportunity for investors focused on dividends, mixing a good yield with shown sustainability, supported by strong profit and sufficient financial strength. Those wanting to look into similar investment ideas can find more screened results using the Best Dividend Stocks screen. For a complete look at HNI’s basics, readers can see the full fundamental report.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consider their financial situation before making any investment decisions.