Investors looking for growth opportunities at reasonable prices often consider strategies that balance expansion potential with financial care. The "Affordable Growth" method focuses on companies showing solid growth paths while keeping good profitability and financial condition, all without requiring high valuation premiums. This process tries to find businesses that mix operational quality with appealing prices, possibly providing lasting returns without the increased risks linked to speculative investments. One company appearing from this process is Halozyme Therapeutics Inc (NASDAQ:HALO).

Growth Trajectory

The central idea of any growth strategy is a company's capacity to grow its operations and earnings, and Halozyme performs well on this point. A ChartMill Growth Rating of 8/10 highlights its solid expansion, which is important for the Affordable Growth screen as it looks for companies with real, above-average growth outlooks instead of just potential.

- Revenue Growth: The company has grown its revenue by 34.97% over the past year, with an average yearly growth rate of 38.95% over recent years.

- Earnings Per Share (EPS) Growth: EPS has increased by 58.41% in the last year, supported by a solid historical average growth of 30.12%.

- Future Expectations: Analysts forecast continued growth, with expected average yearly EPS growth of 17.63% and revenue growth of 12.63% in the coming years.

This steady and solid historical growth, along with positive future estimates, places Halozyme as a company with a demonstrated ability to grow its business efficiently.

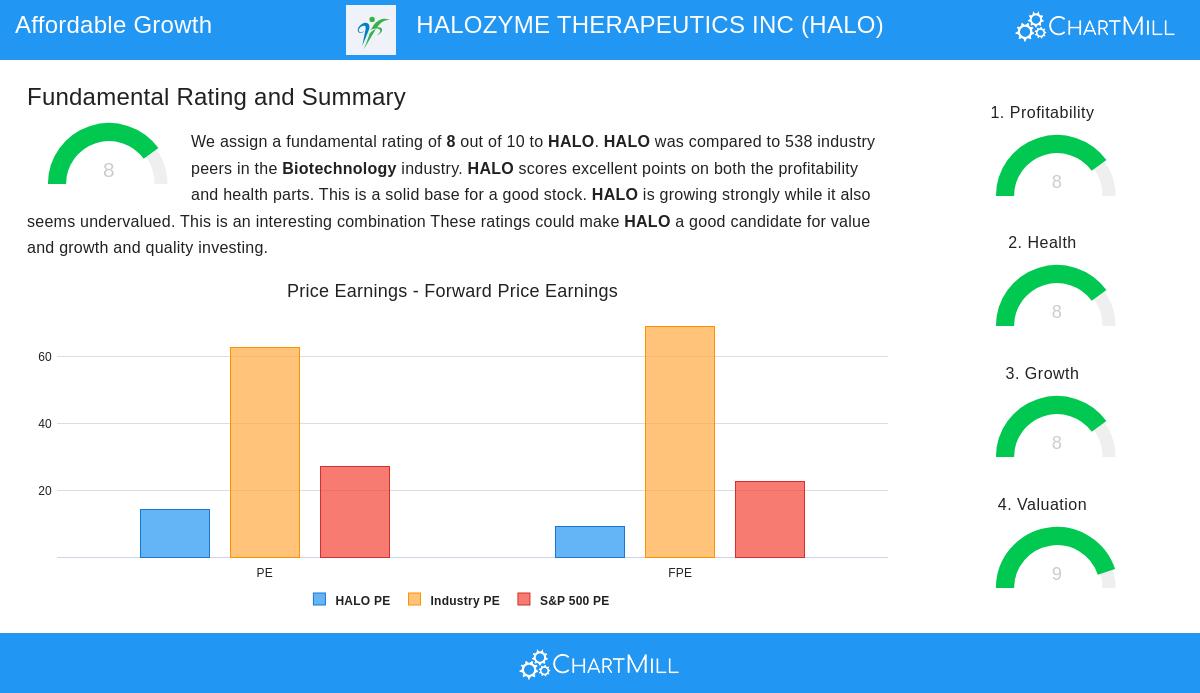

Valuation Metrics

The "Affordable" part of the strategy is essential, making sure investors do not pay too much for growth. Halozyme's ChartMill Valuation Rating of 9/10 shows it is priced appealingly relative to both its industry and its own growth outlook, a main filter in the screen to prevent overvalued investments.

- Price-to-Earnings (P/E): The company's P/E ratio of 14.28 is much lower than the biotechnology industry average of 62.77, making it less expensive than 96% of its peers. It is also well below the S&P 500 average.

- Forward P/E: An even more attractive forward P/E of 9.16 indicates the valuation stays appealing based on future earnings forecasts.

- Price-to-Free-Cash-Flow and EV/EBITDA: These multiples also show Halozyme is valued as less expensive than over 95% of its industry competitors.

This mix of high growth and moderate valuation multiples is uncommon and fits well with the Growth at a Reasonable Price (GARP) idea, suggesting the market may not be fully recognizing the company's earnings capacity.

Profitability and Financial Health

While growth and valuation are the main screens, the strategy also needs acceptable profitability and financial health to make sure the company's growth is lasting and not built on weak foundations. Halozyme performs well here too, with a Profitability Rating of 8/10 and a Health Rating of 8/10.

- Profitability Strength:

- The company has exceptional margins, including a Profit Margin of 47.28% and an Operating Margin of 57.92%, placing it in the top group of its industry.

- Return measures are similarly notable, with a Return on Invested Capital (ROIC) of 28.55%, greatly exceeding its cost of capital and pointing to highly efficient use of investor money.

- Financial Stability:

- Halozyme shows high liquidity, with a Current Ratio of 8.36, meaning it has sufficient resources to meet short-term responsibilities.

- Its Altman-Z score of 5.51 indicates a low near-term chance of financial trouble.

- A point to note is a somewhat high Debt-to-Equity ratio; however, this is balanced by a solid Debt-to-Free-Cash-Flow ratio of 2.79, indicating the company can reduce its debt promptly with its current cash flow.

These solid ratings in profitability and health offer an important safety measure, showing that Halozyme's growth is backed by a fundamentally healthy and well-run business operation.

Conclusion

Halozyme Therapeutics Inc presents a strong case for investors using an Affordable Growth strategy. The company's notable revenue and earnings growth meet the strategy's need for expansion, while its appealing valuation multiples make sure this growth is not bought at a high price. Additionally, its exceptional profitability and sound financial health give assurance in the durability of its business model. This uncommon combination of solid growth, fair valuation, and operational quality makes HALO a significant candidate for more study by those looking for growth at a reasonable price.

For investors interested in finding other companies that match this specific profile, more results from the Affordable Growth screen can be found here. A detailed fundamental analysis report for Halozyme is available for more review here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation to buy, sell, or hold any security, or an endorsement of any investment strategy. All investments involve risk, including the possible loss of principal. Readers should conduct their own research and consult with a qualified financial advisor before making any investment decisions.