For investors looking for a mix of chance and caution, the Growth at a Reasonable Price (GARP) or "affordable growth" method provides a solid middle path. This method tries to find companies that are increasing their earnings and sales at a good rate and are also available at prices that are not too high. By searching for stocks with good growth foundations, acceptable profit and money strength, and a fair cost, investors can take part in a company's rise while keeping some protection from paying too much. One stock that recently came up through this kind of search is Halozyme Therapeutics Inc (NASDAQ:HALO).

A Look at Foundational Strength

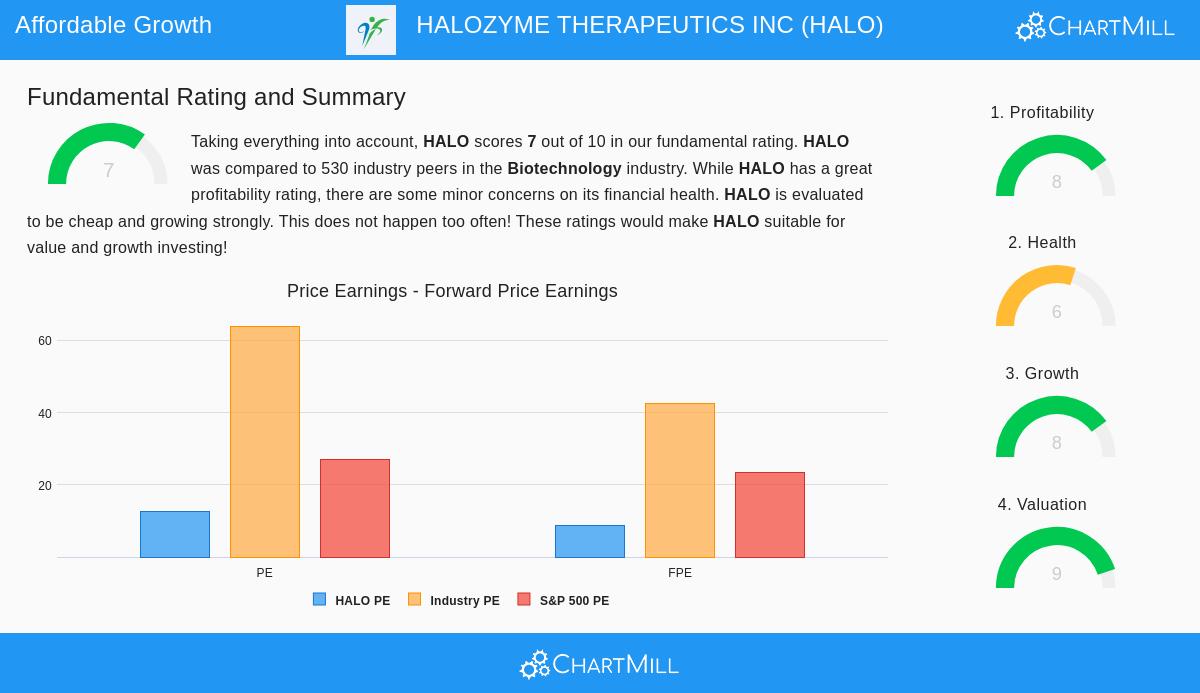

A close fundamental analysis report on ChartMill gives Halozyme a total score of 7 out of 10, measuring it against 530 others in the tough biotechnology field. The report shows the company's position in five key parts: Growth, Valuation, Health, Profitability, and Dividend. For an affordable growth method, the high scores are in Growth (8/10) and Valuation (9/10), helped by good scores in Profitability (8/10). This mix points to a company that is performing effectively, making money, and is still offered at a good price compared to its future.

Strong Growth Path

The central idea of any growth investment is, expectedly, growth. Halozyme performs very well here, getting its high growth score from both past results and what is expected next.

- Past Results: The company has shown notable enlargement. Over the last year, Earnings Per Share (EPS) rose by a strong 48.55%, while Revenue went up by 31.19%. The view over more years is even more notable, with average yearly EPS increase of 30.12% and revenue increase of almost 39% over recent years.

- Next Expectations: Experts think this movement will keep going, though at a slower speed. EPS is predicted to grow at an average yearly rate of 17.25%, with revenue growth expected at 12.82%. While these future guesses show a slowdown from the high past rates, they still signal a solid and better-than-average growth picture.

This steady history and believable future view are key for the affordable growth filter, as they find companies with shown and expected business movement.

A Good Valuation Picture

Finding growth is only part of the task; paying a sensible cost for it is what makes the "affordable" part. Halozyme's valuation score of 9/10 suggests the market may not be completely counting its quality and growth, showing a possible chance.

- Earnings Measures: The stock sells at a Price/Earnings (P/E) ratio of 12.65, which is seen as fair on its own. More significantly, it costs less than about 97% of its biotechnology field competitors. The forward P/E ratio of 8.59 shows an even more interesting picture, suggesting the stock is priced low compared to both its field and the wider S&P 500.

- Cash Flow and EBITDA: The good valuation goes past earnings. Halozyme's Enterprise Value to EBITDA and Price to Free Cash Flow ratios are also lower than over 96% of field rivals.

- Growth Pay: The PEG ratio, which changes the P/E for expected growth rates, shows a low cost relative to the company's growth outlook. The report states that Halozyme's excellent profitability might support a higher measure.

This valuation setting is important for the filtering method. It makes sure that found companies are not "hope stocks" selling at very high prices, but rather growth cases that can be bought at a fair starting point.

Supporting Foundations: Profitability and Health

For growth to last and the valuation to be reasonable, a company must be profitable and financially stable. Halozyme scores well on profitability, with an 8/10 rating pushed by very good margins and returns.

- High Margins and Returns: The company has a Profit Margin of 47.91% and an Operating Margin of 59.33%, putting it in the best group of its field. Its Return on Equity (118.17%) and Return on Invested Capital (42.77%) are similarly excellent, showing very effective use of money.

- Financial Health Points: The financial health score of 6/10 gives a more varied picture, which investors should see. On the good side, Halozyme is building value (ROIC is above its cost of capital), has been lowering its share count, and has a workable debt-to-free-cash-flow ratio. The main worry is in its cash metrics, with Current and Quick ratios that are below field averages, and a Debt-to-Equity ratio of 1.59 that is seen as high. While the Altman-Z score shows no short-term failure risk, the higher debt is a point to watch, particularly in a money-heavy area like biotech.

Summary

Halozyme Therapeutics shows a solid example for the affordable growth investment path. The company displays the two traits this method looks for: a strong, clear growth machine combined with a valuation that seems low relative to both its own outlook and its field. Its top-level profitability gives a firm base for this growth. While the higher debt amount and lower cash ratios need notice from a risk view, the total foundational picture, especially the effective mix of growth and price, makes HALO a stock worth more study for investors following the GARP idea.

This study was built on a stock filter made to find affordable growth chances. You can look at more possible picks from this filter here.

Disclaimer: This article is for information only and is not financial guidance, a suggestion to buy or sell any security, or a support of any investment method. The information shown is based on data given and foundational analysis reports available when written. Investors should do their own complete study and think about their personal money situation and risk comfort before making any investment choices.