Infrastructure specialist Granite Construction Inc (NYSE:GVA) has recently appeared as a candidate for value investors, identified through a screening process that highlights strong valuation metrics with good fundamentals. This method, based on classic value investing principles, looks for companies trading below their intrinsic worth while keeping financial health, profitability, and growth potential, key signs that the market may be missing a fundamentally good business.

Valuation Metrics

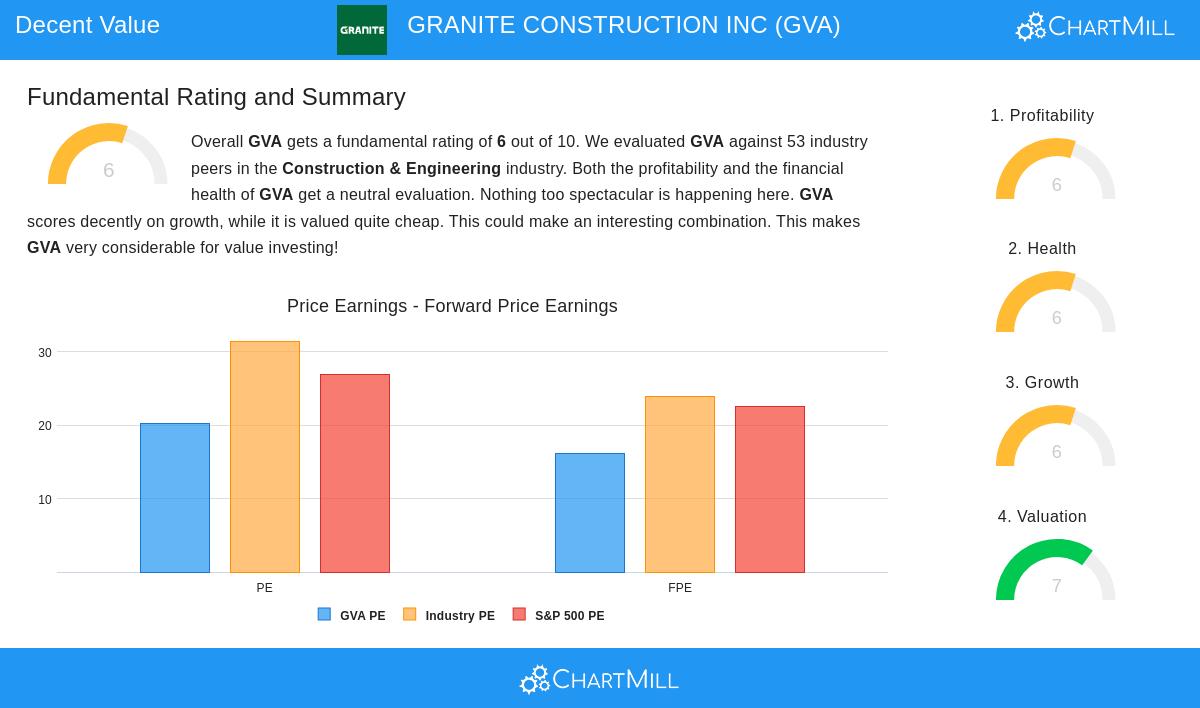

Granite Construction’s valuation profile is notable, receiving a ChartMill Valuation Rating of 7 out of 10. This score indicates several positive metrics that imply the stock may be undervalued compared to both its industry and the wider market.

- Price-to-Earnings (P/E) Ratio: At 20.25, GVA’s P/E is lower than the industry average of 31.45 and the S&P 500 average of 26.84, suggesting a cheaper entry point.

- Forward P/E Ratio: The forward P/E of 16.15 is not only below the industry average of 23.91 but also under the S&P 500’s 22.48, pointing to expected earnings growth without a high price.

- Enterprise Value to EBITDA: The company is ranked cheaper than 81% of its peers on this measure, supporting the valuation case.

- PEG Ratio: A low PEG ratio, which modifies the P/E for growth, implies the stock is fairly priced considering its earnings expansion outlook.

For value investors, these metrics are important. They help find differences between market price and intrinsic value, a basic part of the value investing strategy, which believes such differences usually narrow over time as the market fixes its mispricing.

Financial Health

Granite Construction has a Financial Health Rating of 6, showing a stable but careful financial position. Key points are:

- Solvency: The company’s Altman-Z score of 3.43 shows low bankruptcy risk and does better than 62% of industry peers. Its debt-to-free-cash-flow ratio of 2.40 is good, meaning it can pay down debt fairly fast.

- Liquidity: With a current ratio of 1.57 and quick ratio of 1.45, GVA shows enough short-term liquidity, ranking higher than many competitors in these areas.

- Debt Management: A debt-to-equity ratio of 0.69 shows moderate leverage, although it is manageable considering the company’s cash flow situation.

A good financial health score is important for value investors, as it lowers the risk of value traps, companies that seem cheap but are actually in financial trouble. Stability here supports the idea that the undervaluation is short-term and not a sign of more serious issues.

Profitability

The company’s Profitability Rating of 6 shows sufficient, if not outstanding, earnings power. Important strengths include:

- Return Metrics: Return on assets (5.10%) and return on equity (14.91%) both do better than a majority of industry peers.

- Margins: A profit margin of 3.89% is above the industry median, and both operating and gross margins have improved lately.

- Earnings Consistency: GVA has reported positive earnings in four of the last five years, with steady positive operating cash flow, a signal of operational dependability.

Profitability is a key filter in value investing because it helps verify that a company is not only cheap, but also able to produce returns. This matches the value idea of looking for quality businesses at lower prices.

Growth Prospects

Granite Construction’s Growth Rating of 6 indicates a stable growth path, mixing past performance with future forecasts.

- Historical Growth: EPS grew almost 60% over the past year, with a three-year annualized growth rate of 32.75%. Revenue growth has been more moderate but consistent.

- Forward Estimates: EPS is expected to grow by 24.45% each year in the next few years, exceeding expected revenue growth of 5.46%.

Growth is particularly important in value investing because it can drive a revaluation. If earnings increase as forecast, the market may value the stock higher, reducing the difference between price and intrinsic value.

Conclusion

Granite Construction offers a strong case for value-focused investors. Its appealing valuation ratios, along with decent scores in health, profitability, and growth, suggest a company that is possibly undervalued without losing fundamental quality. These characteristics are precisely what value screens try to find: stocks that provide a margin of safety while keeping operational strength.

For investors wanting to find similar opportunities, more screened results based on these criteria can be found using this Decent Value Stocks screen.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consider their financial situation and risk tolerance before making investment decisions.