Investors looking for growth chances often face the task of weighing expansion possibility against fair cost. The Growth at a Reasonable Price (GARP) method tackles this by selecting companies showing solid growth paths alongside acceptable valuations. This tactic steers clear of both excessively priced high-growth stocks and stagnant value options, concentrating instead on businesses with lasting expansion possibilities available at moderate prices. One filtering system that uses this method searches for stocks with growth grades over 7, valuation marks over 5, and satisfactory earnings and financial strength measures.

Granite Construction Inc (NYSE:GVA) appears as a candidate deserving of a closer look with this view. The infrastructure solutions company provides construction and materials services throughout the United States, concentrating on roads, bridges, rail lines, and other important infrastructure projects.

Growth Path

Granite Construction's growth picture is notable, receiving a growth grade of 7 out of 10 in its fundamental analysis report. The company shows solid expansion in several measures:

- Earnings Per Share rose 61.71% over the last year

- Average yearly EPS expansion of 32.75% over recent years

- Revenue grew 14.20% in the most recent reporting period

- Future EPS expansion forecast at 21.70% per year

- Revenue expansion projections of 9.43% per year going forward

This mix of good past results and acceptable future projections offers assurance in the company's capacity to continue its progress. The quickening in revenue expansion forecasts versus past rates points to better business circumstances and performance.

Valuation Review

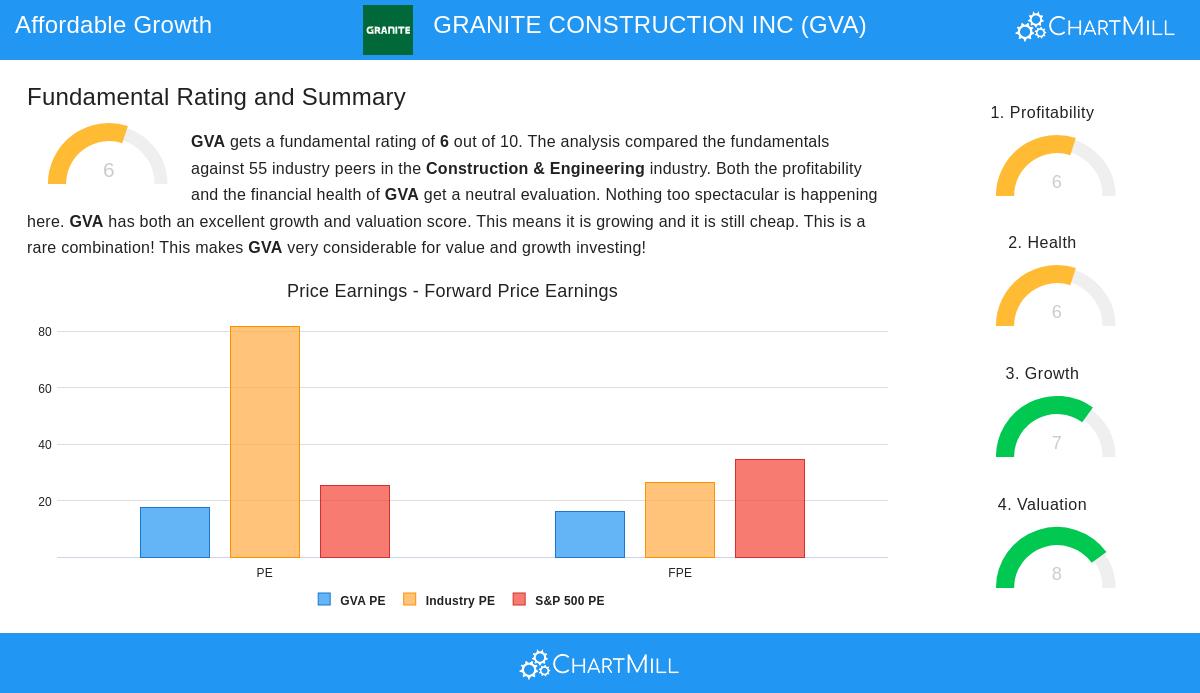

The company's valuation measures show a pleasing picture, scoring 8 out of 10 on the valuation scale. Even with a P/E ratio of 17.69 that seems fair next to the S&P 500's 25.45 average, Granite Construction displays especially good value inside its industry setting:

- P/E ratio much lower than industry average of 81.76

- Forward P/E of 16.19 stacks up well against industry average of 26.31

- Enterprise Value to EBITDA ratio more affordable than 78% of industry members

- Price/Free Cash Flow ratio more affordable than 84% of rivals

- Low PEG ratio signaling inexpensive valuation when expansion is factored in

This valuation placement is key for the affordable growth plan, as it implies the market has not completely accounted for the company's expansion potential, giving investors a good opportunity.

Earnings and Financial Strength

While growth and valuation propel the investment case, Granite Construction keeps satisfactory supporting basics. The company scores 6 out of 10 for both earnings and financial strength, suggesting space for betterment but no significant warning signs.

Earnings strong points contain:

- Return on Assets of 5.10% is higher than 62% of industry members

- Return on Equity of 14.91% is better than 64% of rivals

- Profit Margin of 3.89% puts company in the better half of the industry

- Getting better profit and gross margins in recent periods

Financial strength points:

- Altman-Z score of 3.38 shows no bankruptcy worry

- Debt to Free Cash Flow ratio of 2.40 indicates good solvency

- Current ratio of 1.57 gives sufficient short-term cash availability

- Quick ratio of 1.45 shows financial adaptability

These measures support the affordable growth idea by verifying the company's expansion is supported by lasting operations instead of financial tactics or extreme risk.

The mix of good growth measures, pleasing valuation compared to both the market and industry members, and satisfactory supporting basics makes Granite Construction a noteworthy candidate for investors using a Growth at a Reasonable Price plan. The company's place within the infrastructure field gives extra background, as continuing government funding and private investment in construction projects may support the growth path.

For investors wanting to find comparable chances, more affordable growth candidates are available using this pre-configured stock screen that finds companies with good growth, acceptable valuation, and satisfactory fundamental health.

Disclaimer: This article presents factual information and analysis for educational purposes only and does not constitute investment advice, recommendation, or endorsement of any security. Investors should conduct their own research and consult with financial advisors before making investment decisions.