Fed: Third Cut, Louder Dissent

The Federal Reserve cut its policy rate by 25 basis points to a range of 3.50–3.75%, the third consecutive cut and the lowest level in three years. The vote was 9–3, with one official pushing for a 50 bp cut and two wanting no cut at all, the sharpest internal split since 2019.

In its statement, the Fed acknowledged that job growth has slowed and unemployment has risen enough that the labor market is no longer “tight”, even as core inflation is still expected to hover around 2.5% next year.

The dot plot now signals:

- just one more cut penciled in for 2026,

- and another small step in 2027,

which is Fed-speak for: “We’ve done a lot already, don’t expect a rate-cut party every meeting.”

The Fed is trying to thread a very narrow needle - softening the labor market without letting inflation re-accelerate - while also signaling to markets that the bar for further cuts is now higher.

Adding spice to that backdrop, President Donald Trump is openly preparing to replace Fed Chair Jerome Powell when his term ends in May 2026 and has floated names like Kevin Warsh and Kevin Hassett. That injects a new layer of political risk into the rate path: markets are no longer just reading the dot plot, they’re also trying to handicap Trump’s preferred central banker.

On the macro side:

- The 10-year Treasury yield slipped to around 4.16%, continuing a three-cut, three-month slide that’s easing pressure on valuations and housing.

- The euro strengthened to roughly $1.17, as the dollar sold off on the Fed’s more cautious guidance.

- Brent crude settled near $62.5 (+0.9%) and WTI around $58.8 (+0.6%) as traders weighed the Fed cut against fresh geopolitical jitters from a U.S. seizure of a sanctioned oil tanker off Venezuela.

Net-net, I’d call this a “dovish-enough” day: risk assets higher, dollar weaker, but no sense the Fed has fully capitulated to market easing dreams.

Chips in the Crosshairs: Intel, AMD and Texas Instruments

One of the more uncomfortable stories of the day came from the semiconductor space. Lawsuits filed in Texas accuse Intel (INTC | +0.69%), Advanced Micro Devices (AMD | -0.09%) and Texas Instruments (TXN | +1.2%) of failing to prevent their chips from ending up in Russian missiles and Iranian drones used in attacks on Ukrainian civilians.

According to the filings, components from these companies were found in debris from precision weapons such as KH-101 cruise missiles and Iskander ballistic missiles. The core allegation: “willful ignorance” of diversion risks and inadequate controls on sanctioned products. All three firms say they comply with export rules and stopped doing business in Russia after the invasion.

From a portfolio perspective, I see two takeaways:

-

Headline risk: these suits won’t break the earnings model overnight, but they do add legal and reputational overhang, especially if U.S. regulators decide they need to “make an example” in this cycle.

-

Compliance costs: expect more capex in traceability, tighter distributor oversight (Mouser and others are explicitly named), and potentially stricter end-user screening. That’s margin-negative at the margin, even if it’s the right thing to do.

Interestingly, the market reaction was muted rather than panicked, which tells me investors see this more as a slow-burn risk than an immediate earnings shock.

GE Vernova: Pure Play on the AI Power Crunch

If you want one ticker that captures the market’s current obsession with AI infrastructure, it’s GE Vernova (GEV | +15.62%).

The stock surged roughly 16% after the company’s investor day, where management laid out a markedly more bullish roadmap:

-

Revenue expected to grow from $36–37 billion this year to $52 billion by 2028.

-

EBITDA margin targeted to rise from 14% to 20%.

-

Cumulative free cash flow between 2025–2028 upgraded to $22 billion, versus a prior target of $14 billion.

Year-to-date, GE Vernova is up around 108%, making it one of the best performers in the S&P 500. The story is simple but powerful: the AI boom and electrification wave are driving huge incremental demand for generation, grid and transmission capacity in the U.S., and GE Vernova sits right in that flow.

My view: "Why GE Vernova Surged 16% in a Single Session"

Media & Streaming: Warner Enjoys Takeover Gossip

In media, Warner Bros. Discovery (WBD | +4.49%) enjoyed another speculative spike as investors bet that Netflix (NFLX | -4.14%) and Paramount Skydance (PSKY | +0.55%) could end up in some kind of bidding dance around the company.

There’s no firm deal on the table yet, but the price action tells you how hungry the market is for consolidation in streaming after a brutal, capital-intensive arms race. In plain English: everyone has spent billions chasing subscriber growth, and very few platforms are earning their cost of capital.

For now, I treat this as speculative optionality rather than a base-case M&A thesis, but if we get even a whiff of formal talks, legacy media could re-rate in a hurry.

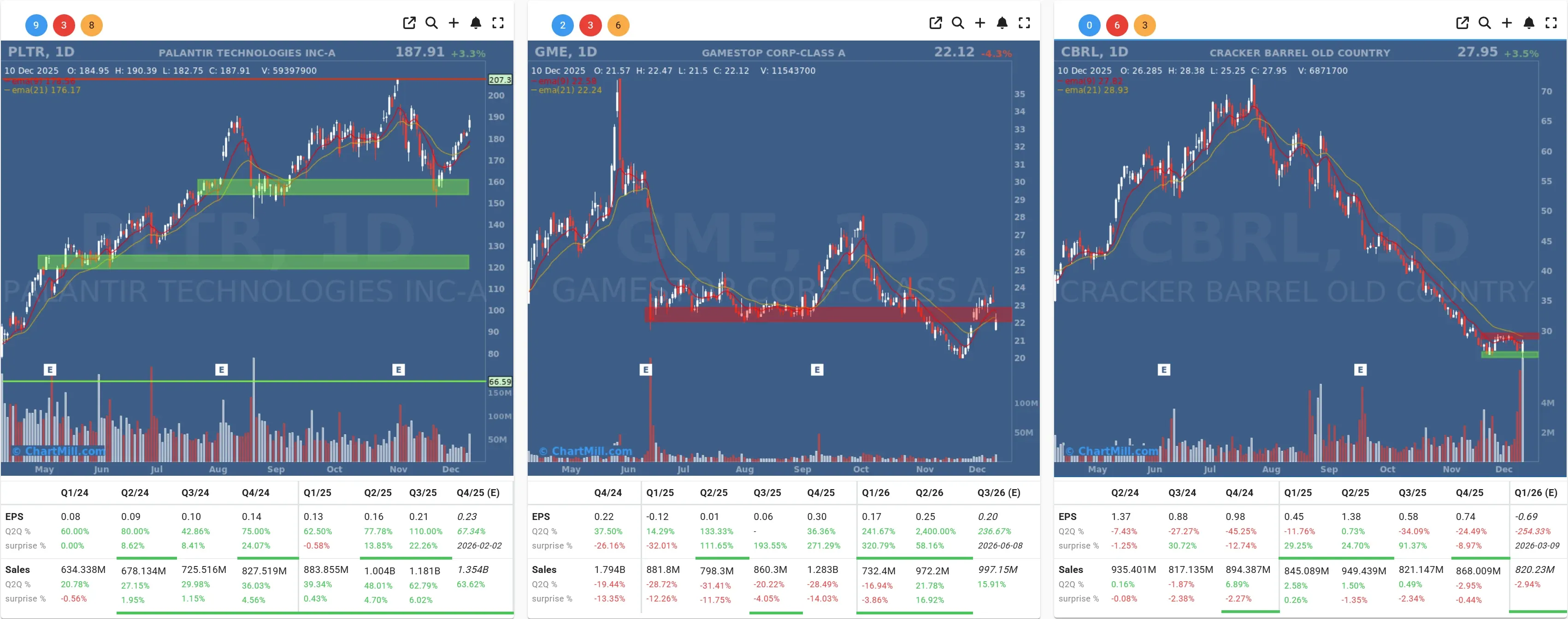

Other Notable Movers: Palantir, Cracker Barrel and GameStop

Palantir (PLTR | +3.34%) rallied after landing a new contract. The market still loves any confirmation that the company can convert its government and commercial AI narrative into real, ink-on-paper deals.

Cracker Barrel (CBRL | +3.52%) gained after earnings, even though the company cut its full-year profit outlook. Classic case of expectations being low enough that “less bad” is actually good.

GameStop (GME | -4.28%) slid as quarterly revenue fell again. The meme era may not be dead, but the fundamentals are still whispering “brick-and-mortar retail, not AI”.

Together, these moves underline a theme I keep coming back to: stock-specific catalysts still matter, even in a macro-driven tape.

After Hours: Oracle Stumbles, Adobe Leans Into AI

The real drama came once the closing bell rang.

Oracle: Big AI Spend, Not Enough Revenue…

Oracle (ORCL | +0.67%) looked fine in the regular session, but traded about 11.5% lower after hours as investors digested a mixed set of numbers.

Key details from the quarter ended in November:

- Adjusted EPS of $2.26, up 54% year-on-year and well ahead of the $1.64 consensus.

- Total revenue up 14% to $16.1 billion, just shy of the roughly $16.2 billion analysts expected.

- Cloud infrastructure revenue up a scorching 68% to $4.1 billion, fuelled by GPU-heavy AI data center demand.

So why the sell-off?

The market has zero patience for any hint that massive AI capex and ballooning debt aren’t translating into equally explosive top-line growth. A small revenue miss after a hype-driven run-up feels like a classic “expectations reset” moment. The AI narrative is intact, but the bar was simply too high.

This doesn’t break the Oracle story, but it does remind everyone that AI infrastructure is capital-intensive and lumpy, not a straight line to the moon.

Adobe: Strong 2026 Guidance, AI Story Still Front and Center

By contrast, Adobe (ADBE | -0.35%) delivered exactly what the market wanted to hear: solid Q4 numbers and an upbeat 2026 outlook built on its generative AI push (Firefly) embedded across Creative Cloud.

For fiscal 2026, Adobe now guides to:

- Revenue of $25.90–26.10 billion, above consensus of about $25.87 billion.

- Adjusted EPS of $23.30–23.50, also ahead of expectations.

Since the launch of ChatGPT, Adobe has been racing to defend and expand its creative software moat with AI-assisted tools. Competition is heating up, but this guidance reassures investors that AI is adding to the pie rather than cannibalizing it.

I’d frame Adobe as one of the more “real economy” AI winners: instead of selling GPUs, it sells productivity to students, designers and enterprises who are increasingly locked into its subscription ecosystem.

How I’m Thinking About Portfolios Here

Pulling it all together, my current bias looks like this:

Macro: The Fed is likely on pause for a while, barring a sharper labor-market deterioration. That should keep the “quality growth + AI” trade supported, but caps how far yields can fall from here.

Policy risk: Trump’s very public pressure campaign on the Fed, plus the looming choice of a Powell successor, is an under-priced volatility factor for 2026–2027.

Thematic tilt: AI remains the dominant theme, but today showed how picks-and-shovels plays like GE Vernova can sometimes outshine pure software names.

Idiosyncratic risk: The chip lawsuits against Intel, AMD and Texas Instruments are a reminder that geopolitical and compliance tail risks don’t show up in a simple P/E screen.

If you’re an active investor, I’d be using this backdrop to lean toward balance: keep exposure to AI infrastructure and quality growth, but pair it with names that benefit from lower yields and a softer dollar, and be willing to step aside when expectations, like Oracle’s tonight, get too far ahead of fundamentals.

Kristoff - ChartMill

Next to read: Small Caps Lead as Breadth Re-Accelerates After Monday’s Shakeout