For investors looking for long-term growth at fair prices, few methods hold the importance of Peter Lynch’s proven strategy. As the famous manager of Fidelity’s Magellan Fund, Lynch stressed investing in companies with lasting earnings growth, sound financial condition, and fair valuations, principles that stay important decades later. His method combines parts of both growth and value investing, concentrating on businesses that are not only growing but also selling at prices that do not overstate their future possibilities. One company now fitting many of Lynch’s main standards is Fluor Corp (NYSE:FLR), a worldwide engineering, procurement, and construction company.

Fluor satisfies several screening measures taken from Lynch’s thinking, starting with earnings growth. Lynch liked companies with a steady record of increasing earnings per share (EPS), preferably between 15% and 30% each year, sufficient to show solid expansion but not too fast to be unreliable. Fluor’s five-year EPS growth is at 27.7%, putting it directly within this goal range and showing a capacity to increase profitably over time.

Another foundation of the Lynch approach is valuation modified for growth, often calculated by the PEG ratio. Lynch viewed a PEG under 1 as an indicator of a fairly priced stock compared to its growth path. Fluor’s PEG ratio of about 0.69 implies the market could be pricing its growth possibilities too low, presenting what Lynch may term a “favourable risk-reward profile” for long-term investors.

Financial condition was just as important to Lynch, who chose companies with good balance sheets and acceptable debt. Fluor’s debt-to-equity ratio of 0.18 is not only under the screen’s limit of 0.6 but also matches Lynch’s stricter liking for ratios below 0.25. This shows a careful capital framework and lower financial danger. Also, the company’s current ratio of 1.62 is above the least need of 1.0, indicating enough immediate cash flow to cover its responsibilities, another Lynch-supported sign of working steadiness.

Profitability is the last main support. Lynch frequently used return on equity (ROE) to measure how well a company uses shareholder money. Fluor’s ROE of 69.5% is much higher than the 15% minimum Lynch supported, showing very effective use of equity and good management performance.

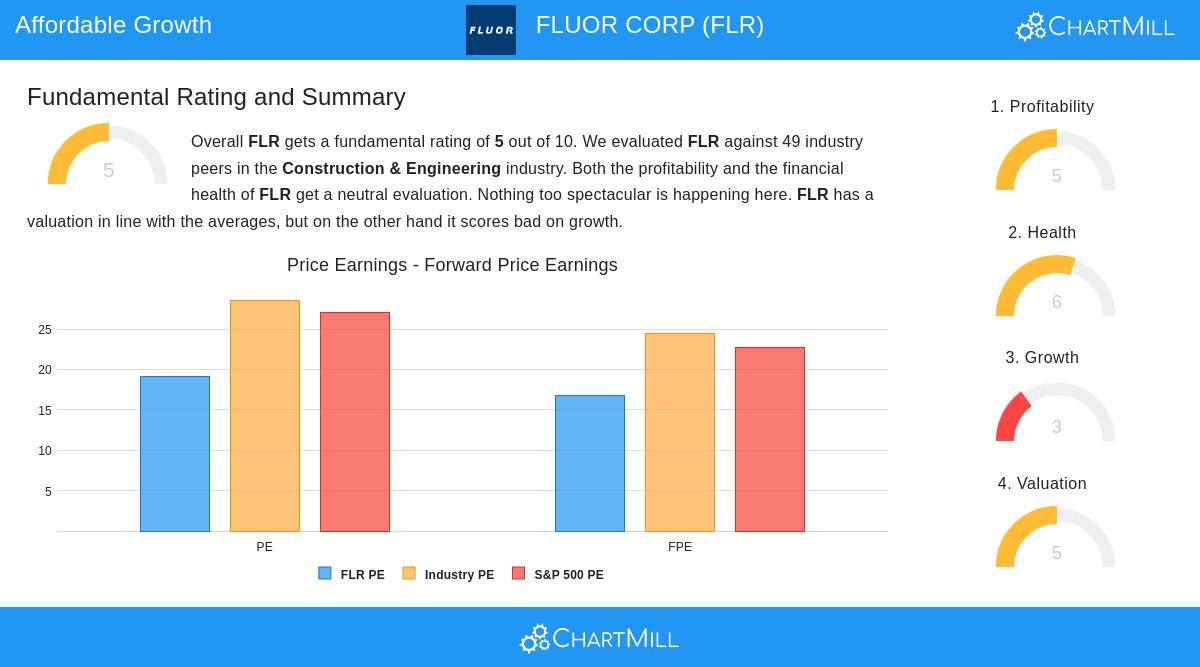

A wider view of Fluor’s basic profile backs this Lynch-led review. The company has an average profitability and financial condition score, with clear strong points in some return figures and solvency checks, although it deals with issues in operating margins and growth steadiness. Its valuation seems fair compared to both industry rivals and the wider market, with several measures pointing to price-level discounts. For a complete summary, readers can see the full fundamental analysis report here.

It is important to mention that Lynch advised investors to see past number-based screens and review non-number factors, like business plan clearness, market benefits, and industry situation. Fluor, with its varied activities in energy, city infrastructure, and government services, works in areas with long-term need supports. Its part in complicated, big projects offers some market protection, while its repeating government and industrial agreements add to income predictability.

For investors wanting to review other companies that fit this method, more screening outcomes based on Peter Lynch’s standards can be found via this link.

This article is for information only and does not form investment guidance. Investors should do their own study and think about their monetary position, risk comfort, and investment goals before making any choices.